.webp)

.webp)

.webp)

.webp)

- Tail risk is the small probability of extreme, portfolio-altering losses. While rare, these events typically do occur in the lifespan of an investment portfolio.

- Standard deviation - a conventional measure of volatility - only tells us the average magnitude of return fluctuations. To better understand risk, we need additional measures that allow us to project and calculate extreme drawdowns.

- However, the drawdown itself is rarely the decisive factor in long-run outcomes. What matters is whether the portfolio — and the investor — is positioned to stay invested through it and participate in the recovery that may follow.

What is tail risk in finance?

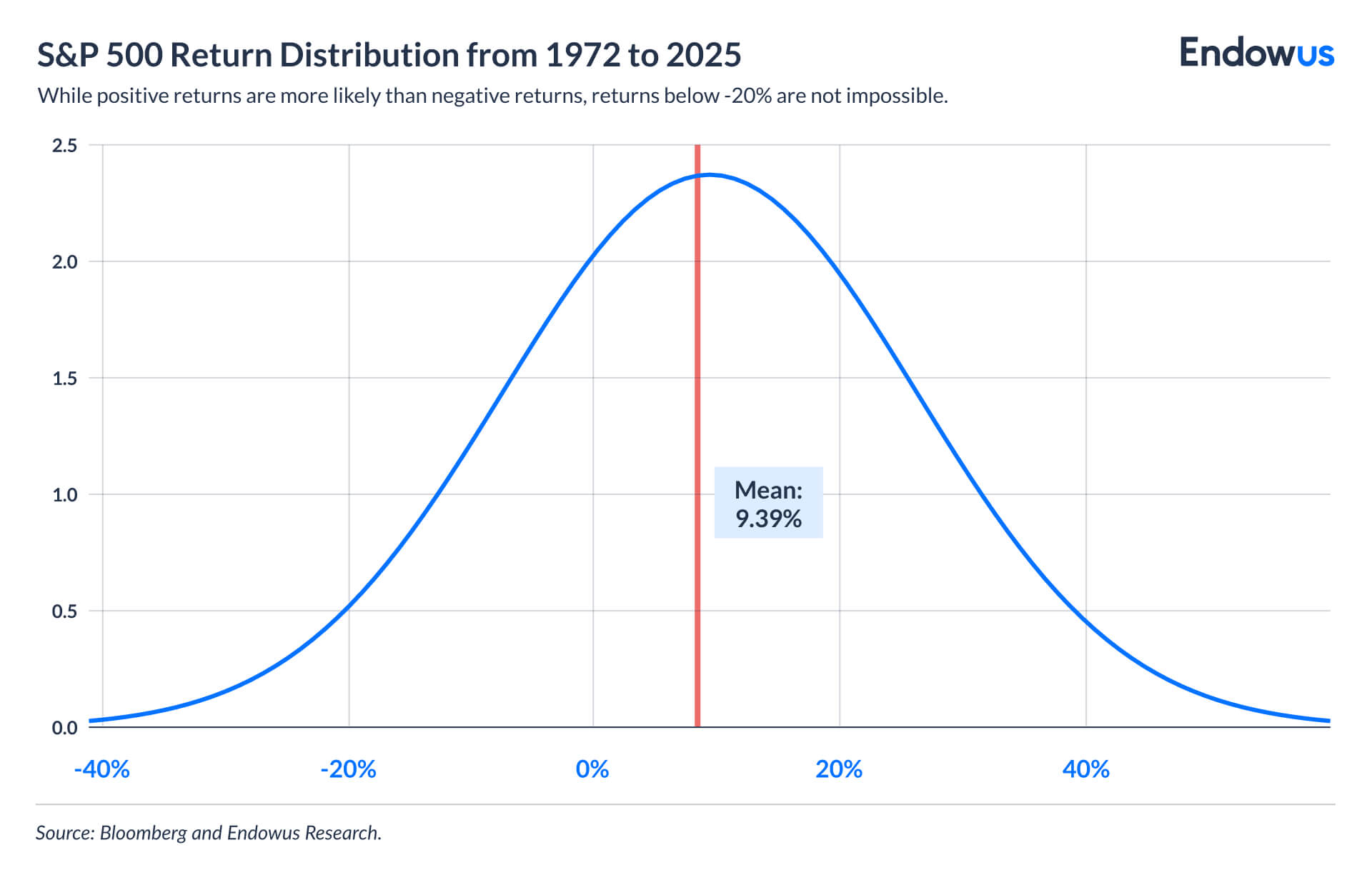

In statistics, the "tails" of a return distribution are the extreme outcomes at either end of the bell curve — events that are rare but, when they occur, are far larger in magnitude than everyday volatility (“standard deviation”) would suggest. Tail risk refers specifically to the left tail: the risk of severe negative returns.

