.webp)

.webp)

.webp)

.webp)

%20(1)%20(1)%20(1).png)

Congratulations on your newly initiated Permanent Residency (PR) status! Apart from the benefits of being able to come in and out of Singapore with ease and taking advantage of the hawker culture, you are now entitled to participate in one of the best managed social security schemes in Asia, the Central Provident Fund (CPF). While your take home pay may be lowered due to your contributions into CPF, you might still be better off financially.

Read to find out more about CPF basics, your contribution rates, and what will happen to your CPF account if you renounce your PR status.

What is CPF?

The Central Provident Fund is Singapore’s pension scheme, a comprehensive social security plan that aims to help its members (both citizens and permanent residents) meet their retirement housing and healthcare needs. You are only able to withdraw these savings at the age of 55 and above.

Under the CPF scheme, all Singaporeans and Permanent Residents are required to make regular contributions to the fund. Each member will have their own CPF account in which these contributions are deposited. Similar to a regular savings account, these contributions earn risk-free interest on your behalf. Over time, this accumulation of wealth allows CPF to fulfil its intended mission of helping its citizens and residents meet their retirement and financial needs. Besides retirement, CPF can be used for education, healthcare and housing purposes.

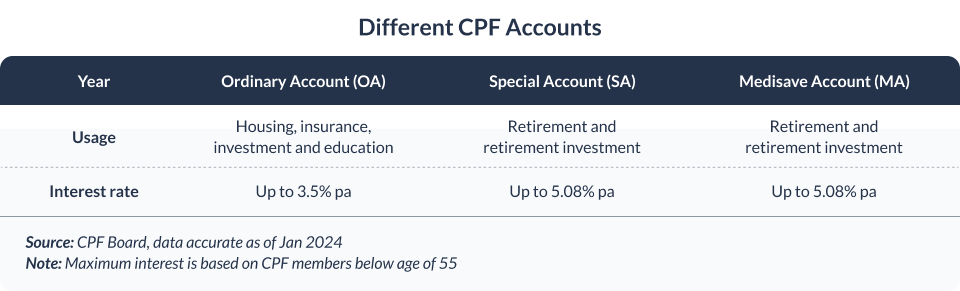

Your CPF is broken into three accounts - Ordinary Account (OA), Special Account (SA), and Medisave Account (MA) before the age of 55, immediately after which a fourth Retirement account (RA) is automatically created. A summary of the different CPF accounts are shown in the table below.

How do CPF contributions work?

Only employees that earn a monthly salary above $500 are required to make monthly contributions to their accounts and the rates of contributions vary depending on age group -- steadily reducing after the age of 55.

Under the plan, both employees and employers are mandated to make separate contributions to the employee’s CPF account. The employer’s contributions have to match that of the employee, and is similarly dependent on the employee’s age group.

How much do new Permanent Residents contribute to CPF?

As a new permanent resident, your contribution to CPF begins at the date of your status approval. Understandably, this sizable deduction from your take home wage might be hard to accomodate at the start, and therefore, the CPF board provides a two year adjustment scheme whereupon newly initiated permanent residents pay a lower contribution rate. This two year buffer is also applied to the employer’s contribution rate. By the third year of your permanent resident status, both you and your employer will have to start contributing the full amount.

How do I determine the start and end date of my lower contribution rate for CPF?

The first year of your Permanent Resident status begins at the date of approval of your entry permit (Form 5 or Form 5A) and it ends on the last day of the month of the first anniversary of your SPR conversion.

The second year of your Permanent Resident status begins on the first day of the month after the month of the first anniversary of your conversion. It ends on the last day of the month of the second anniversary of your conversion.

Consider this example:

CPF contribution rates vary your first two years as a newly initiated Permanent Resident

Under this adjustment scheme for newly initiated Permanent Residents, both employers and employees contribute to CPF at a reduced rate, known as graduated employee - graduated employer rate.

Note: View the full breakdown of contribution rates for all age groups for new PRs here.

If your employer wishes to contribute at a higher CPF rate for you, known as graduated employee - full employer rate, both parties will have to apply for a joint application.

Note: View the full breakdown of contribution rates for all age groups for new PRs here.

If you wish to contribute at a higher CPF rate, known as full employee - graduated employer rate, you can voluntarily top up your CPF through Retirement Sum Top-Up Scheme (RSTU).

If both you and your employer wish to contribute at a higher CPF rate, known as full employee - full employer rate, you will have to engage in both - applying for a joint application for the full employer contribution, and topping up your CPF through the RSTU for the full employee contribution.

As mentioned above, once you have fully transitioned by your third year, you will no longer be considered a newly initiated Permanent Resident and will be subject to pay the full contribution rate, which is the same for all PRs and Singapore Citizens.

What happens to your CPF if you plan to leave Singapore

Keeping your PR status

Intending to migrate overseas temporarily for a new job or for family matters but keep your PR status? Great news! Your CPF account will still be active and your existing funds will still earn risk free interest. However, it is important to note that you and your overseas employer are not required to make any contributions to CPF while living abroad.

While you may not be able to use your CPF funds in your OA, SA and MA accounts to buy a house or for medical expenses while abroad, you are still entitled to use it for other family members residing in Singapore.

Renouncing your PR status

If you plan to leave Singapore and West Malaysia permanently and renounce your PR status, you can apply to CPF Board to withdraw all of your savings. To do so, you can make your application through post or in person.

Once your application has been approved, you will receive all of your funds by interbank GIRO transfer to your Singapore bank account or your overseas bank account. Do note that any outstanding tax liabilities will first be deducted from your CPF savings before any withdrawals.

If you have made an investment under the CPF Investment Scheme (CPFIS), your CPFIS Account will be closed and your investments will be transferred to your own Central Depository (CDP) account and liquidated.

You can choose to terminate your CPF LIFE plan and collect the remaining unused premiums, or choose to remain in the CPF LIFE Scheme and continue to receive monthly payouts to your Singapore bank account.

Missing Singapore? If you decide to return and reobtain your PR status, you will need to refund CPF the full amount withdrawn and accrued interest.

<divider><divider>

This article is for information purposes only and should not be considered as an offer, solicitation or advice for the purchase or sale of any investment products. It is recommended that you seek financial advice as to the suitability of any investment. Whilst Endow.us Pte. Ltd. (“Endowus”) has tried to provide accurate and timely information, there may be inadvertent delays, omissions, technical or factual inaccuracies or typographical errors.

Any opinion or estimate above is made on a general basis and none of Endowus, nor any of its affiliates, representatives or agents have given any consideration to nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Opinions expressed herein are subject to change without notice.

Investment involves risk. The value of investments and the income from them can go down as well as up, and you may not

get the full amount you invested. Past performance is not an indicator nor a guarantee of future performance.

Please note that the above information does not purport to be all-inclusive or to contain all the information that you may need in order to make an informed decision. The information contained herein is not intended, and should not be construed, as legal, tax, regulatory, accounting or financial advice.

%20(1).gif)