.jpg)

US exceptionalism: Midsummer night’s dream?

Many of us would remember that just a couple of months ago, the market was euphoric over the rally in US equities. The risks were known; the Magnificent Seven and the AI theme dominated the market, reaching as much as 35% of the total US equity market share at its highest. It's not like we didn't know it had to come off at some point.

However, not many investors expected US exceptionalism to start showing signs of cracking so quickly. Ever since DeepSeek emerged at the end of January, US markets have been bombarded with crisis after crisis, leaving them lagging behind the pack.

The question now is whether this is merely a short-term bump in the road or if US exceptionalism will fade away like a midsummer night's dream that ends too soon.

What’s behind the US market cracks?

A combination of factors is at play, including the emergence and threat of DeepSeek, increasing uncertainty surrounding the US administration's policy agenda, and weak economic data (such as a sluggish service sector, declining consumer and producer sentiment, and falling home sales) that has quickly re-priced the US growth outlook. Stagflation has also re-entered the conversation.

Sentiment has quickly changed from celebrating Trump’s promise of deregulation, tax cuts, and reduction in federal spending as a positive for equity markets to worrying about slower growth and sticky inflation as a result of tariffs, weaker consumer sentiment and federal job cuts.

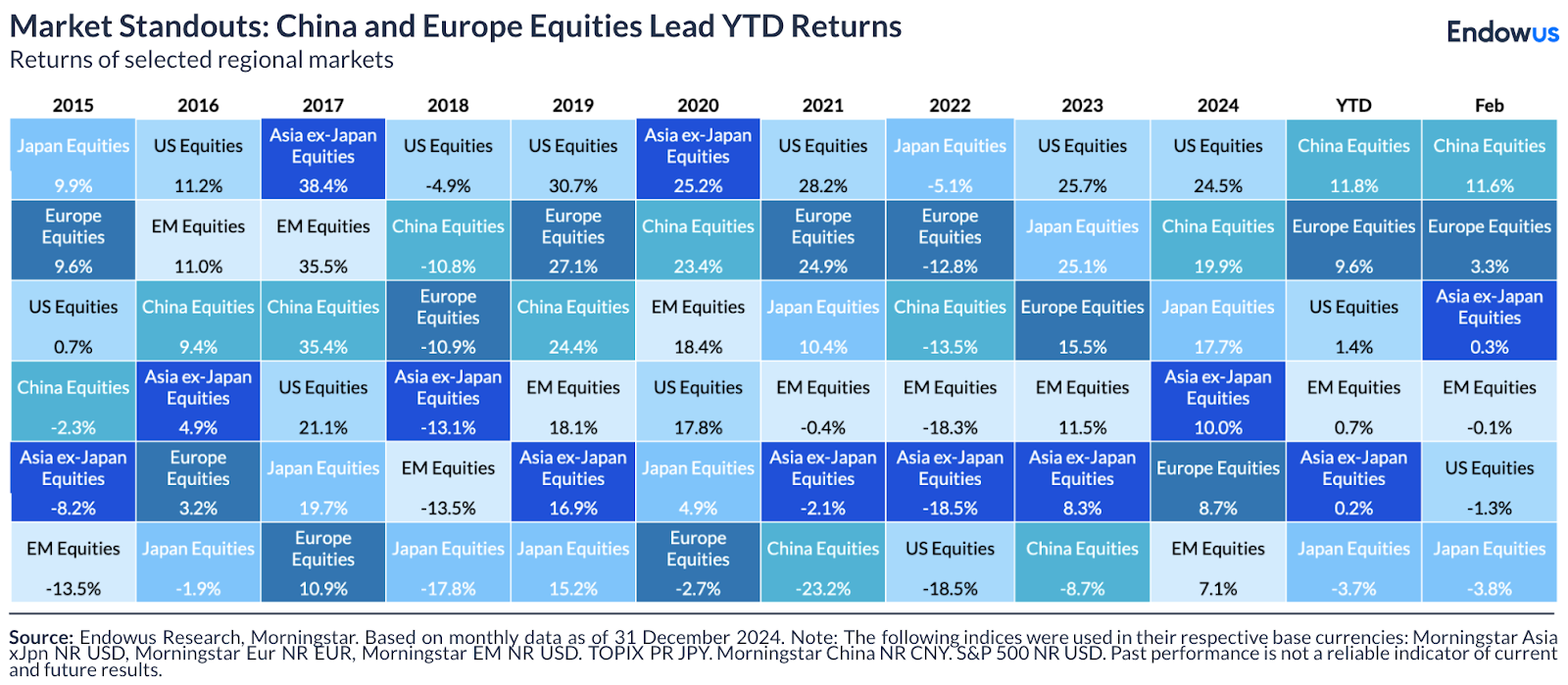

Europe and China on the rise

Other regions, particularly China, are seeing a divergence in returns from the US. Europe and Asia posted strong returns of 9.6% and 11.8% year-to-date, respectively (in USD, as of 28 Feb 2025) – in contrast to the negative returns in the US.

