- Some Asian equity markets have long traded at a discount to global peers - a reflection of governance risks rooted in concentrated ownership, cash hoarding, and weak minority shareholder protections. That structural drag may finally be unwinding.

- Japan's TSE capital efficiency push and revised Stewardship Code mark the most sustained reform effort in the region. Korea's 2025 Commercial Code amendments and dividend tax cuts directly attack the "Korea discount."

- Chaebol structures and cross-shareholding networks remain incompletely dismantled. For investors with a sufficiently long horizon, however, these efforts to achieve more transparency may offer an opportunity for upside.

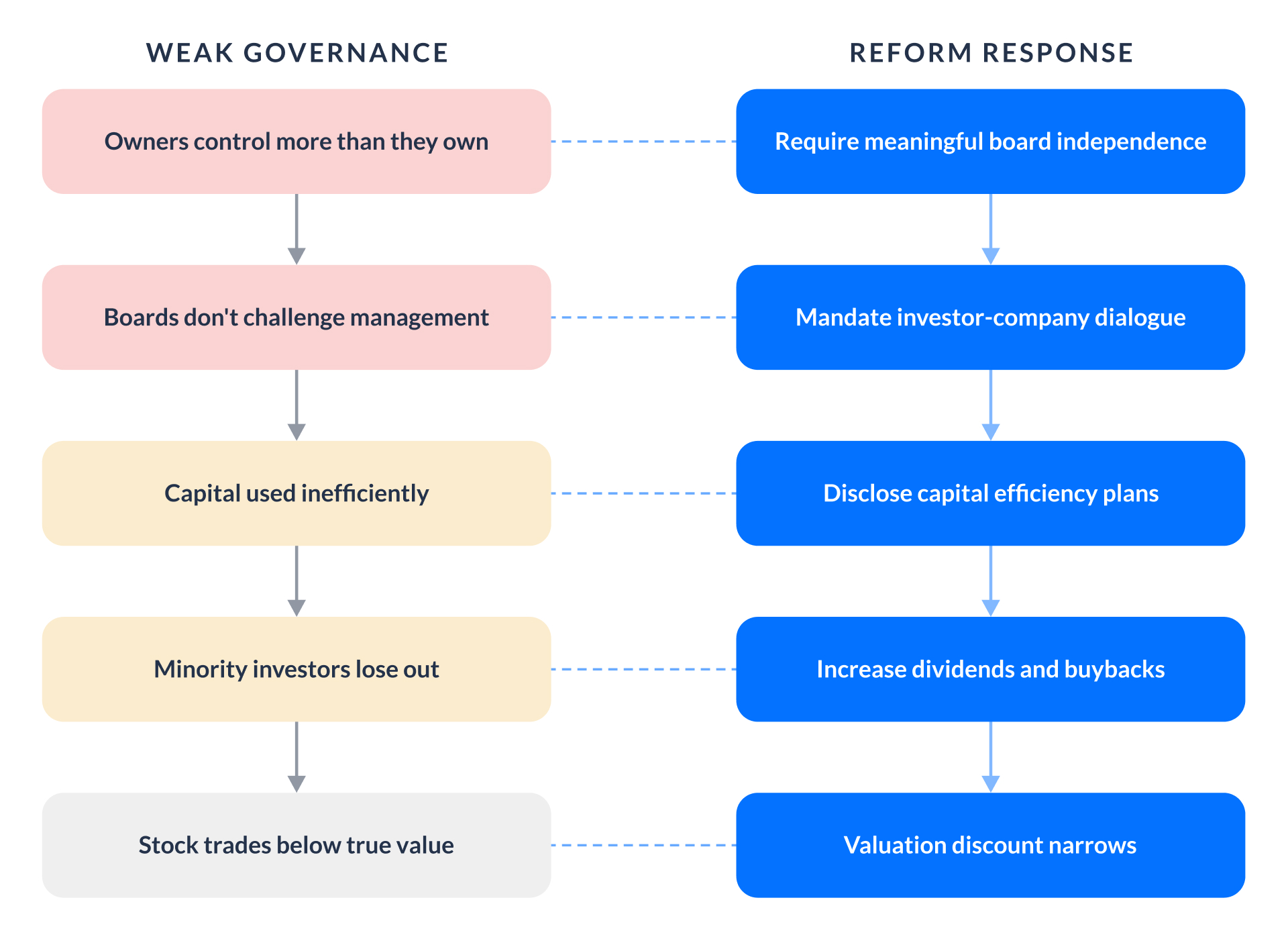

Corporate governance - the framework regulating the relationship between a company's shareholders and its management - has traditionally been weak in Asia. More specifically, family ownership of large conglomerates, weak board independence and opaque related-party transactions have been systematically damaging minority shareholders, creating a drag on market performance.

