.webp)

.webp)

.webp)

.webp)

.jpg)

- Investors nerves have been put to test as we step into March 2026, with U.S. and Israeli strikes on Iran sending crude prices surging and global capital markets into whipsaw.

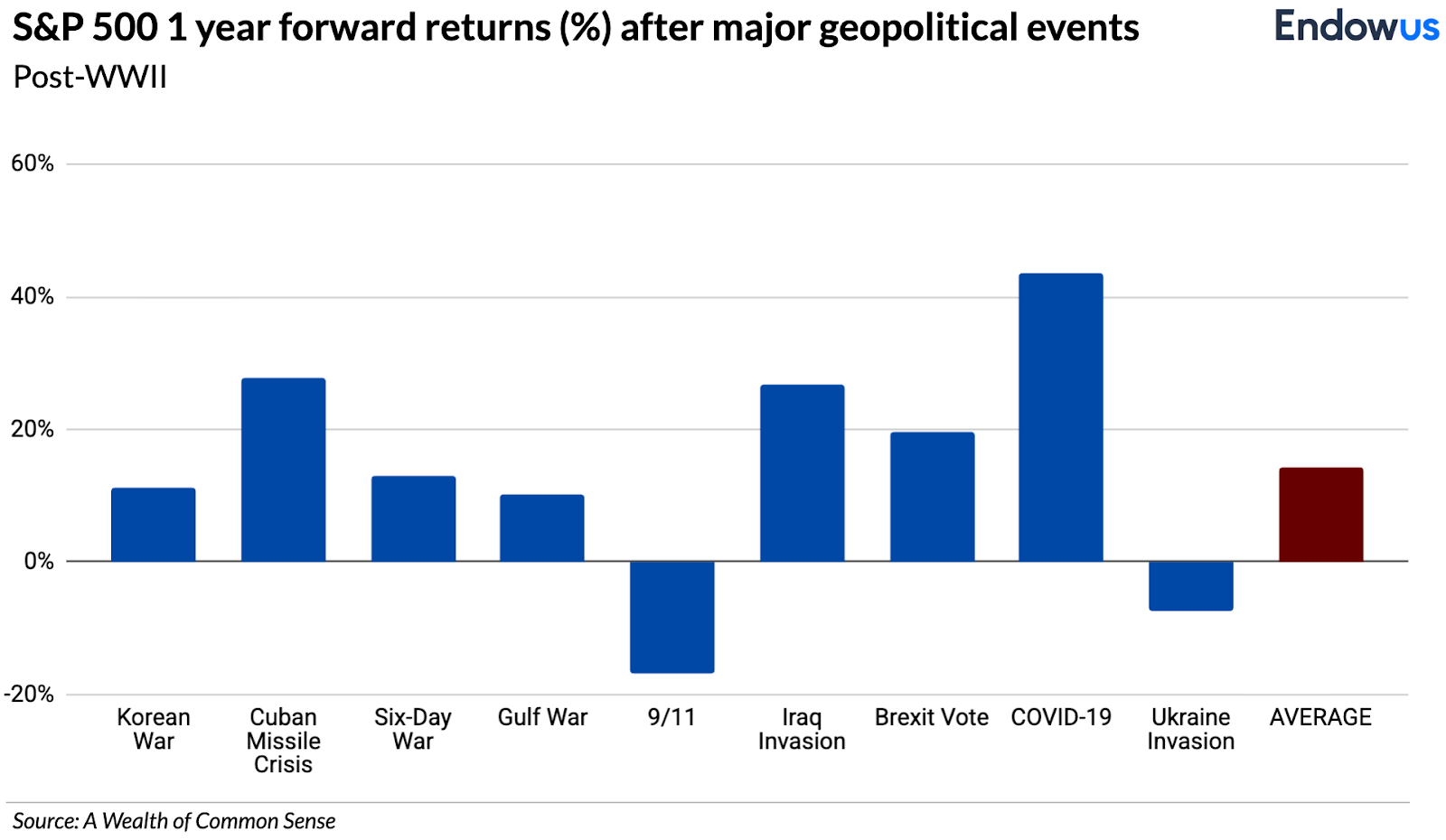

- Examining 40 major geopolitical events over 85 years, found that the S&P 500 lost an average of just 0.9% in the first month following a shock, then gained 3.4% over the subsequent six months. Markets ultimately respond to corporate earnings, economic growth, interest rates, and innovation — not the vagaries of geopolitical winds.

- In an evolving and uncertain market, the most effective response is a return to fundamentals — anchoring your portfolio in disciplined asset allocation and global diversification to navigate the cycle with confidence.

