.webp)

.webp)

.webp)

.webp)

.jpg)

- Hong Kong investors can choose from brokerages, robo advisors, private banks, retail banks, and wealth management platforms such as Endowus — each with a different cost structure and approach to advice.

- The total cost of investing matters as much as the headline fee: trailer commissions, spread markups, and embedded fund margins can erode returns significantly over time.

- An evidence-based, long-term approach to investing — diversified across asset classes, and structured around your goals rather than the service provider’s product shelf — can potentially produce better outcomes for investors.

Many Hong Kongers who want to start investing struggle to choose between different options, and are often unable to make sense of what different types of advisors offer. Banks, brokerages, robo advisors, private banks, and wealth platforms have different value propositions that typically cater to different needs.

At Endowus, our goal is to guide investors - from the ones that are already knowledgeable to the ones who are just starting to familiarize with financial markets - to build long-term wealth, and help them avoid some of the common mistakes that contribute to less than desirable outcomes. These mistakes typically involve excessive trading, attempting to time the market, and chasing investment fads for fear of missing out.

In order for our readers to make informed decisions, in the following sections we will highlight the different services provided by market players in Hong Kong, while paying close attention to the incentives behind their product offerings.

What are your options for investing in Hong Kong?

Hong Kong has one of the most diverse financial ecosystems in Asia. Investors have choice across distinct platform types, with some structural differences.

Online brokerages - such as Interactive Brokers (IBKR) and Futu - will give you direct access to stocks, exchange-traded funds (ETFs), and options with low or zero commissions per trade. They are built for execution, but do not provide investment advice. If you know what you want to buy and are comfortable managing your own portfolio, they can be cost-effective. But they offer no guidance, no financial planning context, and no managed portfolio construction.

This is especially problematic for long-term focused investors who want guidance based on their goals. But it is even more important for investors with limited experience and resources, who should not be suitable to take short-term trading risk.

Robo advisors such as Syfe and StashAway automate portfolio allocation and rebalancing. They are typically lower cost than private banks and more friendly to beginner investors than brokerages. Robo advisors have been particularly successful, namely in offering better diversification and guidance for the mass market - at least compared to brokerages. However, their product universes tend to be more limited, mostly offering proprietary model portfolios and access to ETFs, but no exposure to the broader institutional fund market, or human guidance.

Read more: What is a robo advisor and why Endowus is different

Retail banks offer investment products through physical branch and digital banking platforms. While there may be a convenience factor for existing clients, banks typically retain trailer fees (sales commissions for distributing products) paid by fund managers, which may create a conflict of interest when it comes to product curation. In addition, those with in-house asset management arm may also have a bias toward own or affiliated products.

On the high-end of the spectrum, private banks serve high-net-worth clients, typically starting at US$1 million or more in assets under management (AUM). Product offerings may be comprehensive, with access to a diverse range of products. But bundled advisory fees and relationship manager incentives add a degree of opacity that may decrease - not help build - trust.

Separately from these models, Endowus was built as a wealth management platform that combines a technology layer with human advice and institutional-grade due diligence to make evidence-based, long-term investing accessible to a broader range of clients. Unlike traditional advisors, Endowus operates on a fee model that does not rely on product commissions, which helps align the firm's interests with those of its clients. Investors can access institutional share classes at retail investment sizes, and any trailer fees received from fund managers are returned in full to clients.

How to compare investment platforms: what actually matters

Not all fees are visible, and not all platforms disclose the total cost of investing in a single number. These are the four dimensions that most materially affect your long-term returns.

Total cost of investing: The relevant figure is not just the platform fee, but the fund cost, foreign exchange spread, and any trailer fees retained by the platform. A platform charging 0.3% in access fees while returning trailer commissions to you may cost less in total than a platform showing 0% commission while increasing the bid/ask spread for a foreign currency trade.

Conflict of interest: Who gets paid when the platform recommends a product? Quota-driven relationship managers, platforms that retain fund commissions, and banks that prioritise their own product shelf all face structural incentives that can work against your interests. A fee-only model — where the platform earns only a flat asset-based fee and rebates everything else including commissions — eliminates this conflict by design and creates alignment with the client interest which, in financial advice, should be the only one that matters.

Fund access and quality: Not all funds available to retail investors are created equal. Institutional share classes of the same underlying fund typically carry lower management fees than retail equivalents. Platforms that obtain to reduce fees to the institutional minimums for their clients can deliver a genuine cost advantage over time. This is especially true since fee reduction is a sure source of returns for investors, unlike financial returns.

How to build a long-term investment portfolio in Hong Kong

Portfolio construction for long-term wealth accumulation follows a small number of well-established principles, regardless of where you invest.