Two decades after the 1997 Asian financial crisis - which exposed these vulnerabilities with devastating force - reform agendas currently underway appear promising, and may offer potential upside going forward to investors willing to allocate to Asian markets.

The roots of weak corporate governance in Asia

Governance issues in Asian listed companies are tied to specific economic policy choices. Indeed, most countries favoured concentrated ownerships - especially in key sectors of the economy - as they made it easier to implement industrial policy. In turn, close relationships between these owners and policymakers helped keep these incentives intact.

As a result, large conglomerates - the Japanese keiretsu, South Korean chaebols, and their Southeast Asian equivalents - prospered, with a legal framework allowing controlling families to exercise key decision-making powers despite limited actual economic ownership (as highlighted by the G20/OECD Principles of Corporate Governance).

An OECD assessment published in 2001 found that prevailing governance mechanisms in Asia "often did not encourage management to use resources efficiently,” and governance systems that tended to "protect the interests of controlling investors at the expense of minority investors." Academic analysis of the crisis further characterised the pre-reform environment as one of "crony capitalism, opaque accounting and auditing systems, and too close relations between business and the state[1]."

Japan: Leaping forward with the TSE capital efficiency push

Japan's reform trajectory is arguably the most sustained and sophisticated in the region. The introduction of the Stewardship Code in 2014 and the Corporate Governance Code in 2015 established a dual-track framework - operating on what the OECD Principles describe as a "comply or explain" basis - that assigned explicit responsibilities to both companies and their institutional investors. The logic was that governance failures were not just caused by the controlling parties, but also a function of passive institutional ownership - large shareholders that held diversified portfolios had weak incentives to engage with individual investee companies, facilitating managerial entrenchment.

More recently, the 2021 revision of the Corporate Governance Code tightened requirements on board independence, cross-shareholding disclosure, and diversity, particularly on the Tokyo Stock Exchange's (TSE) newly restructured Prime Market. The more consequential intervention came in March 2023, when the TSE formally requested that Prime Market-listed companies trading below book value develop and disclose plans to improve capital efficiency. This was a direct regulatory challenge to Japan's long-standing corporate culture of cash hoarding and low return on equity - behaviours enabled, in part, by the cross-shareholding networks that insulated management from market discipline (as a reminder, the more efficiently capital is used, the higher the return, which ultimately benefits all investors - and the stock price). By 2024, 72% of Prime Market companies had disclosed capital efficiency measures, and 94 companies were delisted in a drive for quality, the highest number since 2013[2].

The revised June 2025 Stewardship Code (Version 3) abandons a fixed three-year review cycle and explicitly rejects a box-ticking approach, emphasising substantive investor-company dialogue[3]. By mid-2024, the proportion of Prime Market companies with at least one-third independent directors stood at 98.1%, up from 6.4% before the Code's introduction[4]. Cross-shareholding unwind has also since accelerated, with Japan's three largest insurance companies committing to divest their strategic holdings entirely.

Tackling the "Korea Discount": Corporate value-up reforms

South Korea's governance reform agenda is more recent and confronts more entrenched structural obstacles. The "Korea discount" - the persistent undervaluation of Korean equities relative to regional and global peers - has been extensively documented. According to the Korean Corporate Governance Forum, a 100 million won investment made ten years ago would now be worth approximately 160 million won in Korea, compared to 280 million won in Japan and 340 million won in the United States. Two-thirds of KOSPI-listed companies were trading below book value (as of early 2024[5]), which, to be clear, is only positive if the excess cash problem is addressed and the liquid funds are properly invested for the company’s growth.

Before 1997, penalties for securities law violations were capped at the equivalent of under US$7,000[6]. But even after the crisis, improvements were slow to come. A 2006 analysis in the Asian Journal of Comparative Law acknowledged that post-crisis Korean reforms had produced more transparent and accountable companies on paper, with boards and auditors beginning to function more effectively - but argued that Korea needed a further stage of reforms before companies could receive proper valuations, a judgement that remained accurate for nearly two more decades[7].

Chaebols - family-controlled conglomerates operating across multiple sectors through complex circular ownership arrangements - dominate the Korean corporate landscape. Similarly to Japan, they exercise voting rights far in excess of their economic ownership through cross-shareholdings and layered holding structures. Dividend payout ratios are structurally depressed, partly because South Korea's inheritance tax rate - effectively around 60% for listed company owners - creates incentives for controlling families to suppress valuations rather than distribute earnings.

