-p-1600.jpg)

- Individual investors are increasingly offered access to alternative investments, which were historically only reserved for institutional and ultra high-net-worth investors.

- Alternatives can offer potential benefits of diversification and enhanced portfolio resilience, but investors should be aware of trade-offs such as lowered liquidity and potentially higher fees. Return outcomes also depend heavily on strategy and manager selection.

- Allocation to alts should be tailored to individual risk tolerance, time horizon, and liquidity needs, not driven by headline returns alone.

- Endowus Hong Kong offers curated Best-In-Class private markets and hedge fund strategies for our Professional Investor clients. Contact us to learn more.

Alternative investments have moved from niche to mainstream – especially following regional regulators’ push. But for many investors, they still raise fundamental questions.

From return potential to risk perception, illiquidity to diversification, the world of private markets and hedge funds can feel opaque. This article tackles four of the most common questions beginners ask—offering clarity on performance, cost, portfolio fit, and allocation strategy.

Whether you're exploring alts for the first time or refining your understanding, this article will help answer the five most common questions.

1. Do private markets and hedge funds really generate higher returns?

Private markets are a motley crew, and so are hedge funds. They stand for a diverse collection of strategies, and this means their performance can vary significantly.

For private markets, the data from the past decade suggests that the strategies have generally delivered higher returns than traditional portfolios, though outcomes can vary widely by strategy and vintage. Private equity and private credit also appear strong, with returns around 15% and 10% respectively, and the latter offering notably higher yield than public markets. Plus, because investors commit long-term capital, they may earn an illiquidity premium from companies willing to pay more for stable funding.

Hedge funds present a more mixed picture—while some strategies can significantly outperform benchmarks at a given year, while others could also significantly underperform if directional bets went wrong.

The takeaway is that return outcomes vary widely across strategies, even within the same asset class. Performance depends heavily on manager selection and market conditions, making due diligence critical to success.

2. If private markets and hedge funds generate higher returns, should I allocate more of my portfolio into these assets?

The answer is not a simple yes or no. The decision is never about a blanket prioritisation of one asset class over another. While private assets can offer unique risk-return characteristics and potential benefits, it is crucial to consider a comprehensive set of factors before making any investment decisions.

Private markets can offer compelling return and yield profiles, they also come with trade-offs: illiquidity, longer investment horizons, higher fees, and greater dispersion in outcomes. Traditional assets still play a critical role in providing liquidity and transparency, especially in volatile or uncertain environments.

The optimal approach is about thoughtful integration, which is allocating to alternatives in proportion to one’s risk tolerance, time horizon, and need for diversification. Prioritising alternatives may enhance portfolio resilience and return potential, but only when balanced against the foundational strengths of traditional assets.

For instance, an investor with a very long time horizon – let’s say with decades until retirement – and a high tolerance for risk might find a carefully selected private equity allocation suitable, as they can absorb the illiquidity and potential short-term volatility for the prospect of higher long-term returns. Conversely, someone nearing retirement with a lower risk appetite and a need for more immediate access to funds might prioritise more liquid and stable traditional assets.

Your personal circumstances, financial objectives, and comfort with risk should always drive your allocation decisions.

3. I heard that private market strategies and hedge funds are expensive. Is that true?

Yes, they are generally more expensive, especially when compared to low-cost unit trusts and passive index funds. Performance-based fees are common. But the higher fees are not arbitrary. They reflect the complexity of strategies, reward skill and performance, open up access to exclusive asset classes, and in some cases, help align incentives between general partners (GPs), who manage the investments, and end-investors.

In hedge funds, fees are often structured under the well-known “2 and 20” model. A 2% management fee is charged annually on assets under management. A 20% performance fee is applied to profits, typically above a hurdle rate (a minimum return) and subject to a high-water mark, ensuring fees are only paid on new gains.

For private market strategies, an annual management fee is charged on committed capital for closed-ended funds and on net asset value (NAV) for evergreen structures. Another cost is carried interest, which is a share of the profits that fund managers earn only if the investment performs well.

That brings us to the question of “is it worth it?” These can be worth it if the strategies deliver net-of-fee alpha, diversification, and access to opportunities unavailable elsewhere. But the burden of proof lies with the GPs to deliver, and with you as the investor to assess whether the solution fits your broader goals.

4. Does the inclusion of private market investments help diversify my portfolio?

Yes, and to a varying degree.