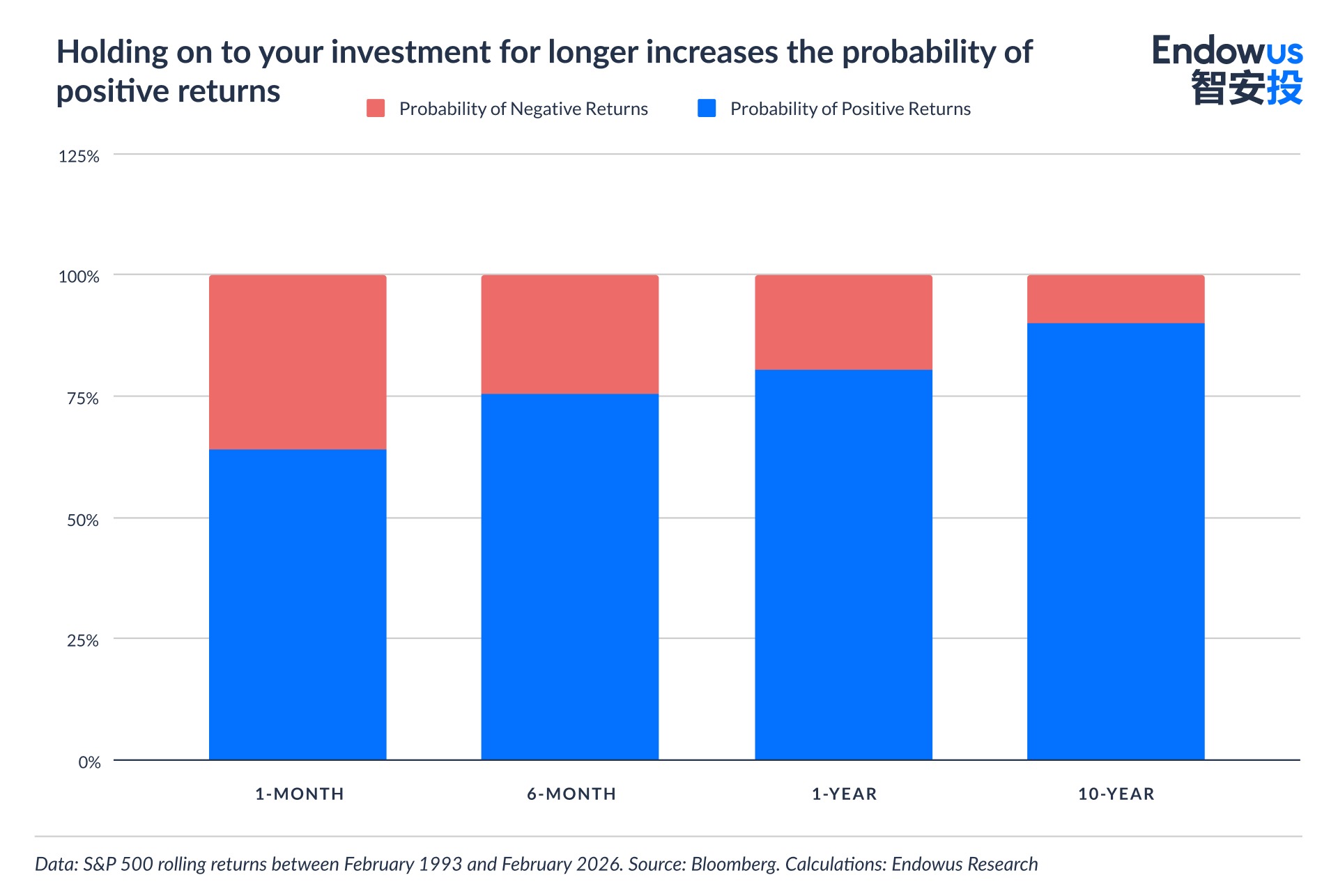

Start with your time horizon and risk tolerance. If you are investing for retirement 20 or more years away, you can typically accept higher short-term volatility in exchange for the potential for higher long-run returns. If you are investing for a goal in five years, your allocation to volatile assets should be commensurately lower.

Diversify across asset classes and geographies. A globally diversified portfolio — covering developed markets (US, Europe, Japan) and emerging markets — reduces concentration risk. Bonds and alternative assets can potentially further reduce portfolio volatility.

