.webp)

.webp)

.webp)

.webp)

.jpg)

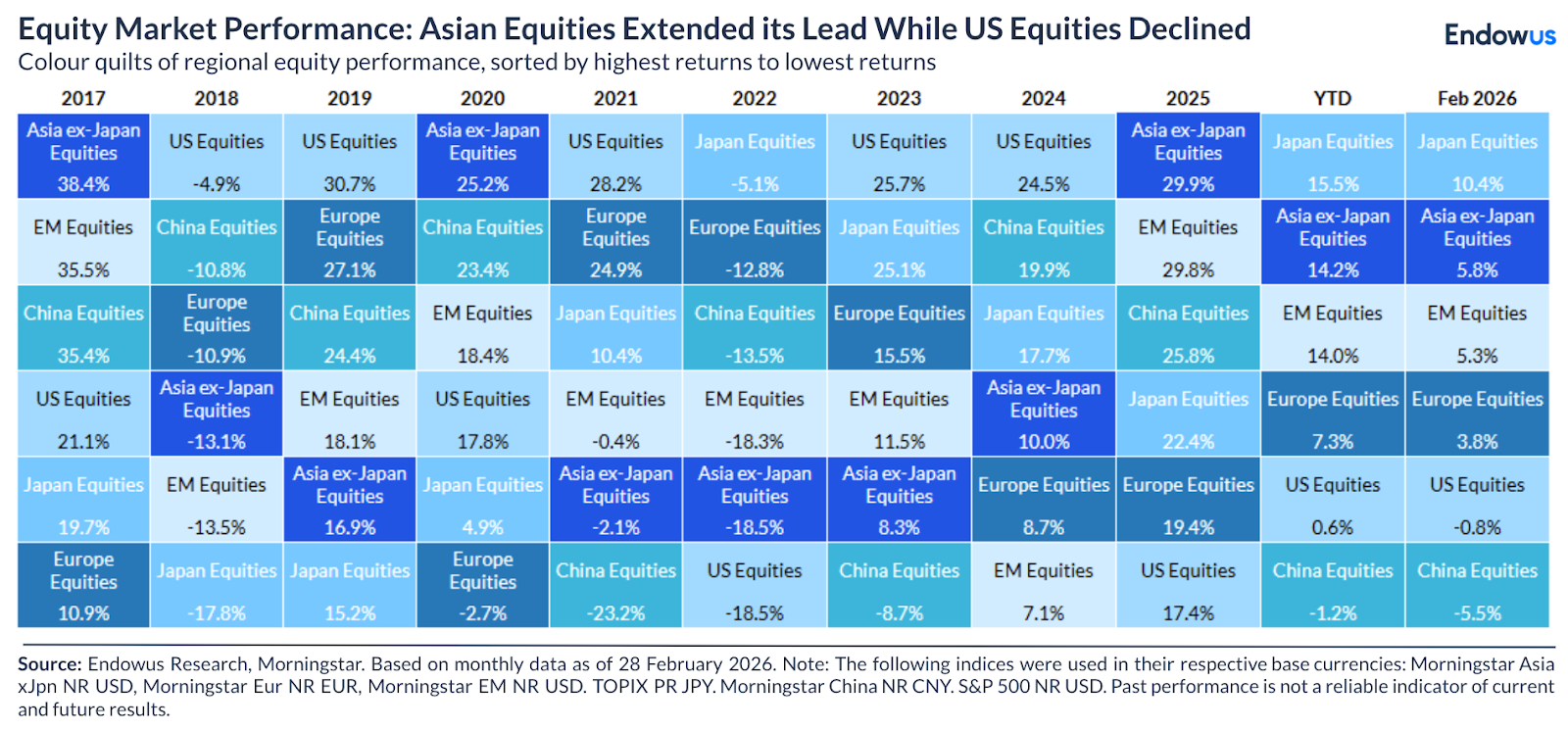

February saw the continuation of the non-US equity outperformance theme that dominated 2025 and carried into January, but with a notable shift in leadership within emerging and developed markets. While EM equities as a whole posted more modest gains compared to January's explosive 8.3% return, Asian markets surged on two landmark political events: Japan's historic snap election and continued momentum in Northeast Asia's semiconductor complex.

The big story of the month was Japan. In one of the most decisive electoral results since World War II, Prime Minister Sanae Takaichi's Liberal Democratic Party secured a two-thirds super-majority in the lower house, winning 316 of 465 parliamentary seats.

