.jpg)

I grew up believing that opening an umbrella indoors would invite ghosts into the house and that every grain of rice left uneaten in my bowl would someday manifest as a pockmark on my future spouse’s face—two superstitions that, despite their absurdity, ensured dry floors and spotless plates. In our household, such beliefs were treated as undeniable truths, passed down without question and shaping our behaviors in subtle ways.

The same unquestioning acceptance often applies to assumptions about investing, particularly when it comes to gender.

We are told that men are naturally inclined to take risks while women are more cautious, that men are rational decision-makers while women are emotional investors. But just as I eventually realised that leftover rice had no bearing on my future spouse’s complexion, it’s time we rethink these deep-rooted beliefs that reinforce outdated gender stereotypes.

Societal practices that seemingly or unwittingly reinforce beliefs

Women indeed hold up half the sky—it’s no secret that they earn, inherit, and manage more wealth than ever before.

In Asia, women collectively control more wealth than in any other region except North America. Their financial influence is growing faster than anywhere else in the world. Despite this progress, women globally are expected to accumulate only 76% of the wealth of men by the end of their working lives, according to the 2022 Wealth Equity Index from Willis Towers Watson and the World Economic Forum.

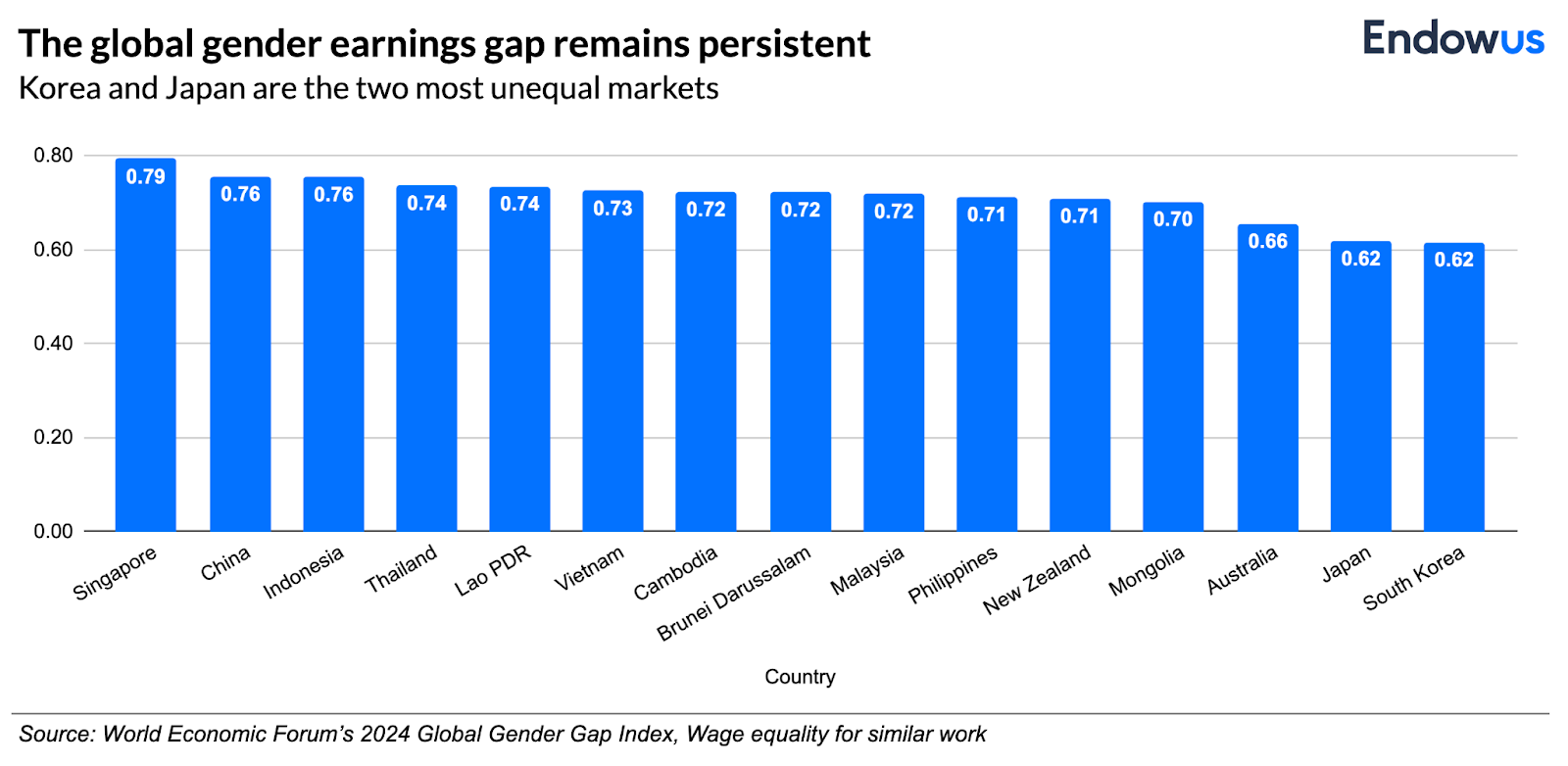

The global gender earnings gap remains persistent, and within Asia, Korea and Japan stand out as the most unequal markets. According to the World Economic Forum’s 2024 Global Gender Gap Index for wage equality for similar work, the two countries received scores of 0.617 and 0.619, respectively – the scores track the distance covered towards parity (i.e. the percentage of the gender gap that has been closed).

Data by the Hong Kong government in 2024 shows that men aged 15 and above earns a median monthly income of more than 40% higher than those of women.

One key factor is the disproportionate burden of unpaid care and domestic work. Women, on average, spend three times more time on these responsibilities than men. Yet, care work can often be undervalued and underpaid, which also means that they have less capacity to generate income through employment and wealth creation through investing.

This gender gap is not just a “women's” problem – the lack of parity limits growth and innovation for all. It is estimated that women could unlock more than US$3 trillion of additional investment capital globally if they invested at the same rate as men.

Gender is not the key differentiator in how people invest

There’s been a lot of research done to understand the behavioural differences between men and women in investing, exploring questions such as which gender has behavioural traits that lead to better investment outcomes.

Studies suggest that men, on average, report saving and investing more frequently, and are more likely to identify as investors, whereas women tend to be more risk-averse and less confident in their financial decisions. These findings have shaped widespread perceptions about gender-based investment behaviours.

When you take a deeper dive, men and women share more fundamental similarities in their investing views and habits than conventional wisdom suggests. The key differences appear to be influenced more by social and demographic factors such as employment status and income level, rather than innate traits. Income is a far stronger predictor of investment behaviour and attitudes than gender.

One of the most notable differences is perceived financial knowledge. According to Fidelity, women are nearly two times likelier to describe their investing knowledge as “beginner”. When asked about financial confidence, many women instinctively respond, “I should be doing more,” regardless of whether that sentiment is objectively true.