The Corporate Value-Up Program, announced in February 2024, drew explicit inspiration from Japan's TSE capital efficiency initiative. Listed companies are now encouraged to disclose multi-year plans targeting improvements in return on equity, price-to-book ratios, and dividend yields. A Korea Value-Up Index was launched in September 2024 to identify companies meeting defined thresholds on profitability, shareholder return, and valuation[8].

The more substantive legislative development came in July 2025, when the National Assembly passed amendments to the Korean Commercial Code expanding directors' fiduciary duties to encompass the interests of all shareholders - not just the company - and strengthening cumulative voting mechanisms for minority investor representation. A further August 2025 amendment reinforced minority shareholder protections. These are structurally significant changes, particularly the expansion of fiduciary duty, which the OECD Principles identify as central to addressing minority shareholder abuse[9].

The critical limitation remains enforcement and scope. The Value-Up Program is largely voluntary. Cross-shareholding and circular ownership structures - the core mechanisms of chaebol control - have not been directly dismantled by the amendments. Mandatory disclosure of related-party transactions, another foundational requirement of the OECD framework, remains outside the current scope of reform[10].

Reasons for optimism: Unlocking long-term upside in Asian equities

There are meaningful reasons to think the current reform cycle may be able to unlock value.

In Japan, the shift toward substantive behavioural change - a ramp-up of investor-company dialogue - marks a qualitative step beyond purely formal checklists. In Korea, the passage of Commercial Code amendments expanding directors' fiduciary duties, combined with the December 2025 reduction in dividend tax rates from 45% to 14–30%, directly addresses two of the structural incentives - weak board accountability and depressed payout ratios - that have historically sustained the Korea discount. As of the end of 2025, 174 Korean companies had disclosed Corporate Value-Up Plans, and the Korea Value-Up Index had risen over 130% since its September 2024 introduction[11].

The historical governance discount embedded in Asian equity valuations was not irrational - it reflected real risks of inefficient capital allocation and opaque ownership structures. If the current reforms prove durable, that discount may narrow. That outcome is not guaranteed, and the chaebol structures and cross-shareholding networks that have historically undermined governance in both markets remain incompletely dismantled. But for investors with a sufficiently long horizon, the direction of travel is clearer than it has been at any point since 1997.

Sources

- Clarke, T., "Crisis and Reform in Corporate Governance in Asia," in Haley & Richter (eds.), Asian Post-Crisis Management, Palgrave Macmillan, 2002

- TSE/FSA, Action Programme for Corporate Governance Reform 2024: Principles into Practice, June 2024; J.P. Morgan Asset Management, Japan's Corporate Reforms Boost Shareholder Value, 2025

- FSA, Stewardship Code Version 3.0, June 2025; ACGA, Decoding Japan's New Stewardship Code and 2025 FSA Action Programme, 2025

- 5TSE/JPX, TSE's Recent Initiatives, 2024

- Korean Corporate Governance Forum, 2024, cited in The Korea Times, November 2025; Glass Lewis, Navigating South Korea's Corporate Value-Up Program, 2024

- ADB, Corporate Governance in Asia: Recent Evidence from Indonesia, Republic of Korea, Malaysia, and Thailand, Asian Development Bank Institute, 2003

- The Next Stage of Reforms: Korean Corporate Governance in the Post-Asian Financial Crisis Era, Asian Journal of Comparative Law, Vol. 1, 2006

- Financial Services Commission, Corporate Value-Up Program Guidelines, May 2024

- Berkeley Journal of International Law, Beyond the Korea Discount: How the August 2025 Commercial Code Amendment Addresses (and Overlooks) Chaebol Dominance, December 2025; ACGA, A Crossroad for CG Reforms in Korea, 2025

- OECD, Asia Corporate Governance Programme, 2025

- Janus Henderson Investors, Corporate Governance Reforms: Unlocking Shareholder Value in Japan and South Korea, February 2026

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

This article is not intended to be relied upon as a forecast or research or investment advice, and should not form the basis of any investment or other decisions. The information contained herein is not intended, and should not be construed, as any legal, tax, regulatory, accounting or financial advice. If you would like investment, accounting, tax or legal advice, you should consult with your own professional advisors regarding your individual circumstances and needs.

The information in this article may not be suitable for all investors. You are responsible for any action that you take or decision that you make in reliance on any content in this article, and you agree that Endowus HK Limited (“Endowus”) is not liable under any circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a recommendation, offer or solicitation by Endowus or its affiliates to you to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction.

This is not intended to be an invitation or offer made to the public to subscribe for any financial product or to enter into any transaction.

Accuracy of Information

Whilst Endowus has made reasonable efforts to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or errors in any such information. Endowus does not warrant or represent that the information in this article is correct, accurate or reliable.

Opinions

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this article are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

This article has not been reviewed by the Securities and Futures Commission of Hong Kong.

.png)