The market reaction was swift and powerful. The Nikkei 225 surged nearly 4% on the day of the result, crossing 57,000 for the first time, as investors priced in accelerated implementation of her pro-growth agenda: fiscal stimulus, a potential two-year food tax suspension, higher defence spending, and strategic investment in AI, semiconductors, and energy. The "Takaichi trade"—stronger equities, steeper Japanese government bond (JGB) curve, weaker yen—was firmly in motion by mid-month.

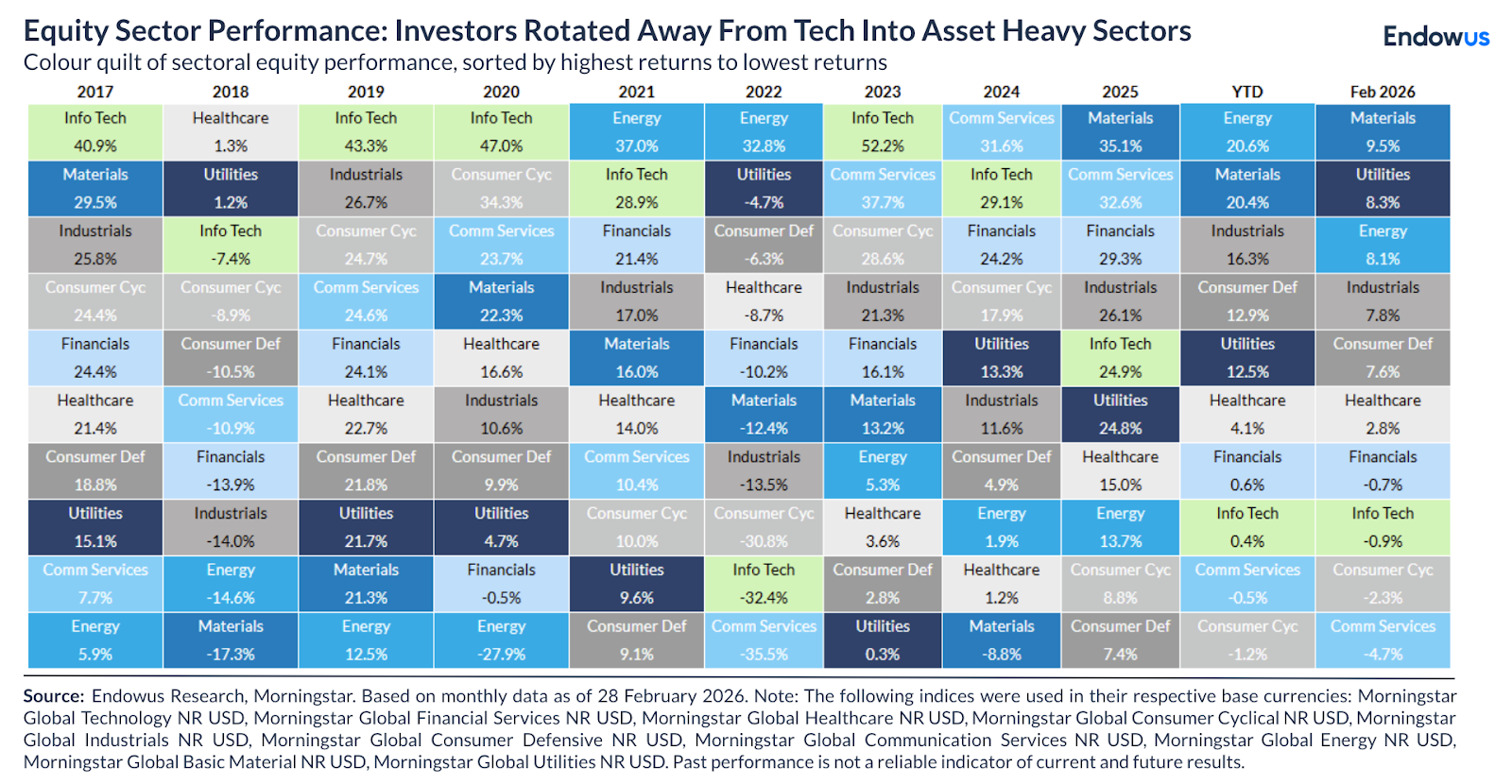

By sector globally, technology and hardware led in Asia while energy, materials, and industrials continued their relative strength in Western markets. The AI theme evolved in February: hardware and semiconductors remained firm, buoyed by Japan's strategic investment commitments and continued demand from hyperscalers, while software and SaaS faced renewed pressure from valuation concerns and growing fear of AI-driven business model disruption. The rotation from "AI enablers" to "AI adopters" continued as a key debate in markets.

