.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

About the event

When it comes to investing for passive income, there seems to be an overwhelming range of options available. Anything from investments like bonds, dividend stocks and CPF LIFE to financial products like annuities, income funds and REITs are available for retail investors to consider.

While some financial products are marketed to give high, stable returns, they come with their own restrictions, hidden fees and other drawbacks. Meanwhile the industry doesn’t make it easy to optimise for individual needs like more stability, higher payouts or greater growth.

Find out how Endowus Income Portfolios have revolutionised the way you can better invest for passive income, effortlessly and inexpensively. We will cover:

- Common income solutions and their pros and cons

- Our new range of Endowus Income Portfolios

- How to decide which approach to income investing works best for you

- Our approach to portfolio construction for income investing

- How we manage our portfolios on an ongoing basis

Chapters

00:00 Introduction to Endowus

05:08 What is income investing?

07:04 What is the difference between income investing and growth investing?

12:15 How did we build our Income Portfolios?

15:17 How to decide between different Endowus Income Portfolios?

20:48 How are the Endowus Income Portfolios different from others?

25:50 Yield of different fixed income or equities sectors

30:04 How much more you save in fees with Endowus

33:24 Historical performance and risk of the Income Portfolios

35:53 Stable Income Portfolio deep-dive

41:02 Higher Income Portfolio deep-dive

45:01 Future Income Portfolio deep-dive

48:18 Risk of different Income Portfolio

52:50 Live audience Q&A

Learn more about the Endowus Income Portfolios here.

What is the difference between income investing and growth investing? (07:04)

Sam: The purpose of income investing is to prioritise current income. On a basis of $100,000 invested with a 5% payout ratio, you would receive about $420 per month. This money would then be taken out of your investment for you to spend. You can also have a capital growth component for your portfolio but the purpose is to grow capital so that you can take some out while preserving capital.

Whereas growth investing is about maximising the long term wealth and your savings. The focus is to grow your capital as opposed to current income. Some people may have current income or distributions from their current investments but the money is mostly reinvested. If a $100 payout is received, it will be reinvested and continue to compound the growth of your wealth.

From this illustration comparing income investing and growth investing, for income investing you will have $105,000 at the end of 5 years, which is more than your initial investment despite receiving payouts for spending. However, for growth investing, since you have reinvested your payouts, the compounding returns you receive will be more than the sum of all the payouts that you would have received.

Differences between the 3 Income Portfolio (19:28)

Sam: The 3 Income Portfolios have very distinct differences, ranging from the primary objective to your secondary objective on whether you are trying to achieve capital preservation or grow your capital. The current payouts and estimated long-term appreciation are different as well. All of these products can reach negative returns in the short term. However, income products should not be focused on the capital in the short term but instead the long term returns over decades to achieve consistent payouts and long term capital appreciation that is expected from the portfolio.

Note: Long-term estimated capital appreciation and total returns are based on a calculation of 95% probability range of outcomes on the lower end based on historical capital appreciation data and monte carlo simulation of outcomes for the upper end over 10 years. Actual performance may be greater or less than estimates depending on market movements and fund manager decisions that may be beyond the control of Endowus. Past performance is not a guarantee of future returns.

What makes the Endowus Income Portfolios different from others? (21:52)

Yulin: Endowus uses a robust and institutional framework based investment process and a multi-manager model. We are in a unique position of doing this because we are not tied to a single manager and we are only paid by you making us independent. We also have the expertise to do it well because of the due diligence process.

We assess the capability of the investment manager. After thorough research, we choose fund managers with the conviction, capacity, the right team and process to deliver consistent investment performance as well as income, since this is the primary objective of the strategies that they manage.

We assess the consistency and sustainability of the income payouts. This requires us to understand the distribution structure of the fund — its sources of income for the payout, especially knowing if they are dipping into the capital which is something we do not want to see. We also need to know if the current yield of the fund is able to sustain the desired target payout of the fund.

Lastly, as emphasised, we also look at the cost of the product. We actively work and negotiate with fund managers to bring you access to the lowest cost share class possible. We do our best to provide you with institutional share classes of the funds and rebate all the trailer fees that are usually kept by distributors for themselves.

What is the yield of the different fixed income and equities sector? (25:50)

Sustainability of income is extremely important and it is not easy to get income returns. If you see a product that offers you 8% annual payout, you probably need to reconsider and look into the product to see how they are paying that 8%. Looking at the yield across different fixed income and equity sectors, in the market currently, the highest yielding is in Asian high yield because of the recent property saga that has depressed the price and artificially improved yield. Even so, it is only paying about 5.8%. If we look at government bonds, it is paying about less than 2%.

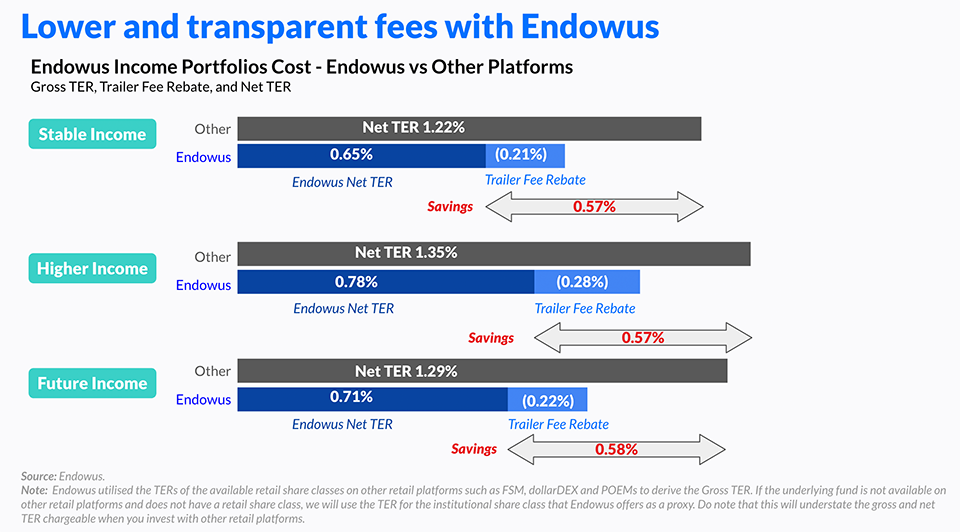

How much more you save in fees with Endowus (30:04)

Sam: Retail platforms, banks or fund platforms normally provide retail share class funds with a significantly higher net total expense ratio (TER). Endowus Income Portfolios have a net TER that starts at a lower portion because for some of these funds, we access institutional share classes that are not normally offered at banks, retail or fund platforms.

When we are unable to access institutional share classes, we will give trailer fee rebates back to our clients. This combination of savings for the portfolio that we provide is a significant amount. At 57 percentage points, that is almost half your investment. The savings are relatively significant and that is the reason why you should be using the Endowus platform.

Webinar: Choosing the right robo advisor in Singapore - Comparing Endowus with the rest

Webinar: Endowus Q2 2021: Performance review and market insights

Webinar: Endowus Q3 2021 Performance review and market insights

%20F1(2).webp)

.webp)

.webp)