Perhaps, the real question is whether self-expressed confidence is even relevant. Many financial surveys continue to focus on this question, which yields the same outdated conclusions. Instead, what may matter more is being accurately attuned to one’s level of knowledge and risk tolerance, rather than overestimating one’s ability to outsmart the market.

Recognising that gender-based differences in investing are largely overstated is empowering. It means that financial success is driven not by inherent traits but by individual choices, access to resources, and informed decision-making. Dispelling these outdated stereotypes reinforces the idea that everyone, regardless of gender, can take control of their financial future. At the end of the day, the principles of successful investing – diversification, taking appropriate risk, staying invested for the long term - are universal and not dictated by gender.

I’m passionate about trying to bridge the investment gap, but superficially pink-washing financial products and marketing them exclusively to women does not cut it. It perpetuates the belief that women require a fundamentally different approach to money, rather than addressing the structural issues that impact a woman’s financial journey, such as taking a career break to raise children or longer average lifespans that require more retirement planning.

Goodbye to stereotypes

It’s time to bid goodbye to The Wolf of Wall Street stereotypes – investing is not inherently a gendered activity.

Wealth management for women should recognise these structural challenges without being patronising or perpetuating outdated stereotypes about innate gender differences.

A woman who takes time out for caregiving needs a financial plan that compensates for lower income during this time, and the disparity between what women will need over their lifetimes due to the pay gap and longer lives means that their investment portfolio perhaps actually needs to take more risk.

At the end of the day, a woman may go through a different life journey, but we want the same things as men when it comes to financial advice: A personalised approach that is tailored to our individual needs and goals.

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

This article is not intended to be relied upon as a forecast or research or investment advice, and should not form the basis of any investment or other decisions. The information contained herein is not intended, and should not be construed, as any legal, tax, regulatory, accounting or financial advice. If you would like investment, accounting, tax or legal advice, you should consult with your own professional advisors regarding your individual circumstances and needs.

The information in this article may not be suitable for all investors. You are responsible for any action that you take or decision that you make in reliance on any content in this article, and you agree that Endowus HK Limited (“Endowus”) is not liable under any circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a recommendation, offer or solicitation by Endowus or its affiliates to you to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction.

This is not intended to be an invitation or offer made to the public to subscribe for any financial product or to enter into any transaction.

Accuracy of Information

Whilst Endowus has made reasonable efforts to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or errors in any such information. Endowus does not warrant or represent that the information in this article is correct, accurate or reliable.

Opinions

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this article are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

This article has not been reviewed by the Securities and Futures Commission of Hong Kong.

.png)