On the US equity side, February was a notably weaker month. The S&P 500 declined approximately 0.9%, with the NASDAQ falling harder on AI-related concerns. Technology and financials—last year's biggest winners—were among the worst performers, as investors pivoted to energy, materials, and consumer staples.

A surprise reacceleration in the January PCE inflation data (released on February 27) triggered a broad risk-off sell-off to close the month, reinforcing the narrative of sticky inflation and slower easing. Global equities still managed a positive return of approximately 1.6% for the month, thanks to the strong performance of non-US equities.

Global equity

By region, Japan and Korea were the standout performers for February. The Nikkei hit multiple record closes throughout the month on the back of the Takaichi landslide, with investors broadening their attention from initial "Takaichi trade" winners (exporters, cyclicals, financials) to a wider basket including AI, semiconductors, defence, and renewables.

Meanwhile in Korea, KOSPI showed two consecutive months of 20%+ returns, largely driven by semiconductors. In March, however, KOSPI showed enormous volatility following the US-Iran war, suggesting FOMO buying in KOSPI leading up to February.

European equities held their ground, though with a more mixed performance than in January. The consensus view of European equities as a "value alternative" to the expensive S&P 500 continued to attract flows, supporting a strong year-to-date performance relative to US large caps.

US equities lagged the global pack. While the early part of the month saw some recovery in tech names from January's volatility, the late-February PCE shock triggered the S&P 500's steepest single-day decline in months. Value outperformed growth, and mega-cap technology concentration risk came back into focus. Small and mid-cap names held up better than large-cap growth on a relative basis.

By sector, energy continued its strong run as Middle East tensions kept oil prices elevated through much of the month before some softening on OPEC+ supply news. Materials remained firm, supported by gold and silver's continued upward momentum following the wobble in late Jan. Industrials held on to their broadening leadership theme.

In contrast, information technology was under pressure from AI disruption fears, particularly in software and SaaS, while financials also underperformed amid concerns about BDC credit quality and loan books concentrated in tech and software businesses.

These changes can be clearly seen in the HSTECH Index, which has shifted from excitement about AI to a focus on real profits. The OpenClaw (Lobster) agent system has grown rapidly, especially after it was adopted by Alibaba and Tencent Cloud. However, BOCI China warns that this industry is still very new, and it is unclear whether it will turn a profit. Along with tough competition and renewed trade tensions, these issues have caused investors to move their money from tech to biohealth and materials companies. In the future, the market may remain uncertain as investors grapple with changes within China and growing pressure from abroad.

