.jpg)

- Q2 2025 marked one of the most rapid market reversals in history. Global equities fell more than 10% in the first few days of the quarter amid the fear and uncertainty surrounding “Liberation Day”. However, it rallied more than 23% from the bottom to end the quarter up 11.5%.

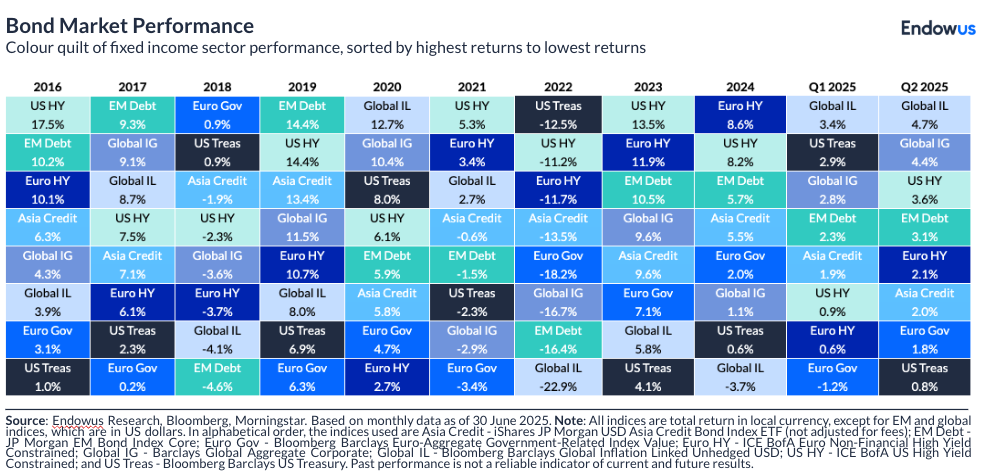

- As for bonds, the global aggregate index (on a hedged basis) rose 1.6% for the quarter, continuing two consecutive quarters of more than 1% returns. However, the bond market also had its share of drama as the 10 year yield rose more than 70bps during early April amid concerns over holding USD assets and investors asking for a higher term premium.

- The USD continued to drop in Q2, with the U.S. dollar index (DXY) falling 7% for the quarter. Concerns over USD dominance as well as fiscal debt (further exacerbated by the passing of the “Big Beautiful Bill”) caused the sell off.

- As equity markets have reached all time highs in early July, investors naturally question the sustainability of the rally. However, as we wrote in our article “Why are markets reaching new highs, while the USD stays weak?”, the market is driven by sales and earnings and often continues to make new highs.

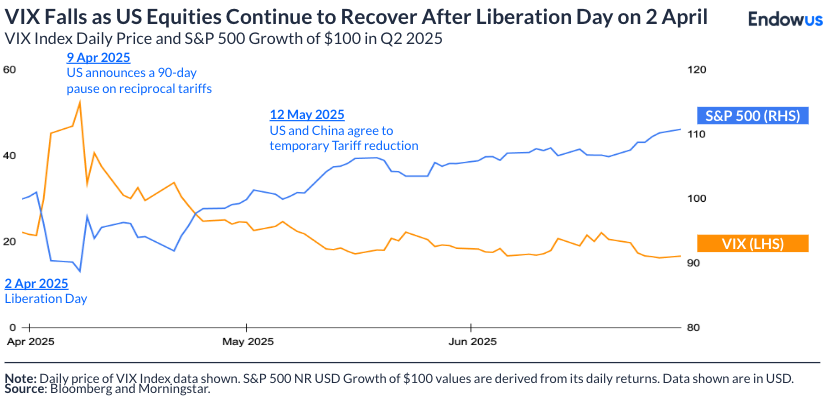

- Recent economic data has shown that the economy is holding up steady despite tariff concerns, and inflation is also within expectations. Moreover, uncertainties around tariffs seem to have come down as the market begins to digest the rules of engagement. As such, the VIX index has now firmly gone back to pre-Liberation day levels.

- This does not mean that it will continue this way, and unexpected events can always occur. However, if there is anything the market events in Q2 have shown us, it is that trying to time the markets is difficult and “time in the market” is much more important for long term wealth accumulation.

