.webp)

.webp)

.webp)

.webp)

- Wealth held predominantly in Hong Kong equities, property, and Hong Kong dollar (HKD) cash is not sensitive to three independent sources of return, as all three are tied to the mainland Chinese economy and, through the dollar peg, to US monetary conditions.

- That shared exposure shows up when it matters most: the Hang Seng Index has fallen more than 35% on five separate occasions, and in Hong Kong’s recent downturn local equities and residential property declined together rather than offsetting each other.

- Hong Kong investors who are not US tax residents face a 30% US withholding tax on dividends from US-domiciled funds, which makes fund domicile a material consideration when building diversified exposure.

Most Hong Kong households hold their wealth in three places: locally listed equities, residential property, and Hong Kong dollar (HKD) cash. This exposure appears diversified—it is, after all, a set of different asset classes. A better understanding of portfolio risk, however, would highlight correlations between these assets’ returns, which in turn would argue in favor of real diversification.

The problem is not simply that Hong Kong equities are volatile, though they are: the Hang Seng Index (HSI) has an annualised volatility of close to 28% over five decades. More in depth, all three of those holdings appear to answer to the same forces—the mainland Chinese economy, and US monetary conditions transmitted through the dollar peg.

This article sets out why a portfolio anchored in Hong Kong is more concentrated than it appears, what that concentration has cost investors historically, and how to build genuine diversification across geography, asset class, currency, and fund structure. For the full return and drawdown record behind this argument, our companion guide to the Hang Seng Index’s historical returns and volatility documents the 52-year picture.

Why concentration risk is high in Hong Kong

Outside of cash, most private wealth in Hong Kong sits in two places: locally listed equities and residential property. They are usually treated as separate holdings. In risk terms, they are closely related.

The HSI is not a diversified proxy for global growth. It is a concentrated instrument. Its top 10 constituents account for close to 50% of index weight, and a large share of the index comprises mainland Chinese financial, technology, consumer, energy, and telecommunications companies listed in Hong Kong. An 8% single-stock cap limits the influence of any one name, but it does nothing to reduce the index’s underlying tilt toward Greater China corporate earnings and Chinese policy.

That tilt is the transmission mechanism. When mainland macroeconomic conditions deteriorate, or when regulatory sentiment toward a major sector shifts, the effect flows through most of the index.

The 2021–2023 selloff illustrates the point. Beijing’s regulatory tightening across technology, education, and property, compounded by the Evergrande debt crisis and rising global interest rates, drove the HSI down approximately 49.6% from its May 2021 peak to its October 2022 trough, with three consecutive years of negative price returns.

Hong Kong property moved in the same direction, and for overlapping reasons. The Rating and Valuation Department’s private domestic price index fell roughly 28%, from 398.1 in September 2021 to a trough of 284.9 in March 2025. An investor holding both local equities and residential property took losses on both sides at the same time—precisely because both were exposed to the same underlying driver.

This was not a one-off. The HSI has recorded five peak-to-trough declines of more than 35% since the 1990s—the 1997–1998 Asian financial crisis, the 2000–2003 dot-com and SARS period, the 2007–2009 global financial crisis, the 2015–2016 China scare, and the 2021–2023 selloff—and recoveries have been slow. After the 2008 low, the index did not reclaim its prior peak in price terms until 2018. A household whose savings, home, and salary are all tied to the same economy feels each of these episodes across its whole balance sheet at once.

The remedy is not to avoid Hong Kong. It is to add assets whose returns are driven by different forces—different economies, currencies, asset classes, and sectors—so that a shock to any one of them does not move the whole portfolio.

The Hong Kong dollar has been pegged to the US dollar within a band of 7.75 to 7.85 since 1983, maintained by the Hong Kong Monetary Authority (HKMA) through the Linked Exchange Rate System. As of June 2026, the HKMA held approximately US$445.9 billion in foreign exchange reserves—a buffer that has historically been sufficient to defend the peg through repeated periods of stress.

Because the nominal HKD–USD rate barely moves, many Hong Kong investors treat currency risk as effectively solved. For an investor whose assets and spending are both in HKD or USD, exchange-rate volatility is indeed minimal. But three risks survive the peg:

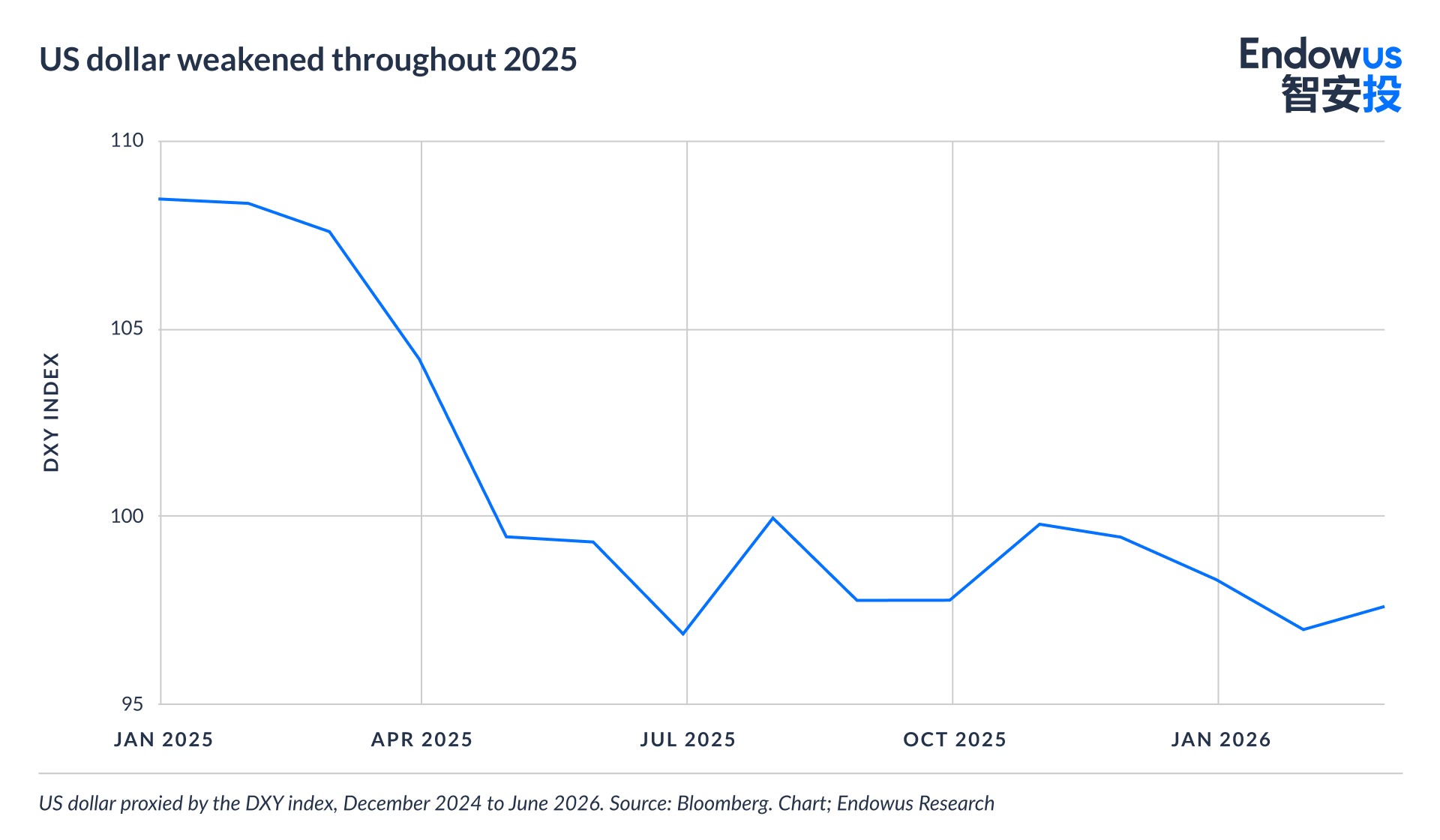

- Purchasing-power risk. When the US dollar weakens against other major currencies—as it did through 2025 as US fiscal deficits widened—the global purchasing power of HKD savings falls with it, even though the nominal peg holds.

- Imported monetary policy. The peg requires Hong Kong to track US interest rate decisions regardless of local conditions. When the US Federal Reserve tightens, Hong Kong absorbs that tightening to prevent capital outflows, which feeds through to the Hong Kong Interbank Offered Rate (HIBOR), banks’ HKD funding costs, and local mortgage rates—all of which increase as a consequence.

- Concentration risk. The peg offers no protection against over-exposure to Hong Kong equities and property, because those are HKD-denominated assets. A stable exchange rate does not help diversify a portfolio.

Holding assets denominated in euros, yen, sterling, and emerging market currencies may provide currency diversification that a stable HKD–USD rate cannot replicate.

A cost most Hong Kong investors overlook: fund domicile

There is a practical consideration that separates Hong Kong-based investors from their peers in many other markets: US dividend withholding tax.

Investors in Hong Kong who are not US tax residents are subject to a 30% withholding tax on cash dividends paid by US-domiciled securities and exchange-traded funds (ETFs). The drag is not trivial. On a 2% dividend yield, a 30% withholding reduces the effective yield to 1.4%, and that gap compounds over time.

Funds domiciled in jurisdictions such as Ireland and Luxembourg can access a reduced 15% withholding rate under their tax treaties with the US. For two otherwise similar funds tracking the same index, domicile alone can therefore change the net income an investor receives.

This is one area where an adviser who understands the Hong Kong tax context—and constructs portfolios around it—adds value beyond generic asset allocation.

How you can build genuine diversification as a Hong Kong-based investor

Global diversification for a Hong Kong-based investor works across four dimensions.

- Geographic breadth. Meaningful allocations to US, European, Japanese, and emerging market equities.