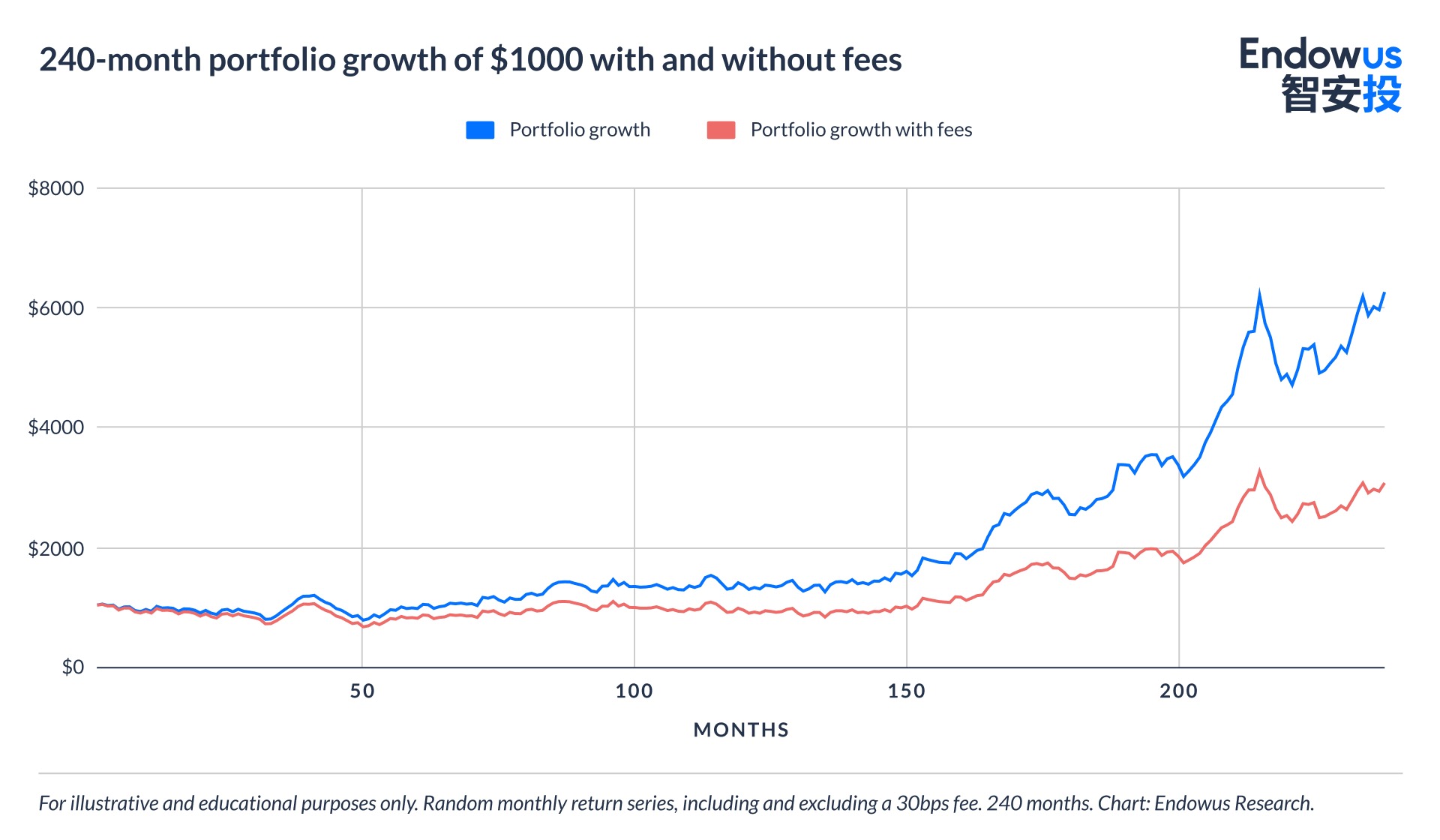

Minimise costs. Over a 20-year horizon, a 0.3% difference in annual fees can make a substantial difference in a portfolio’s terminal value. Access to institutional share classes with typically lower pricing, combined with a platform that does not retain trailer fee commissions, can compound this advantage.

Read more: Mutual fund fees are a mystery — they shouldn't be

Rebalance regularly. A target asset allocation drifts over time as different assets grow at different rates. Periodic rebalancing maintains the intended risk profile and imposes a systematic discipline on the portfolio. Our platform triggers an automatic rebalancing - subject to client’s approval - when a portfolio drifts ≥15% from its target allocation, and the IO will conduct periodic reviews and may initiate - based on its investment views - Recommended Portfolio Changes (RPC), which involve switching funds in advised portfolios after Investment Committee approval.

Invest consistently. Attempting to time the market consistently tends to destroy value relative to staying invested. Dollar-cost averaging — investing a fixed amount at regular intervals regardless of market conditions — reduces the risk of investing a lump sum at a market peak.

Why evidence-based investing matters

Technology-driven investment platforms often market themselves on user experience and app design. These features facilitate advisory services and portfolio construction. But in the field of financial advisory, competent human input is particularly important to build trust.

Separately, platforms that earn revenue from product commissions, fund management margins, or spread markups may have a financial incentive to prioritise products that generate higher fees for them, not products that are best for you. This misalignment can compound over decades.