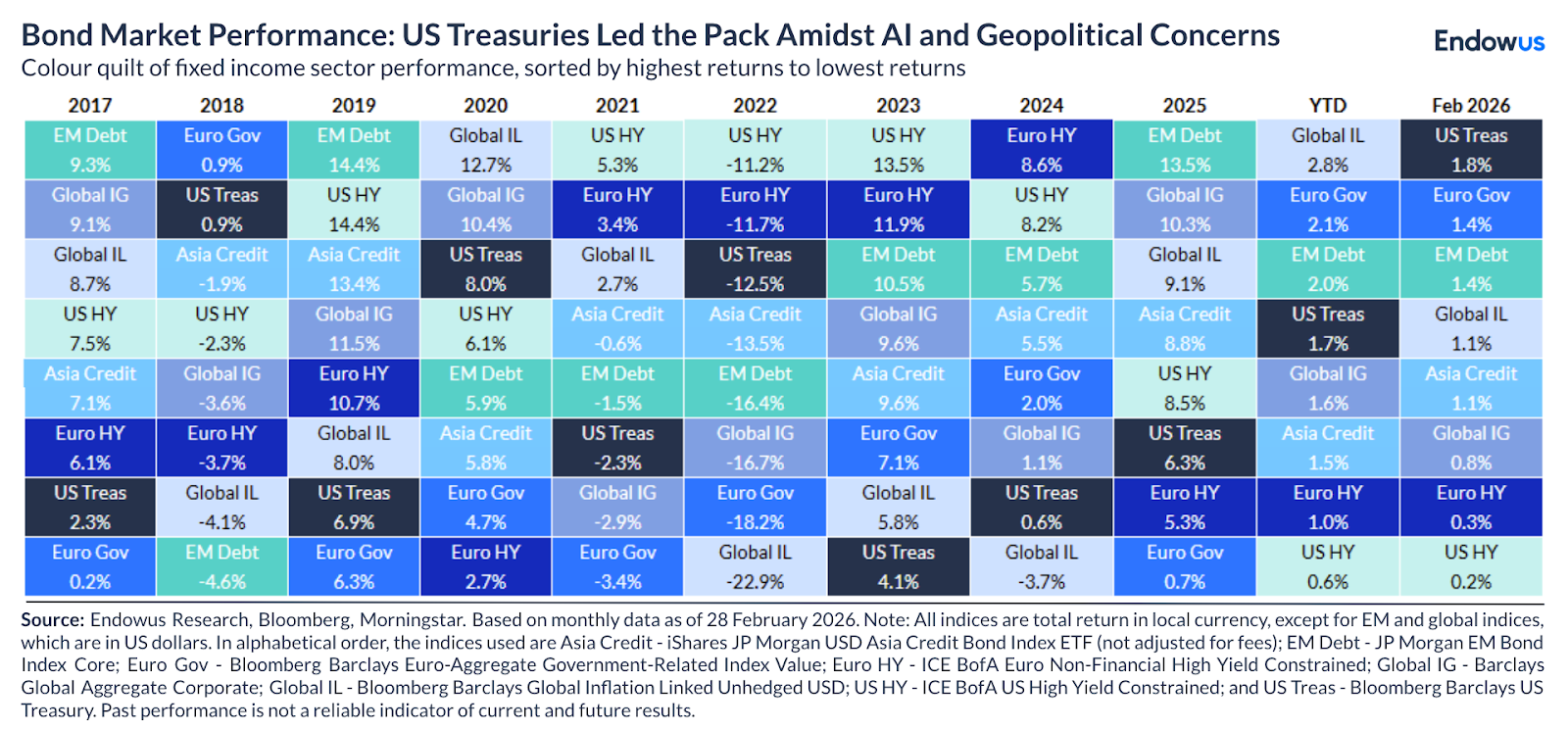

Global fixed income

The fixed income picture in February was more constructive than January, primarily because Treasury yields fell rather than rose. The 10-year US Treasury yield declined from approximately 4.24% at end-January to close the month at 3.9%, reflecting a rally in safe-haven assets in the second half of the month amid the risk-off move triggered by late-breaking Middle East tensions. The 2-year yield also fell around 15 basis points to approximately 3.4%.

Investment grade and high yield credit held up well in aggregate, supported by tight spreads and solid corporate balance sheets. However, credit spreads did widen modestly in the final days of the month as the equity sell-off and AI-related business model concerns, particularly around software and BDC portfolios heavy in tech lending, prompted a degree of risk-off repositioning.

EM debt continued to post solid numbers, supported by constructive global growth projections and ongoing appetite for carry in a world where EM central banks retain meaningful room to cut rates.

Commodities

Commodities were broadly flat for February—a sharp deceleration from January's exceptional 10% monthly gain. The key dynamic was divergence: precious metals continued their strong run while oil was more volatile, and ultimately softer as OPEC+’s production increase announcement kept a lid on prices even with brewing geopolitical uncertainty. Since the US-Iran war, however, Brent has spiked sharply higher on uncertainty of supply disruption from the Strait of Hormuz.

Gold gained a further 7.8% in February, reaching above US$5,200/oz and extending its year-to-date gain to approximately 22%. The drivers were consistent with prior months.

The USD found some support in February, posting its first monthly gain since October 2025, partly a function of safe-haven demand at month-end and some recalibration of rate cut expectations following the PCE surprise.

Staying long-term resilient with Endowus Hong Kong

Nobel prize-winning economist Harry Markowitz called diversification "the only free lunch in finance".

Spreading your investments across asset classes and geographies will help with diversifying your risk. With market volatility comes opportunities. If you have a long-term investing horizon, as many of us do, these developments may offer an opportunity through steady, regular investing in diversified and risk-adjusted portfolios.

With the digital wealth platform Endowus, you can plan and manage your money — by investing in Best-In-Class Funds and globally diversified, low-cost model portfolios seamlessly.

Click here to get started on your investing journey with Endowus Hong Kong today.

<divider><divider>

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Opinions

Whilst Endowus HK Limited (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a promotion, recommendation, solicitation, invitation or offer by Endowus or its affiliates to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This is not intended to be an invitation or offer made to the public to subscribe for any financial product or other transaction.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)

.png)