.webp)

.webp)

.webp)

.webp)

"If fees consume more than 1% of your assets annually, you should probably shop for another adviser."

- The Intelligent Investor (1949) by Benjamin Graham, Warren Buffett's professor and mentor

Are you overpaying? High fees eat into your investment returns

There are two supermarkets within a 10-minute walk from my house, but I order my groceries on Redmart as it's slightly cheaper. I check Hotels.com and Expedia before booking any trips to find a good deal. It's so easy to compare prices for any purchases and save a few dollars, but it's shocking to realise that one of our largest expenses goes under the radar. Investors are surprisingly clueless on how much in fees they pay on investment products that over the long run could amount to hundreds of thousands of dollars. Can you think of any other products or services where you have no idea what they cost?

Time and time again, fees have been proven to be one of the key determinants of long-term returns. Fees can vary greatly between different mutual funds or unit trusts, different share-classes of the same funds, or even buying the same fund via different banks or brokers. Bottom line is: You can't control where the markets go, but you can control how much you pay in fees.

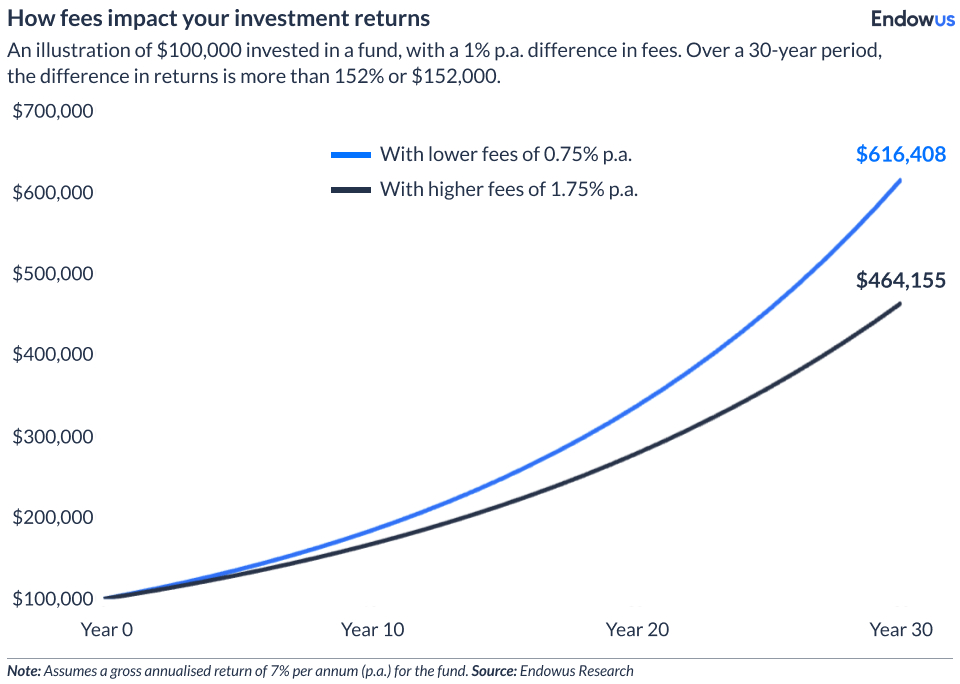

A $100,000 investment in a fund earning 7% per annum (a good return), but with a fee of 1.75% versus 0.75%, will deprive you of about 152% in returns (or $152,000) over 30 years.

A cheat sheet of fund fees

Here are some common types of fees that investors should look out for when investing in unit trusts or mutual funds:

Upfront fee, front-end load or initial sales charge

Typically 2-5% in Singapore

Fee payable by you to the bank, financial advisor or broker who sold you the fund. This is charged as a percentage of your investment amount and should be negotiated.

Wrap fee

Typically 0.35-1.5% p.a. in Singapore

Fee charged by a bank, financial advisor or broker for investment advice, administration or other investment services. This is charged as a percentage of the market value of your portfolio. Make sure you know what you are getting for the wrap fee, and do not have to pay other fees on top that you thought were included.

Platform fee

Typically 0.20-1% p.a. in Singapore

Fee generally charged by online platforms (i.e. Fundsupermart) for administration of your investments and use of their platform. This is charged as a percentage of the market value of your portfolio.

Brokerage fee

Typically 0.20-0.50% of your transaction amount in Singapore

Fee charged by banks, financial advisors or brokers for executing the transaction of a fund or other financial product.

Switch fee

Typically 0.5-1% of your investment amount in Singapore

Fee charged when you switch from one fund to another. This is not common, but still exists on some platforms. You really should not have to pay this, ever.

Redemption fee

Typically 1-5% of your investment amount in Singapore

Fee payable whenever you sell or redeem a fund. Some funds progressively reduce the redemption fee if you hold your investment over a longer period of time. Also less common these days, but still exists for some retail investment products.

Expense ratio, ongoing charges or management fee

Typically 1-2.5% p.a. for retail share classes available in Singapore

An annual fee the funds will charge for fund expenses, including management fees, administrative fees, and operating costs. This is deducted from a fund's net asset value (NAV), and accrued on a daily basis.

This is the only fee that institutional investors pay, and it is typically a fraction of what retail investors pay. For example, the same fund with both institutional and retail share classes will charge institutional investors ~0.50% and retail investors anywhere between 1-2.5%.

Trailer fee

Typically 50-60% of the expense ratio in Singapore

This is a scary one. The elusive recurring distribution commission is paid by the fund management company to the bank, financial advisor or broker that sold you the fund. This fee is paid as long as you hold the fund in your portfolio. This means that you're not able to see this fee directly - you will only see it as a reduction in the net asset value (NAV) of the fund and as some part of the expense ratio the fund manager is charging you.

You can read more about trailer fees in our article.

Low, fair fees with Endowus — keep much more of your returns

Fees are important to your investment returns. On Endowus, individuals get institutional access to high-performing funds at the lowest possible, fair, and transparent fees.

Previously, individual investors in Singapore were not able to invest in the cheaper class of funds, known as the institutional share-class. But not anymore — you can now invest in institutional share-class funds, some exclusively on Endowus, starting from just $1,000.

The all-in Endowus Fee is a per-annum fee based on the value of assets you hold with Endowus. We do not charge a sales fee, transaction fee, or any other hidden fees, unlike other platforms. You also get 100% Cashback on all commissions, known as trailer fees — as of January 2023, we have returned more than S$6 million in these fund-distributor commissions to customers since inception.

Unlike other platforms, we do not collect trailer fees, which eat into your returns and wrongly incentivise other advisors and platforms to sell certain funds that may not be suitable for you. This reduces our costs to a fraction of the industry average, which then translates to better returns for you in the long term.

For more information on our transparent fee structure, click here. To get started with Endowus today, follow this link.

<divider><divider>

This article is for information purposes only and should not be considered as an offer, solicitation or advice for the purchase or sale of any investment products. It is recommended that you seek financial advice as to the suitability of any investment. Whilst Endowus Singapore Pte. Ltd. (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Investment involves risk. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Past performance is not an indicator nor a guarantee of future performance.

Please note that the above information does not purport to be all-inclusive or to contain all the information that you may need in order to make an informed decision. The information contained herein is not intended, and should not be construed, as legal, tax, regulatory, accounting or financial advice.

.jpeg)

%20(1).gif)