.webp)

.webp)

.webp)

.webp)

.jpg)

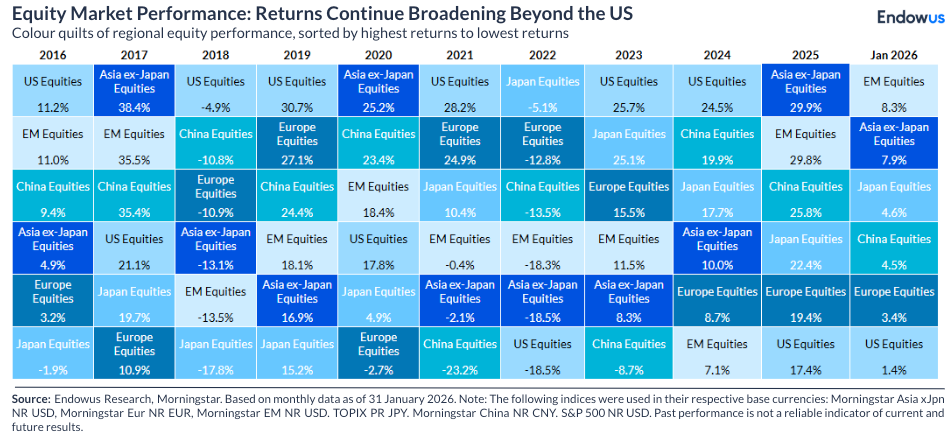

2025 was the first year in a long while where emerging market equities and non-US DM equities (i.e. Europe and Japan) outperformed US equities. Much of the same phenomenon continued in January with EM equities rising a whopping 8.3%. Korean equities, in particular, rose 23% for the month.

By sector, energy, materials and industrials led the way while technology lagged. As such, the broadening out of leadership by region (from US) and by sector (from tech) continued in Jan 2026.

Within the AI related segment, hardware and semiconductors remained firm but software struggled among valuation concerns and the risk that AI may disrupt certain SaaS industries.

In fixed income, the 10 year treasury yield rose 7 basis points to 4.24%. This move was driven by a “cautious pause” from the Fed and the nomination of Kevin Warsh as the next Fed Chair whom some view as more hawkish than other Fed chair candidates.

As for commodities, oil prices snapped a five month losing streak, jumping over 13% due to Middle East tensions and cold winter weather. However, the real story of the month was Gold and Silver which fell 16% and 39% respectively from its peak towards the end of the month due to a massive “unwind” caused partly by the nomination of Kevin Warsh. Gold and Silver still managed to end Jan higher by 13% and 19% respectively compared to the beginning of the month. With Oil, Gold, and Silver strong, commodities had one of its strongest months in the last 15 years.

The USD started the year in weakness with the DXY Index falling 1.4% for Jan. However, it found some support following the nomination of Kevin Warsh as Fed chair.

Global equity

By region, it was all about emerging markets with Korea (+23%), Brazil (+17%), Chile (+13%), and Taiwan (+11%) leading the charge. It was a mix of strength in semiconductors (Korea/Taiwan) and commodities in Latam markets that drove a big part of the strength.

Japan and EU markets were also strong, showing the broadening out of the equity rally into all major regions outside of the US market. Japan’s performance was helped by expectations of corporate reform and fiscal stimulus, thanks to the expected landslide victory at the early Feb snap elections (as of the time of writing, LDP had already won the election by a landslide and the Japanese equities market continued its strength in Feb).

In Europe, performance was spread across multiple sectors with Europe viewed as a “value” alternative to S&P500 and particularly US tech.

On a sector basis, the Energy sector was the best performing, driven by the surge in oil. Materials also continued their strength that started in 2025, driven by the performance of gold and other precious metals as well as the strength in copper. Industrials also performed well with sector leadership broadening out from technology. Even the consumer defensive sector which had been a big laggard in 2025 played catch up in Jan 2026.

.jpg)

Global fixed income

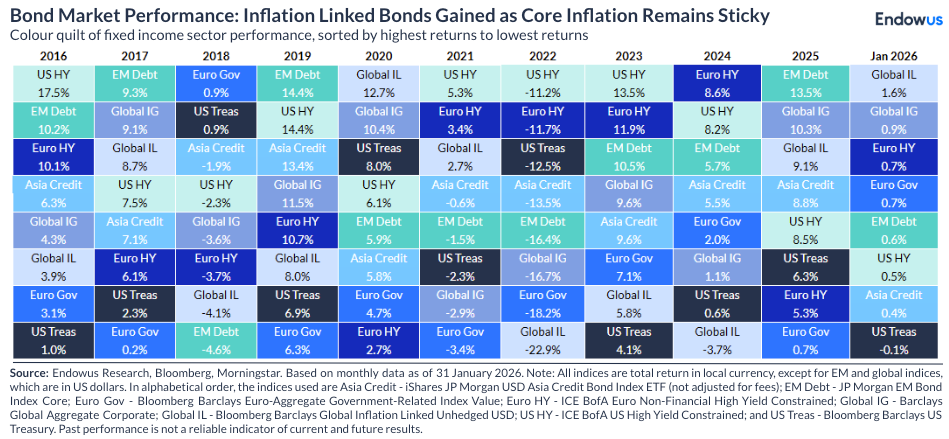

Global bonds saw muted performance during the month as better than expected economic data in the US led the Fed to keep its federal funds rate unchanged at the 3.5%-3.75% range, causing interest rates to rise.

Global investment grade and high yield bonds did better than treasury bonds, however, as credit saw solid performance on the back of positive US economic data that tightened credit spreads further. EM debt also continues to post solid numbers following a strong 2025.

Commodities

The Commodities index rose by 10% in Jan 2026, its strongest monthly move since Dec 2010. Many parts of the commodities index were strong with Gold rising 13%, Brent 16%, Natural Gas 18%, Crude 14%, Copper 4% and Silver rising 19%. These 6 commodities alone make up more than 40% of the index.

There seems to be higher demand for real assets including commodities following the stellar performance of Gold despite the fact that different commodities have very different supply responses.

We believe commodities can augment client portfolios as a satellite, but we do not encourage viewing them as core positions due to its lack of cashflow.

Building a long-term resilient portfolio with Endowus Hong Kong

Nobel prize-winning economist Harry Markowitz called diversification "the only free lunch in finance".

Spreading your investments across asset classes and geographies will help with diversifying your risk. With market volatility comes opportunities. If you have a long-term investing horizon, as many of us do, these developments may offer an opportunity through steady, regular investing in diversified and risk-adjusted portfolios.

With the digital wealth platform Endowus, you can plan and manage your money — by investing in Best-In-Class Funds and globally diversified, low-cost model portfolios seamlessly.

Click here to get started on your investing journey with Endowus Hong Kong today.

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

o invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)

.png)