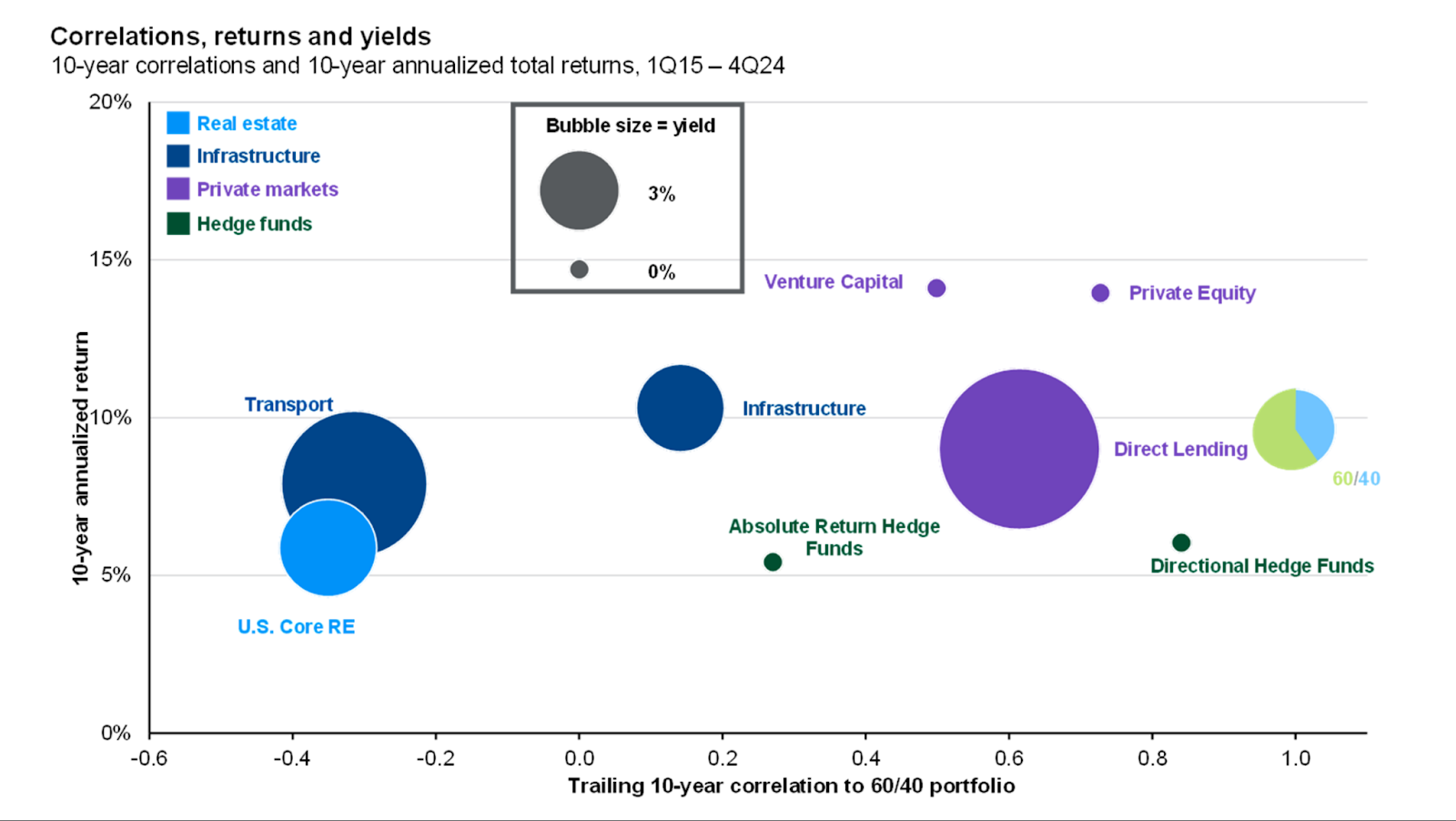

Several alternative strategies, particularly in real assets and private markets, show low to even negative correlation to a traditional 60/40 portfolio. Transport real estate and infrastructure, for instance, exhibit correlations near -0.3 and -0.1, respectively, while still delivering solid returns and attractive yields.

In contrast, some hedge fund strategies—especially directional ones—track closely with public markets, limiting their diversification benefit.

Similarly, private equity tends to be correlated with public equities, as both involve ownership stakes in companies and share the risk of capital loss when underlying valuations decline. They are also influenced by broader economic factors, including market conditions, company performance, industry trends, and macroeconomic shifts such as interest rate changes and inflation. While private equity may offer an illiquidity premium, its exposure to business cycles and company-specific risks often mirrors that of public equity.

The key is to analyse each alternative investment on its own merits and its expected behaviour relative to your existing portfolio.

5. Does the illiquidity of private market strategies and hedge funds make volatility irrelevant?

Illiquidity can obscure volatility, but it doesn’t eliminate it.