- Click here to get started on your investing journey with Endowus Hong Kong today.

This article was originally published in The Business Times. It has been adapted and updated by Endowus to reflect the specific economic context of the Hong Kong market.

The first week of March 2026 has rocked the markets and is currently testing investor nerves.

U.S. and Israeli strikes on Iran sent Brent crude surging above US$80 a barrel, shuttered Gulf airspace, and triggered circuit breakers from Seoul to Karachi. The world’s best performing stock market in Korea, the KOSPI, suffered its worst single-day crash since 2008, and the S&P 500 briefly fell more than 2.5%, though both markets rebound thereafter.

Gold spiked, the VIX jumped to 25, and treasury yields whipsawed as investors struggled to decide whether to fear inflation or flee to safety.

It is human nature to feel that this time is different and worse. But the science of wealth demands we look beyond the headlines and examine the evidence.

History's comfortable lesson

The relationship between war and financial markets is counterintuitive. The U.S. stock market rose a combined 115% during World Wars I and II. The Dow gained an annualised 16% through the Korean War and nearly 43% in total during the Vietnam era. During the Cuban Missile Crisis—thirteen days when the world stood on the brink of nuclear annihilation—the Dow lost just 1.2%, then gained over 10% by year-end.

This often happens because military and industrial spending rises alongside investments to rebuild infrastructure and arsenals, driving economic activity through a process of creative destruction.

The pattern is remarkably consistent. Research from Carson Group, examining 40 major geopolitical events over 85 years, found that the S&P 500 lost an average of just 0.9% in the first month following a shock, then gained 3.4% over the subsequent six months. According to Hartford Funds, stocks were higher one year after the onset of armed conflict roughly 70% of the time, with average returns in the high single digits.

The reason? Markets ultimately respond to corporate earnings, economic growth, interest rates, and innovation—not the vagaries of geopolitical winds.

The real risks seem to be elsewhere

That said, dismissing every concern would be naive. The Iran conflict matters primarily through one channel: oil.

The Strait of Hormuz carries roughly 13 million barrels per day—about 31% of global seaborne crude flows. Goldman Sachs estimates the market is pricing in approximately four weeks of disruption, with Brent trading roughly US$13 above the firm’s estimated fair value of US$65. If the conflict is short-lived, crude can simply be stored on land in Middle Eastern producing countries, leaving cumulative supply unaffected. But if the Strait remains disrupted beyond that window, prices could surge into triple-digit territory through forced demand destruction.

Should Brent sustain these elevated levels, central banks—including the U.S. Fed—may be forced into a “higher-for-longer” posture to combat reignited inflation. Consequently, the timeline for the next Fed rate cut has drifted significantly; markets now look towards June 2026 at the earliest, provided price pressures and geopolitical tensions abate.

For Hong Kongers, the energy crisis is transmitted directly through the HKD-USD linked exchange rate. The logic is clear: surging oil prices reignite global inflation, forcing the Fed to delay rate cuts to prevent overheating. While HIBOR does not always track the Fed in lockstep, the macro reality remains: a "higher-for-longer" Fed policy sets an elevated structural floor for local interest rates. Hong Kong residents will feel short-term pains from higher energy bills to potentially higher mortgage servicing costs with interest rates expected to remain elevated.

While geopolitical sparks in the Middle East inevitably ripple through to local living costs and rent cheques, it is still unclear whether these are longer term structural or temporary dislocation that will mean revert.

In an evolving and uncertain market, the most effective response is a return to fundamentals—anchoring your portfolio in disciplined asset allocation and global diversification to navigate the cycle with confidence.

The AI correction is a bigger story than Iran

Ironically, a more consequential market eruption was already underway before the first missiles flew. The so-called “SaaSpocalypse” of early 2026 has erased nearly US$1 trillion from the S&P 500 Software and Services Index, as the rise of agentic AI triggered a fundamental re-rating of per-seat subscription business models. Forward earnings multiples for the software sector collapsed from 39x to 21x in just six weeks.

The contagion has not stopped at software. Private credit firms with significant exposure to technology lending have seen share prices fall 9–16%. The U.S. equity market capitalisation now was sitting at nearly twice GDP, well above dot-com-era levels, and the Magnificent Seven still represented roughly 35% of the S&P 500.

An estimated half of data centre investment is funded through private credit, according to Morgan Stanley, creating a web of interconnected exposures that could amplify any reversal.