Standard portfolio models often assume asset returns follow a normal distribution. In practice, financial markets exhibit what statisticians call "fat tails" — meaning extreme events happen more frequently, and with greater severity, than the models predict. The global financial crisis (GFC) of 2008, the Covid-19 crash of 2020, and the dot-com collapse of 2000–2002 were all, in theory, statistical outliers. In practice, they have each occurred within a single working lifetime. In the Asian context, an example of a statistical outlier is the 1997 crisis.

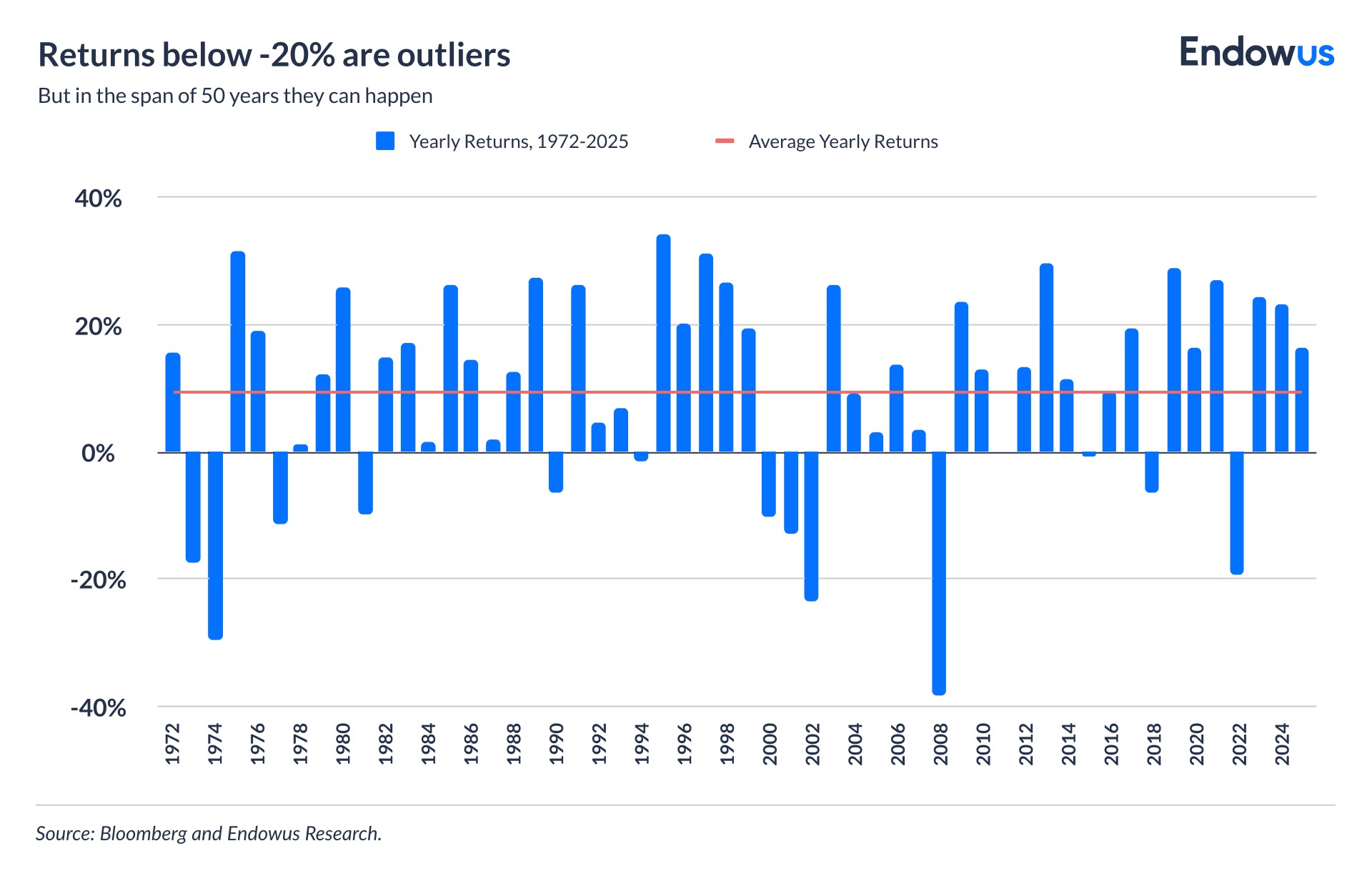

Looking at U.S. large-cap equity returns from 1972 to 2025 tail events, defined here as losses exceeding 20% in a single calendar year, have occurred three times. That is roughly one in every 18 years. For a 30-year investor, the historical record suggests they may encounter two such events over their investment horizon.

For the Hang Seng Index, volatility has been historically higher - it is less liquid than the S&P 500 - with higher mean returns, which means tail events in a strict statistical sense (two standard deviations, or -64.4%) never actually occurred. But large drawdowns (>25%) did happen at least five times since 1966.

