The original version of this article first appeared in The Business Times.

Another year goes by with major stock markets at or near historic highs. Global equity markets, including the US, wrapped up 2025 with a strong finish. Expectations among Wall Street market strategists remain almost unanimously bullish for 2026.

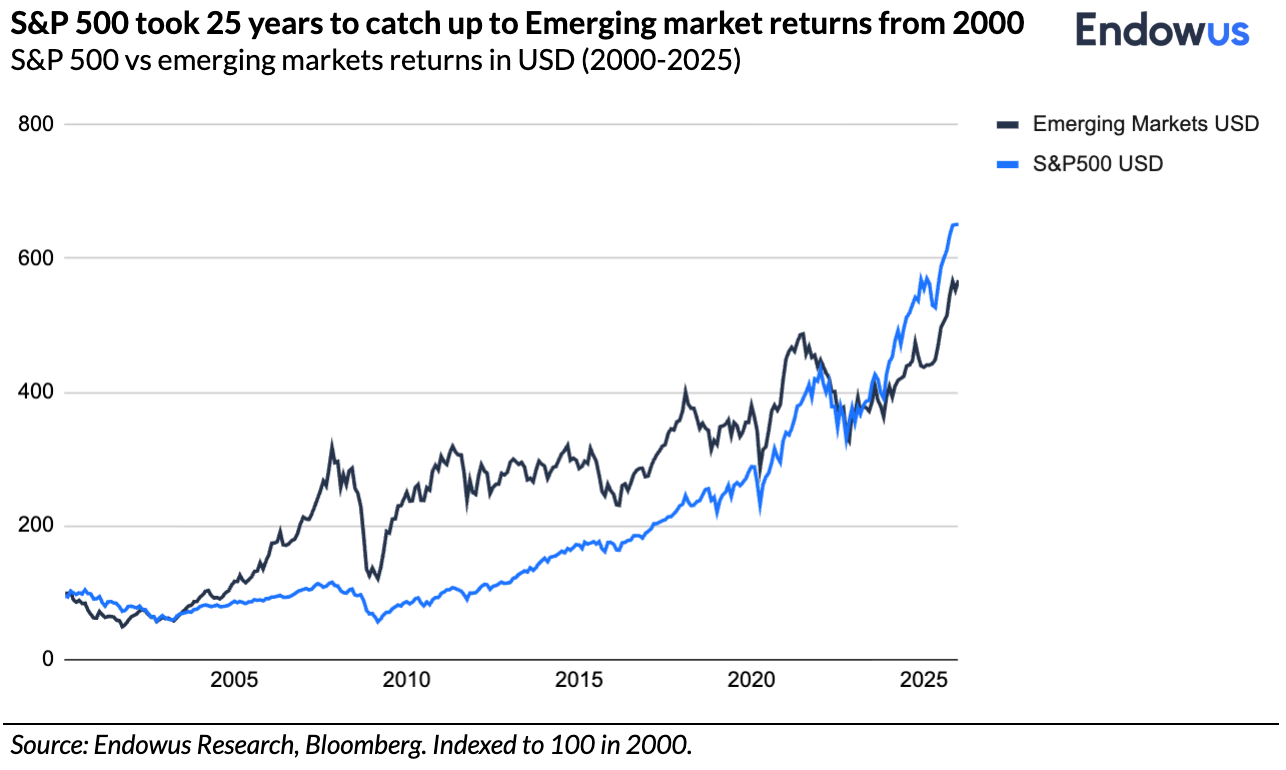

The popular US S&P 500 Index delivered a solid return of 17.9% for the year in US dollar terms. This comes on the back of three consecutive years of positive returns, and being up six out of the past seven years - all rising by double digits.

In most cases, investors should be happy with such a return, but human psychology does not work that way because we know how to compare. Unfortunately, the S&P 500 did not just underperform the tech-heavy Nasdaq index for the third consecutive year; it underperformed global markets ex-US by a historic margin.