An evidence-based investment philosophy — grounded in decades of academic research from institutions such as Dimensional Fund Advisors, and the broader finance academy — consistently points in the same direction: broadly diversified, low-cost, long-horizon investing outperforms tactical, high-fee alternatives for most investors.

Investment implications

For investors in Hong Kong who want to build long-term wealth, the key decision is setting up their strategic asset allocation - which needs to take into account their time horizon(s) for each one of their long-term goals, as well as their risk appetite and profile. These are primary considerations that should be discussed before any investment decision is made, in the context of the investor’s onboarding.

We built Endowus so that we could guide investors through these extremely important choices - before deciding “what” to invest in, figuring out “why” am I investing and with what ideal outcome in mind. These require human advisory, which Endowus provides.

Hong Kong investors may work with a bank because of the convenience of an existing relationship, but potentially suffer from the cumulative effect of embedded fees and conflicted product recommendations. They may pick a robo advisor, but this would not give them access to human guidance, or sophisticated due diligence. Or they may choose to “do it themselves” and use a brokerage, but in addition to potentially hidden fees, they may neglect a holistic, long-term approach to investing.

Endowus is built specifically to intercept the existing demand for evidence-based, long-term investing, and further aims at educating as many investors as possible on the advantages of thinking in those terms. It offers access to institutional-class funds and returns all trailer fees to clients.

Investors who want to understand whether their current platform is genuinely working in their interests can schedule a free consultation here.

Frequently asked questions

How much money do I need to start investing in Hong Kong?

Most online brokerages and robo advisors have low or no minimum investment requirements. Retail bank investment products often have product-level minimums. Wealth management platforms like Endowus have lower entry points, with no requirement to meet the typically high AUM thresholds required by private banks.

Is investing through a Hong Kong bank or online platform safe?

Regulated platforms — including banks, brokerages, robo advisors, and wealth platforms such as Endowus — are all licensed entities with the Hong Kong Monetary Authority (HKMA) and/or the Securities and Futures Commission (SFC) for the activities they conduct.

Hence, it is important to verify the platform you are considering is a fully regulated entity through official databases maintained by HKMA and SFC.

Once verified, when choosing a platform of choice, factors to consider include cost structure, potential conflict of interest, and advice philosophy — which affect outcomes over time.

What is a trailer fee and why does it matter?

A trailer fee (also called a trail commission) is an ongoing fee paid by a fund manager to a distributor — such as a bank or platform — for distributing their fund to investors. Most banks and many platforms retain this fee as revenue. Endowus returns all trailer fees received from fund managers back to investors, which reduces the effective annual cost of the portfolio and generates interest alignment between the advisor and the investor.

What is an institutional share class and why does it matter?

Institutional share classes carry lower management fees but are typically only accessible to investors meeting large minimum thresholds. Endowus clients qualify for institutional share classes, allowing them to benefit from fee levels normally reserved for large institutions.

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance or returns. Projected performance or returns is not guaranteed to materialise. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down. Individual stock performance does not represent the return of a fund.

General risk warnings relating to collective investment schemes

Before making an investment decision, you are reminded to refer to the relevant prospectus/offering document for specific risk considerations and related fees and charges. Funds are not a bank deposit and not capital guaranteed, and are subject to investment risks, including the possible loss of the principal amount invested. Some of the funds also involve derivatives. Do not invest in them unless you fully understand and are willing to assume the risks associated with them.

Opinions

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endowus HK Limited (“Endowus”) and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus HK Limited, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. You may also wish to seek financial advice through a financial advisor or the Endowus platform and independent legal, accounting, regulatory or tax advice, as appropriate.

No invitation or solicitation

Nothing contained in this article should be construed as a solicitation, an offer to buy or sell, or recommendation, to acquire or dispose of any security, commodity, investment or to engage in any other transaction in any jurisdiction in which such solicitation, offer to buy or sale would be unlawful under the securities laws of such jurisdiction. No information included in this article is to be construed as investment advice or as a recommendation or a representation about the suitability or appropriateness of any advisory product or service; or an offer to buy or sell, or the solicitation of an offer to buy or sell, any security, financial product, or instrument; or to participate in any particular trading strategy. Investors should seek independent financial and tax advice before making any investment decision.

Product Risk Rating

Please note that any product risk rating (the “PRR”) provided by us is an internal rating assigned based on our product risk assessment model, and is for your reference only. The PRR is subject to change from time to time. The PRR does not take into account your individual circumstances, objectives or needs and should not be regarded as advice or recommendation to purchase, hold or sell any fund or make any other investment decisions. Accordingly, you should not solely rely on the PRR in making your investment decision in the relevant Fund.

This advertisement has not been reviewed by the Securities and Futures Commission or any regulatory authority in Hong Kong.

.png)