.webp)

.webp)

.webp)

.webp)

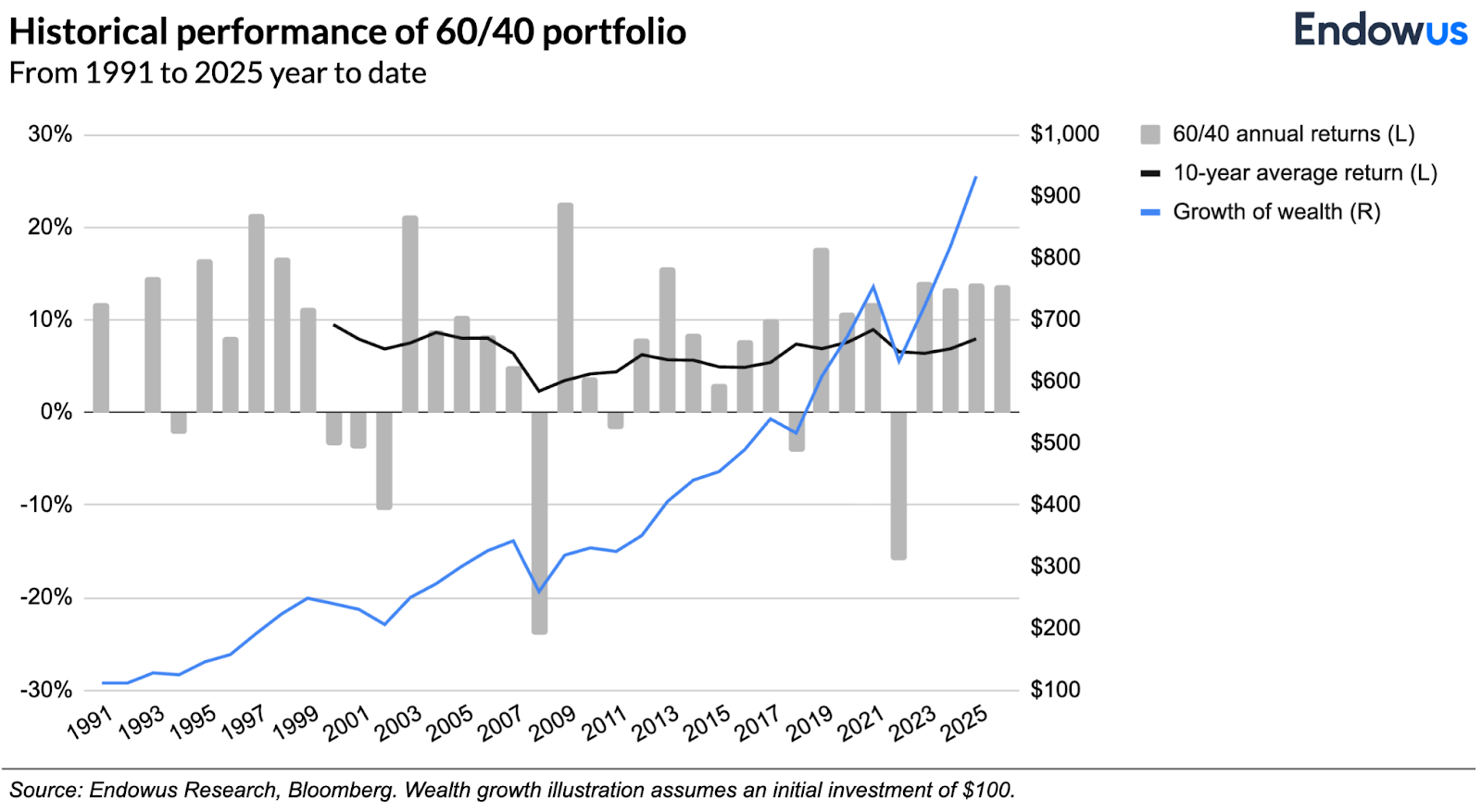

The 60/40 portfolio has returned 8% annual return over the past decade with an allocation to 60% global equities and 40% global fixed income. The past five year average is 7.4%. The 10-, 15-, 35-years all gravitate around the 7% mark, sometimes rising to 8% or falling closer to 6%. In the past 35 years, the 60/40 portfolio is up 833%. Those are some pretty impressive numbers and seem to go against most people’s expectations.

There have been so many articles about the death or demise of the 60/40 portfolio in recent years, mostly because of its anemic returns during 2021-2022. However, since the end of 2022, the 60/40 portfolio is up 40%. Is this normal and is this recovery sustainable?

60/40 works because of fixed income

Investors like the balanced portfolio because of the upside from equities, as we know stock markets rise over the long term. This is why we start with a higher equity allocation to compound growth.

However, investors do not choose 100% equities because of the volatility of the stock market. In particular, we hate to see large negative returns. This is why the portfolio adds fixed income as a hedge.

Hedging works only when there is a negative correlation between asset classes. Namely, when equities fall, fixed income should go up to soften the blow of losses. Has fixed income done its part? The answer to that question historically has been a resounding yes.

Most of the time, the 60/40 has been a great portfolio

Global stock and bond market indexes were incepted in 1991, which gives us 35 years of data. About two thirds of the time, or over 23 years, both stocks and bonds were up. In those years, the portfolio averaged annual returns of 12%.

There were three years (1999, 2013 and 2021) when stocks were up but bonds were down. This was also a good outcome as stocks rose much more than bonds fell. In fact, bonds showed an average decline of only 2.2%, while stocks rose by a whopping 23%.