- Asset class breadth. Fixed income, alternatives, and cash-equivalent instruments alongside equities. This is where correlation does real work: since 1999, a portfolio of 60% global equities and 40% global fixed income has delivered an average annual return of approximately 7.06%, and fixed income was positive in seven of the eight calendar years in which equities fell. Past performance is not necessarily a guide to future performance or returns.

- Currency breadth. Assets across multiple currencies hedge HKD-specific risks, including any future adjustment to the peg.

- Fund-structure efficiency. Choosing fund domiciles that limit withholding-tax drag for non-US tax residents, and favouring funds that pass through institutional-class pricing.

For most Hong Kong investors, the starting point is to recognise the concentration already embedded in local property, equities, and USD-pegged cash—and then to add, deliberately, the assets that do not share those risks.

Investment implications

The single most useful step for a Hong Kong-based investor is to audit actual exposure—not just the equities consciously selected, but the full picture, including property, employee stock options, and cash. This is the only way to find out if effective exposure to mainland China and HKD-correlated assets is effectively higher than intended.

In our view, the objective is not to predict which market leads next, but to own enough exposure to the global economy that the question about which market is going to outperform stops mattering to the portfolio’s survival. The remedy is not to divest from Hong Kong stocks, but to build the global layer deliberately and gradually, as an addition to existing assets, using institutional-quality funds and structures appropriate for Hong Kong residents.

Endowus provides access to more than 300 funds curated from global managers, including funds selected for their suitability for Hong Kong-based investors. The Flagship portfolios are built around broad, low-cost, globally diversified exposure, with an asset allocation calibrated to each investor’s risk profile and time horizon.

Before adding global exposure, it is worth understanding the home-market position you are diversifying away from. Our guides to the Hang Seng Index’s historical returns and volatility and to building a diversified portfolio with ex-US funds set out the evidence in detail. For investors ready to build a portfolio that reflects where they actually live, the conversation starts at endowus.com/en-hk.

Frequently asked questions

Is the Hang Seng Index a good proxy for global equity exposure?

No. The HSI is heavily concentrated in companies whose core revenues are rooted in mainland China. It provides no meaningful exposure to US, European, or Japanese markets, and its risk profile is closely tied to mainland China’s macroeconomic and regulatory conditions.

Does the HKD peg remove currency risk for Hong Kong investors?

It removes HKD-to-USD conversion risk, but not exposure to US dollar weakness, imported US monetary policy, or concentration in HKD-denominated assets. A stable exchange rate is not the same as a diversified portfolio.

Why does fund domicile matter for Hong Kong investors?

Hong Kong-based investors who are not US tax residents face a 30% withholding tax on dividends from US-domiciled funds. Funds domiciled in certain jurisdictions, such as many Ireland-domiciled funds, access a reduced 15% rate under US tax treaties. Domicile selection is therefore a meaningful consideration when building global equity exposure.

What does a well-diversified portfolio look like for a Hong Kong investor?

It combines geographic breadth (US, Europe, Japan, and emerging markets), asset class breadth (equities and fixed income at minimum), currency breadth beyond the HKD–USD pair, and fund structures that are efficient for Hong Kong tax residents. The exact allocation depends on the investor’s risk tolerance and time horizon.

How does Endowus help Hong Kong investors access global diversification?

Endowus provides access to more than 300 institutional-quality funds from leading global managers, with a curated selection for Hong Kong residents. The platform offers diversified Flagship portfolios, individual fund access through FundSmart, and private markets for eligible professional investors—at institutional-class fee levels.

Risk Warnings

Investment involves risk. Past performance is not an indicator nor a guarantee of future performance. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

This article is not intended to be relied upon as a forecast or research or investment advice, and should not form the basis of any investment or other decisions. The information contained herein is not intended, and should not be construed, as any legal, tax, regulatory, accounting or financial advice. If you would like investment, accounting, tax or legal advice, you should consult with your own professional advisors regarding your individual circumstances and needs.

The information in this article may not be suitable for all investors. You are responsible for any action that you take or decision that you make in reliance on any content in this article, and you agree that Endowus HK Limited (“Endowus”) is not liable under any circumstances.

No invitation or solicitation

Neither the information, nor any opinion, contained in this article constitutes a recommendation, offer or solicitation by Endowus or its affiliates to you to buy or sell any securities, collective investment schemes or other financial instruments or services, nor shall any such security, collective investment scheme, or other financial instruments or services be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction.

This is not intended to be an invitation or offer made to the public to subscribe for any financial product or to enter into any transaction.

Accuracy of Information

Whilst Endowus has made reasonable efforts to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or errors in any such information. Endowus does not warrant or represent that the information in this article is correct, accurate or reliable.

Opinions

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this article are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

In presenting the information above, none of Endowus, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider whether any investment views and products/services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances.

This article has not been reviewed by the Securities and Futures Commission of Hong Kong. Endowus HK Limited is licensed by the Securities and Futures Commission of Hong Kong (CE No. BQR225) to carry on Type 1 (Dealing in Securities), Type 4 (Advising on Securities) and Type 9 (Asset Management) regulated activities.

.png)