The Yale School of Management statistics showed that AI-related capital expenditure accounted for 1.1% of U.S. GDP growth in the first half of 2025, while AI-related stocks drove 75% of S&P 500 returns since the launch of ChatGPT in November 2022. This is not a sideshow. A significant correction in AI valuations would have macroeconomic consequences, potentially more durable than a four-week disruption to oil shipping lanes.

The macro overlay is still important

Layer these together and the picture for 2026 becomes more textured.

Valuations were already high entering the year. The Case-Shiller price-to-earnings ratio for the U.S. market exceeded 40 for the first time since the dot-com crash. Arguably it has been high for a while and yet the market kept rising, and of course, it can go higher and it did during the dot-com bubble, but the margin for error is smaller.

The S&P 500 traded at 23 times forward earnings versus 14 times for the FTSE—a historically wide gap that speaks to the premium embedded in U.S. equities and the concentration risk therein versus most other global markets.

A National Bureau of Economic Research study published in February 2026 found that despite 90% of firms reporting no measurable impact from AI on workplace productivity, investment continued to pour in at unprecedented scale.

This could be seen as the classic late-cycle cocktail: elevated valuations, concentrated market leadership, geopolitical uncertainty, and a narrative—AI—that has driven both real investment and speculative excess. However, just as we would caution against excessive optimism on the way up that led to concentration risk, we do not want to jump on the bandwagon of bashing all things AI.

Finally, as I wrote in the first Science of Wealth article of the year, there was almost unanimous positivity among all the talking heads of Wall Street. None of this means a major correction beyond this initial move is imminent. But it does mean that the margin of safety for investors was already narrow coming into the year, and that the Iran conflict has arrived at a moment when markets were already recalibrating.

What the historical evidence tells us to do

The science of wealth is about using data and evidence to make better decisions—not to predict the future, but to understand the range of outcomes and position sensibly within it.

The evidence tells us three things:

1. Geopolitical events, however frightening, have rarely derailed markets over the medium to long term. The initial shock is real but typically short-lived. Investors who sold during past crises almost invariably regretted it.

2. The true risk to watch is not the war itself but its second-order effects: a sustained oil supply disruption that reignites inflation and forces central banks to tighten further. This remains a tail risk, not a base case, but it demands monitoring.

However, a “higher-for-longer” Fed policy effectively anchors HIBOR at elevated levels, stalling any reprieve for local borrowers. This creates a structural floor for mortgage repayments while directly inflating utility surcharges. For Hong Kong residents, persistent rental inflation also remains a primary risk as financing burdens are passed from landlords to tenants. Until global energy markets stabilise and inflationary pressures subside, Hong Kong’s cost of living will remain inextricably linked to the geopolitical pulse of the Middle East.

3. The AI and software repricing is structural, not merely cyclical, and may prove more significant for portfolios than the geopolitical headlines dominating the news cycle.

For investors in Hong Kong and across Asia, the new prescription is unglamorous but time-tested: stay diversified across geographies, asset classes, and styles. Resist the urge to time markets around headlines. Ensure that your portfolio is not excessively concentrated in any single theme, however compelling. And remember that the cost of missing the recovery almost always exceeds the cost of enduring the drawdown.

Panic sells at the bottom, but the long arc of markets bends towards growth. This too shall pass. The question is not whether you will be invested when it does, but whether you were patient enough to stay the course.

Click here to get started on your investing journey with Endowus Hong Kong today. If you need guidance on your wealth journey, feel free to reach out to our team of SFC-licensed client advisors.

Read more:

- Stay invested in a downturn — these charts show why

- Afraid to invest? 3 Charts to ease your fears

- The power of diversification in investing

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

This article is not intended to be relied upon as a forecast or research or investment advice, and should not form the basis of any investment or other decisions. The information contained herein is not intended, and should not be construed, as any legal, tax, regulatory, accounting or financial advice. If you would like investment, accounting, tax or legal advice, you should consult with your own professional advisors regarding your individual circumstances and needs.

The information in this article may not be suitable for all investors. You are responsible for any action that you take or decision that you make in reliance on any content in this article, and you agree that Endowus HK Limited (“Endowus”) is not liable under any circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a recommendation, offer or solicitation by Endowus or its affiliates to you to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction.

This is not intended to be an invitation or offer made to the public to subscribe for any financial product or to enter into any transaction.

Accuracy of Information

Whilst Endowus has made reasonable efforts to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or errors in any such information. Endowus does not warrant or represent that the information in this article is correct, accurate or reliable.

Opinions

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this article are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

This article has not been reviewed by the Securities and Futures Commission of Hong Kong.

.png)