Why conventional metrics fail to measure tail risk

The most widely used measure of portfolio risk is volatility, typically expressed as standard deviation. Volatility captures how much returns fluctuate around their average. It is useful, but incomplete.

The problem is that volatility treats upside and downside moves symmetrically. A year of +40% returns raises volatility just as much as a year of -40% losses - but fully recovering from a 40% loss requires a 65%+ return. More importantly, volatility says nothing about the shape of the tails - it cannot tell you whether losses of 30% or 40% are plausible, only that returns have tended to deviate from average by a certain amount.

Tail risk measures attempt to address this. Value at Risk (VaR) estimates the minimum loss an investor would expect to suffer in the worst 5% of outcomes, over a given period. Said otherwise: in any given year (or month, or day, depending on what we are calculating), there is a 5% probability that losses will be higher than the minimum. To actually calculate the loss we need Conditional Value at Risk (CVaR), also called Expected Shortfall, which estimates the average loss in the scenarios that fall beyond the VaR threshold.

While VaR and CVaR are also not perfect instruments, a combination of the two helps understand and calculate what happens to a portfolio during extreme events - something that standard deviation alone does not do.

Tail risk in a diversified portfolio

While diversification reduces unsystematic risk - the “idiosyncratic” risk of individual assets or sectors - it does not fully shield against the risk of extreme events. In fact, extreme events are by definition not just hard to predict, but also typically produce an environment where investors have few places to hide.

In a genuine market crisis, correlations tend to rise sharply. Assets that behaved independently under normal conditions can move together when conditions deteriorate. This was visible in 2008, when equities, credit, and real estate all fell simultaneously. Even some hedge fund strategies that were supposed to be market-neutral experienced significant losses. The only assets that provided meaningful protection were sovereign government bonds from highly rated issuers, gold, and cash - which are important in a diversified portfolio and serve exactly this purpose, to add protection in the event of an extreme drawdown.

In fact, diversification is crucial in any market condition. Across normal market environments, which represent the majority of the investment horizon, diversification delivers genuine risk reduction and return smoothing. In a tail risk environment, the portfolio sleeve that is invested in “safe assets” can potentially provide some protection against market losses.

Core principles of tail risk management

Tail risk management does not mean avoiding equity markets. It means building a portfolio that can potentially limit losses during extreme scenarios.

At Endowus, we incorporate some key principles into how we think about portfolio construction for our clients.

Genuine diversification across risk factors

Include exposures that may behave differently in a crisis, such as alternative strategies with low correlation to equity, and geographic diversification across economies at different points in the cycle.

Liquidity management

Tail events often coincide with forced selling - investors needing cash precisely when markets are most dislocated. Maintaining an adequate cash buffer or liquid reserve means a portfolio does not need to crystallise losses at the worst moment.

Maintaining a long investment horizon

Over most 10-year rolling periods in the historical record, U.S. large-cap equities have delivered positive total returns. The primary risk of a tail event is not the drawdown itself but the behavioural response of selling at the bottom and missing the recovery that follows.

The behavioural impact of tail events on investors

Tail risk is a practical portfolio design problem — one that has meaningful consequences for retirement outcomes, wealth preservation, and the ability to stay invested through market cycles.

In our view, the most important implication is behavioural. The investors who come closest to realising the long-run return of equity markets are typically those who build portfolios they can hold through a tail event without panic-selling. That means matching risk exposure to investment horizon and genuine loss tolerance - not stated risk appetite, which tends to be revised downward sharply in a drawdown.

It also means being honest about what diversification can and cannot do. A well-constructed multi-asset portfolio may reduce the severity of a tail event. Eliminating it entirely is neither realistic nor the goal — the goal is to ensure that when it arrives, the portfolio, and the investor, can withstand it.

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

This article is not intended to be relied upon as a forecast or research or investment advice, and should not form the basis of any investment or other decisions. The information contained herein is not intended, and should not be construed, as any legal, tax, regulatory, accounting or financial advice. If you would like investment, accounting, tax or legal advice, you should consult with your own professional advisors regarding your individual circumstances and needs.

The information in this article may not be suitable for all investors. You are responsible for any action that you take or decision that you make in reliance on any content in this article, and you agree that Endowus HK Limited (“Endowus”) is not liable under any circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a recommendation, offer or solicitation by Endowus or its affiliates to you to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction.

This is not intended to be an invitation or offer made to the public to subscribe for any financial product or to enter into any transaction.

Accuracy of Information

Whilst Endowus has made reasonable efforts to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or errors in any such information. Endowus does not warrant or represent that the information in this article is correct, accurate or reliable.

Opinions

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this article are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

This article has not been reviewed by the Securities and Futures Commission of Hong Kong.

.png)