Normally, in these years when stocks are up and bonds are down, the economy and earnings are strong and support the stock market. However, concerns about an overheating economy and/or rising inflation leads to rising interest rates, which hits fixed income. Shockingly, the 60/40 portfolio did even better in these three years than when both stocks and bonds were both up, averaging a phenomenal 12.9% annual return.

So in 26 years (three-quarters of the time), there is a happy scenario where the 60/40 has returned over 12% returns. This again shows how the equities performance provides enough upside even in a 60/40 portfolio. When this compounds over time, the returns could be quite significant as seen in the chart.

What about fixed income’s role in 60/40?

Let’s turn to the role of fixed income in the 60/40 portfolio and whether it did what it was supposed to do historically. In 31 of the 35 years, global bonds posted a positive return. So the first point to make is that fixed income returns are pretty stable with much less volatility than stocks, and in almost 90% of the time, bonds provide a positive contribution to the portfolio regardless of what equities do.

The second point may surprise many. In 12 years, or almost a third of the time, bonds actually generated a higher absolute return than equities. So fixed income contributes positively to the return of the portfolio often.

Finally, the third and most important point. In eight of the nine years that equities fell, fixed income returns were positive. So, fixed income more than played its part in dampening the negative effect of equity market volatility, especially at times when it is most needed. Diversification, therefore, has given us a better risk adjusted return. So what about the remaining one year?

What was the exception?

Only once in 35 years were stocks and bonds both down together. In 2022 equities was down 19% while bonds posted double digit negative returns of 11.5%. This followed a 1.3% return in 2021 and resulted in two consecutive years of negative returns. The first time both of these feats had occurred.

The only other times fixed income markets were down was 5.2% in 1999 and 0.2% in 2013. Returns turned negative in 2008 during the Global Financial Crisis and in 2020 during COVID, but in both cases it recovered, ending up 3.9% in 2008 and 5.4% in 2020.

A brief history of the bond bull market

It’s easy to forget that fixed income enjoyed an unprecedented period of good returns during a 50 year bull market since interest rates peaked in the 1970s and continued to meander its way down to zero in 2008 and again in 2020. The expansion of global free trade, lower cost of manufacturing and distribution, and a structural decline in costs and inflation gave free reign to central banks to cut interest rates.

However, it wasn’t just these disinflationary effects of globalisation, but also the deflationary shocks of the world lurching from one financial crisis to the next. The 1997 Asian Financial crisis, The Savings and Loan (S&L) crisis and the Long-Term Capital Management (LTCM) collapse, The dot-com bubble burst in 2000, the Global Financial Crisis in 2008, European debt crisis in 2013 and finally the COVID pandemic allowed the central banks, especially the US Federal Reserve, to take interest rates to zero.

The lower bound of interest rates was reached a second time in 2020 when many of the long term trends were reversing. Inflation started rising post COVID, accompanied by a sharp rise in global geopolitical tension that caused major disruptions to global supply chains. The upshot has been a new regime of higher for longer inflation and interest rates that led to the shock of 2022.

After peaking at the end of 2023, interest rates have been steadily albeit slowly coming down. The US was the last to cut rates last year and despite an extended pause, has recently started a new rate cut cycle that is likely to extend into 2026.

If the 2021-2022 period of sharply negative bond returns was an anomaly, then we are now entering a period when bonds benefit from both a high starting yield and the prospect of falling interest rates driving capital gains. Fixed income can once again play the role it has historically played so well – being a natural hedge against the volatility of equities.

Why is this time different?

The most dangerous four words in investing is “this time is different.”

The longer you invest, you realise that history indeed rhymes, but it doesn’t repeat itself. We have a recency bias where we anchor our expectations against what has happened most recently, when we should actually anchor our expectations on the longer term historical evidence. The 60/40 portfolio is such a case. We should not be overweight 2021-2022, but look at 1991-2025.

The 60/40 portfolio has generated 13.8% in the past three years. Even if this is unsustainable, a return to long term averages of 7-8% would be an attractive proposition as equities reach new highs and fixed income looks more attractive. The king is dead, long live the king!

Start your globally diversified portfolio with Endowus

The Endowus Flagship Portfolios are designed as a one-stop solution for investors seeking expert-curated, diversified global portfolios for long-term wealth accumulation at low, fair cost.

To simplify your investment journey, the Endowus Flagship Portfolios are offered as a Discretionary Portfolio Management (DPM) service on the Endowus Hong Kong platform. Behind the portfolios is an implementation of a strict, institutional-grade screening process by the Endowus Investment Office.

Investing should be made simple, for everyone. Click here to get started with Endowus today.

Read more:

- Following the laws of nature with markets

- Is diversification dead?

- Like Lego play, is your investment portfolio built to last?

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

- Due to its anemic returns during 2021-22, some have questioned whether this has marked the "death or demise of the 60/40 portfolio".

- The longer you invest, you realise that history indeed rhymes, but it doesn’t repeat itself. We have a recency bias where we anchor our expectations against what has happened most recently.

- The 60/40 portfolio has returned 8% annual return over the past decade withthe past 10, 15, 35 years all gravitate around the 7% mark. As investors, we should anchor our expectations longer-term historical evidence as opposed to recency bias.

- Click here to get started on your wealth journey with Endowus Hong Kong today and explore our 60/40 Flagship Portfolio.

.png)