Private market strategies often report smoother return profiles due to pricing on a less frequent basis, often based on “events” such as the pricing of the latest fundraising round of the company. These methods of estimating the value of an asset can mask underlying market fluctuations. This perceived stability may offer psychological comfort during periods of public market stress, but it doesn’t mean the assets are immune to risk.

Economic downturns, shifts in credit conditions, or operational challenges can still materially impact performance—just not always in real time.

Hedge funds, depending on their strategy, may also exhibit dampened volatility, especially in less transparent or less frequently traded positions. Ultimately, while illiquidity can reduce mark-to-market noise, it doesn’t negate the importance of understanding the true risk embedded in these strategies.

Therefore, while the reporting of volatility might be less frequent due to illiquidity, the underlying risk of significant value changes remains very real and can be substantial.

Bonus round: I’ve heard semi-liquid or evergreen private market funds are more liquid than closed-end funds. How liquid are they, and how long does it take to sell my holdings?

Semi-liquid or evergreen private market funds offer more flexibility than traditional closed-end funds, but they are not fully liquid. These funds typically allow redemptions at monthly or quarterly intervals, often capped at a certain percentage of the fund’s net asset value.

Redemption request in advance will be needed, and investors should expect a phased exit if the request exceeds the fund’s redemption cap. In practice, it may take a few months to fully redeem your evergreen fund position—much faster than the 8-10 year lock-up of closed-end funds, but expect it to be still slower than liquidating public market assets.

Conclusion

Alternatives or not, the potential for higher returns is inherently tied to the assumption of risk.

Whether through illiquidity, complexity, or market exposure, every investment decision carries trade-offs. Private markets may offer compelling upside and diversification benefits, but they demand patience, selectivity, and a clear understanding of underlying risks. Hedge funds, too, can provide unique—yet their effectiveness depends heavily on strategy and execution.

Ultimately, the question isn’t whether alternatives are better than traditional assets, but how they fit within a broader, well-calibrated portfolio. Thoughtful allocation—grounded in objectives, time horizon, and risk tolerance—is what turns access into advantage.

Unlock exclusive access to alternatives with Endowus Hong Kong

Endowus offers exclusive access to alternative investment opportunities with global investment giants including Apollo, Blackstone, Carlyle, Macquarie, Oaktree and more to our Professional Investor clients.

If you are not yet a Professional Investor, opt-in today and to unveil access to leading alternative strategies. Contact us for a consultation or email us at privatewealth.hk@endowus.com to learn how you can hollistically consider incorporating alternatives into your portfolio.

Click here to get started on a better way to manage your wealth.

Read more:

- How alternative investments can fit into one’s portfolio

- Why become a professional investor in Hong Kong

- Understanding private credit

<divider><divider>

Risk Warnings

Endowus Alternatives, Endowus Private Wealth and the Wealth Implementation Plan are intended for Professional Investors in Hong Kong only.

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance or returns. Projected performance or returns is not guaranteed to materialise. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down. Individual stock performance does not represent the return of a fund.

General risk warnings relating to collective investment schemes

Before making an investment decision, you are reminded to refer to the relevant prospectus/ offering document for specific risk considerations and related fees and charges. Funds are not a bank deposit and not capital guaranteed, and is subject to investment risks, including the possible loss of the principal amount invested. Some of the funds also involve derivatives. Do not invest in them unless you fully understand and are willing to assume the risks associated with them.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors. Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus HK Limited (“Endowus”) and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus HK Limited, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. You may also wish to seek financial advice through a financial advisor or the Endowus platform and independent legal, accounting, regulatory or tax advice, as appropriate.

No invitation or solicitation

Nothing contained in this article should be construed as a solicitation, an offer to buy or sale, or recommendation, to acquire or dispose of any security, commodity, investment or to engage in any other transaction in any jurisdiction in which such solicitation, offer to buy or sale would be unlawful under the securities laws in such jurisdiction. No information included in this article is to be construed as investment advice or as a recommendation or a representation about the suitability or appropriateness of any advisory product or service; or an offer to buy or sell, or the solicitation of an offer to buy or sell, any security, financial product, or instrument; or to participate in any particular trading strategy. Investors should seek independent financial and tax advice before making any investment decision.

Product Risk Rating: Please note that any product risk rating (the “PRR”) provided by us is an internal rating assigned based on our product risk assessment model, and is for your reference only. The PRR is subject to change from time to time. The PRR does not take into account your individual circumstances, objectives or needs and should not be regarded as advice or recommendation to purchase, hold or sell any fund or make any other investment decisions. Accordingly, you should not solely rely on the PRR in making your investment decision in the relevant Fund.

This article has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)