The emerging markets index returned 29.8%, and the developed equity market ex-US (MSCI World ex-USA) returned 32.4%. The best performing market globally last year, South Korea, saw its KOSPI index deliver a stellar 83.2% return for the year.

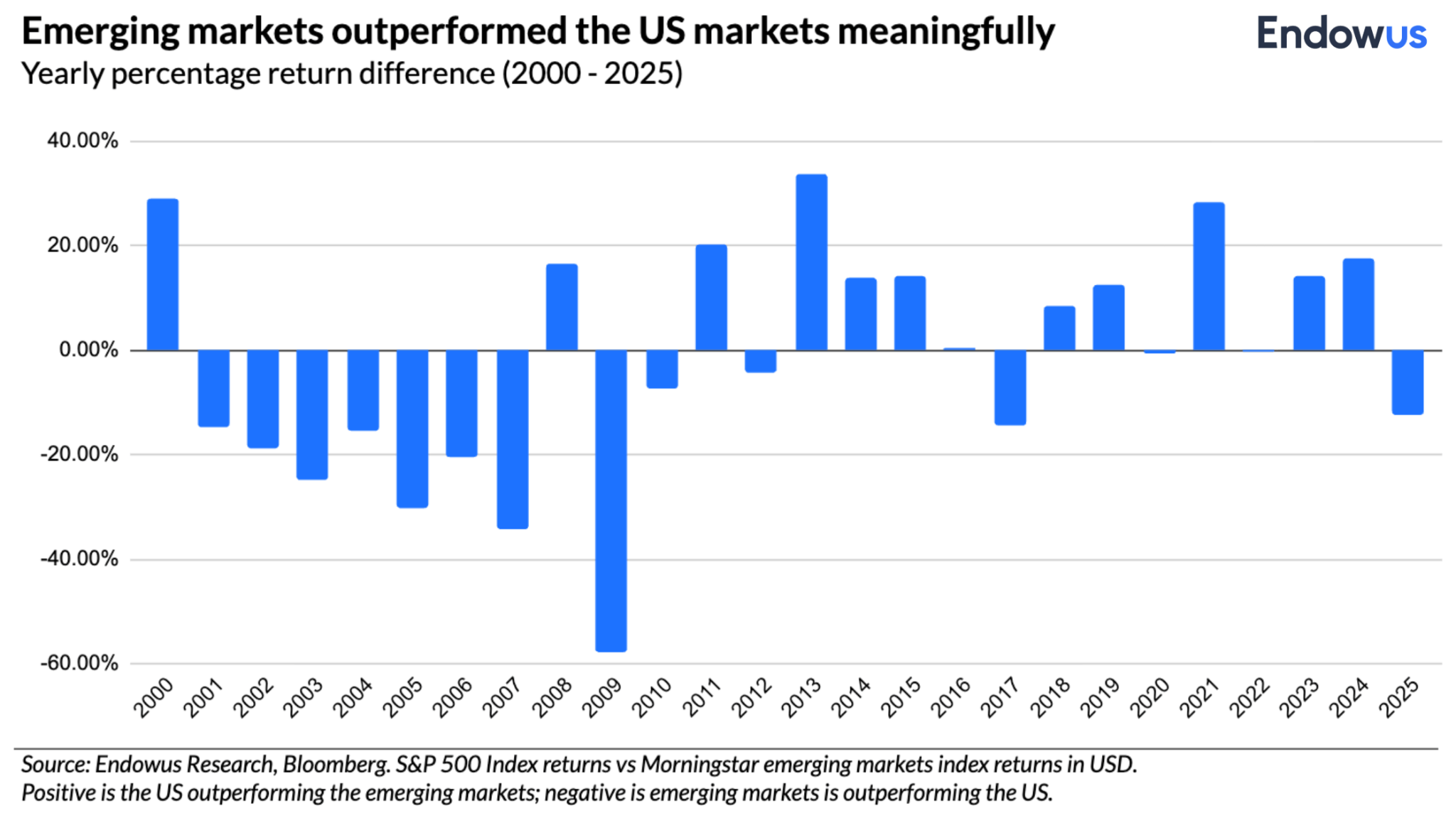

What is remarkable is that 2025 was the first time in eight years that emerging markets outperformed the US market, and only the second time in 15 years. However, this was not always the case. After the tech bubble burst in 2000, emerging markets outperformed US markets for seven consecutive years between 2001 and 2007.