June and Q2 2025 Market Update

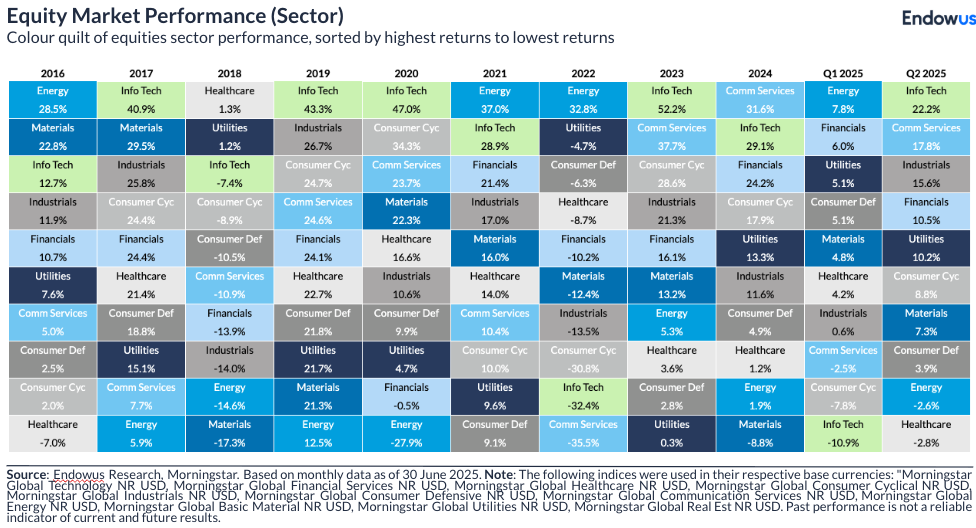

In Q2 2025, global equities, but more specifically the technology sector, made a big comeback after falling from Feb to early April. The emergence of DeepSeek, concerns over valuations, and a short-lived but impactful tariff induced sell-off saw the sector fall as much as 28% from mid February to early April. However, the sector recovered more than 40% from its lows in April to end the quarter +22% and reach an all time high. This was thanks to the sector’s continued display of strong earnings as well as the stronger than expected adoption of AI (for example, the DeepSeek event is perceived to be an accelerator of AI adoption and demand as opposed to a direct threat).

Fixed income also had a solid quarter, posting two consecutive quarters of +1% returns (on a hedged basis). However, under the surface, the asset class also had its share of drama with the JGB 30 year yields reaching multi decade highs of over 3% and the US treasury 30 year also rising 85 bps to a high of 5.15% in May as investors demand higher term premiums for long duration bonds.

Gold and silver gained in the second quarter; however, the magnitude of gains was considerably smaller than in the first quarter and more a result of USD weakness than anything else in our view.

Global Equity Market

While tech led the rebound in Q2 after being the worst performer in Q1, other sectors such as industrials also posted strong returns in Q2 as concerns over tariffs subsided.

The worst performing sectors were energy and healthcare. The former on geopolitical uncertainty and potential tariff induced trade disruption, and the latter on pricing concerns.

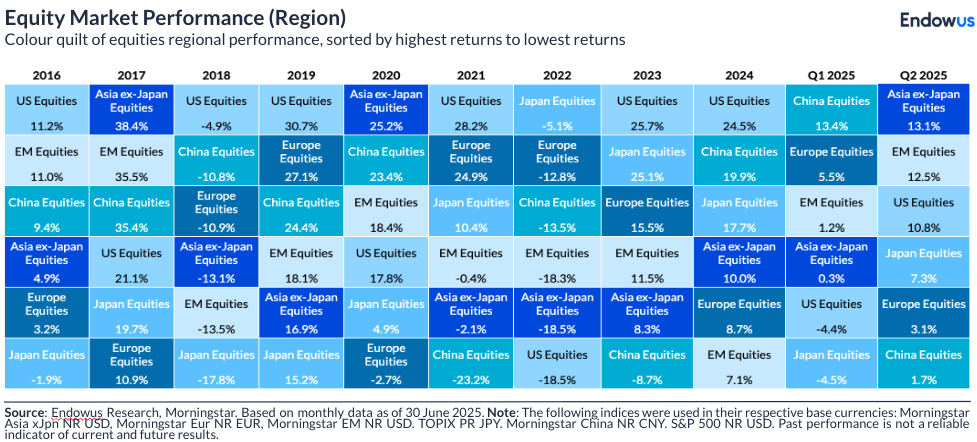

By region, Asia-ex Japan was the best performing region, led by Korea, which posted a +35% return in 2Q on a local currency basis. This was on the back of the election of President Lee, which is seen as an end to political uncertainty and also potentially positive reforms on the stock market alongside strong fiscal policy. China equities were the weakest performer after being the strongest performer in Q1, as we saw momentum subside.

Global Fixed Income Market

The Global Agg Index on a USD hedged basis returned +1.6% in Q2 after reporting +1.1% in Q1. On an unhedged basis, the Global Agg Index returned +4.5% and +2.6% respectively as dollar weakness helped performance. The best performing sub segment continues to be Global Inflation Linked Bonds, which rose 4.7% followed by Global IG, which rose 4.4%. The US treasury rose 0.8% for the quarter.

Building a long-term resilient portfolio with Endowus Hong Kong

It is almost impossible to predict exactly how macro events would play out. However, spreading your investments across asset classes and geographies will help with diversifying your risk. With market volatility comes opportunities. If you have a long-term investing horizon, as many of us do, these developments may offer an opportunity through steady, regular investing in diversified and risk-adjusted portfolios.

With Endowus, you can plan and manage your money — by investing in Best-In-Class Funds and globally diversified, low-cost model portfolios seamlessly.

Click here to get started on your investing journey with Endowus Hong Kong today.

Read more:

- Why are markets reaching new highs, while the USD stays weak?

- Multi-currency investments are now available: AUD, CAD, EUR, and GBP

- Endowus Q1 2025 Market Update and Outlook — Freedom or fallout?

<divider><divider>

Risk Warnings

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)

.png)