The rally in Europe is primarily driven by a recovery narrative. Expectations are high that the leadership change in Germany, Europe's largest economy, will pave the way for a new economic recovery.

Additionally, defence-related stocks are gaining momentum, fueled by hopes that increased defence spending and an end to the war in Ukraine could stimulate growth.

Capital is flowing accordingly. After years of near-consistent outflows, European equity funds are attracting the largest inflows since 2022, according to Bank of America figures, while the record inflows into US equities seen last year are drying up.

On the other hand, the rally in China feels like a familiar déjà vu, driven by "Chinese Magnificent Seven" companies such as Alibaba, BYD, and Tencent.

The Chinese government, which had previously been tough on technology companies, has also shifted its stance to one of comprehensive support. The excitement surrounding China’s low-cost, high-performance AI chatbot "DeepSeek" has further fueled the momentum of these stocks.

What now?

Never judge a book by its cover, though.

In the US, for example, not all stocks are down. Sectors such as healthcare, consumer staples, energy, and real estate have delivered healthy positive returns over the month. Notably, these are sectors traditionally classified as less growth-oriented and more value-oriented – often considered "recession-proof" sectors.

Similarly, in China, strong returns were concentrated in the export-focused offshore market. Concerns about the real estate market meant that GDP-sensitive domestic equities lagged.

As for Europe, the region's growth remains fragile. The continent is likely to face Trump's tariff threats soon. Germany's DAX experienced a sharp decline of 3.5% at the end of February – its steepest fall in exactly four years – as fears of a trade war unsettled global markets.

What’s in it for you?

The drivers of over- and underperformance in different regional markets are intriguing and can present exciting opportunities for investors, especially for those who enjoy analysing the markets and predicting future movements.

However, as we've seen in the past few months, it is extremely difficult to forecast the next winner. Consider your investment objectives and risk tolerance before deciding to allocate a significant sum of money to your next investment.

Global equity

The signs of a halt in US exceptionalism that emerged in January continued into February. US equities were weighed down by ongoing concerns about mega-cap tech, particularly following the developments around DeepSeek.

Despite this, there were bright spots within the US market as sectors such as consumer staples, energy, and real estate delivered healthy positive returns, showcasing some evidence of sector rotation amidst broader market concerns.

In contrast, Asian shares climbed 1.1% over the month, largely driven by an impressive 11.7% increase in Chinese equities in USD. The excitement surrounding DeepSeek's implications continued to lift the broader Chinese tech sector. On the other hand, Japan was an outlier in the region, with the TOPIX posting negative returns due to the yen appreciating against the dollar.

Meanwhile, European equities emerged as the top-performing major equity market, as investors started counting the days to a ceasefire in Ukraine.

Global fixed income

Fixed-income assets shone as risk diversifiers in February, navigating through a storm of market volatility. The month was marked by higher-than-expected January inflation data, weakening business and consumer sentiment, and the ongoing drama of tariff discussions with Canada and Mexico.

As rates generally moved lower, fixed-income assets reaped the benefits. Core bonds and longer-duration assets led the pack, while high-yield markets managed to stay positive but trailed behind their higher quality counterparts.

Commodities

In February, a slightly weaker USD and a rally in bond prices did not support most commodities, with declines seen across metals (silver, platinum, palladium), crude oil, coal, and agricultural products.

Gold proved an exception, as its bull factors remained intact, bolstered by fears of US tariffs boosting safe-haven demand.

The broad risk-off sentiments also impacted digital assets, with Bitcoin prices dropping by about 18% during February, while Ethereum saw a decline of approximately 32%.

Building a long-term resilient portfolio with Endowus Hong Kong

Nobel prize-winning economist Harry Markowitz called diversification "the only free lunch in finance".

Spreading your investments across asset classes and geographies will help with diversifying your risk. With market volatility comes opportunities. If you have a long-term investing horizon, as many of us do, these developments may offer an opportunity through steady, regular investing in diversified and risk-adjusted portfolios.

With the digital wealth platform Endowus, you can plan and manage your money — by investing in Best-In-Class Funds and globally diversified, low-cost model portfolios seamlessly.

Click here to get started on your investing journey with Endowus Hong Kong today.

Read more:

- Global trade in flux: The impact of US tariffs on China, Asia and beyond

- Top 8 convictions in the Year of the Snake

- Top 3 concerns of fund managers in 2025

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)

.png)