Back to basics: What drives stock market returns?

Equity markets are fundamentally driven by three factors: earnings growth, multiple expansion, and currency movements. When you add the payouts received through dividends, it gives you what is called the total return for the market or index.

A company is highly impacted by top-down macro factors such as economic growth or consumer demand for products and services. How they are priced and how input cost move is impacted by and impacts inflation which are closely tied with interest rate policies. Furthermore, micro factors also impact earnings such as the company’s management and strategy as well as investments, cost management. It is the combination of all of these and many other factors that will drive profit growth.

Thus when looking at earnings, it is more about where we are in the cycle and the size of the delta. Over time, earnings almost invariably rise as the economy, trade, monetary base all expand over the long term. It is also a nominal number and therefore inflation will raise it more and thus a positive factor that underpins the markets.

So, what will happen in 2026?

The S&P 500's performance in 2025 was largely grounded in earnings which is estimated to have risen by 13.6%. As we look toward 2026, the gears are shifting.

Earnings growth is likely to decelerate even if growth remains strong as most expect, or it could turn negative if a US recession takes hold. With dividends unlikely to change much and currency moves remaining highly uncertain, the only remaining lever for the US market is multiple expansion (investors paying more for every dollar of profit).

The problem? US valuations are already high. The S&P 500 is trading at more than 22 times forward earnings to close out the year — a clear premium to history.

The US CAPE (Cyclically Adjusted Price-to-Earnings) ratio remains near the 99th percentile of its long-term averages. While valuations are notoriously poor at timing the market in the short term, they are incredibly helpful in marking long-term future expected returns. A higher starting valuation almost mathematically guarantees a lower return profile over the next decade, and vice versa.

Of course, if you draw out a positive scenario, it is not unfeasible to see US economic growth remaining robust, allowing companies to generate good earnings growth, all while multiples, with falling interest rates, could expand further, and companies pay out higher dividends resulting in another positive year.

But, the bigger question that is being drawn here is whether it will be another repeat of last year, when the US did exactly that and yet left a lot of investors unhappy due to the better performances elsewhere and the impact of a weaker currency that dragged on returns.

Whether markets end up going up this year or down, it seems that being diversified, therefore, is even more vital for your portfolio this year. The starting point for valuations remains significantly lower in most global markets outside the US despite last year’s outperformance. By diversifying, you aren't just hedging your risk; you are positioning yourself where the mathematical probability of future returns is more in your favor. This may also be the case for factors such as value versus growth, and asset classes such as fixed income and private markets.

Sometimes less is more

As we begin a new year, it is easy to do one of two things—on the one hand, the path of least resistance is to continue to extrapolate the current trajectory of markets and asset prices as we approach another historic high and a continued optimism in the markets.

Or, on the other, just because we have seen a switch in the calendar year to a new year, suddenly thinking that things need to change, and expecting markets to reverse or change course, even though underlying fundamentals do not change in a few days or a few weeks.

In my over thirty years of investing, one of the most common mistakes I have seen, and the biggest temptation investors commonly face, is thinking that we have to do something.

The itch to take some kind of action as the new year begins is not necessarily good when it comes to investing. That impulse may be good and maybe we should all focus that new energy in becoming healthier, work on better relationships and pursue learning so we can continue to grow and improve ourselves.

Like new year’s resolutions, trying to do too much may be detrimental to achieving better outcomes. By prioritising what matters and sometimes doing less and focusing on the important strategic allocations, such as diversification, we may welcome (and enjoy) a year with fewer moves but better outcomes.

Read more:

- Why are markets reaching new highs, while the USD stays weak?

- This New Year, make financial goals that stick – here’s how

- Learn why passive investing beats active investing

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)