.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

.jpg)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- In the current elevated interest rate environment, SMEs and startups cannot keep ignoring the opportunity cost of leaving corporate cash in a non-interest-bearing current account.

- Liquidity remains the primary constraint for most businesses. Money market funds (MMFs) and ultra-short duration bond funds may offer a practical middle ground: competitive yields without lock-up periods, alongside limited credit risk.

- Endowus helps corporate clients navigate the key tradeoffs in cash management — liquidity, FX risk, diversification, and asset safety — while offering access to institutional share class funds and 100% Cashback on trailer commissions, potentially reducing fund fees by up to 50%.

To learn more about the Endowus Treasury and Institutional Advisory Services, please visit this link or contact us at institutional@endowus.com.

Interest rates remain at multi-decade highs, while central banks grapple with sticky inflation amidst elevated energy prices. For small and medium-sized enterprise (SME) owners, chief financial officers (CFOs), and startup treasurers, the opportunity cost of inaction has never been greater. Yet for many businesses, the path to higher yield on corporate cash remains either unclear or operationally cumbersome.

This piece lays out why that gap exists, and how to close it.

Why corporate cash so often sits idle

The instinct to leave working capital in a current account is understandable. Liquidity is not optional for a growing business — cash flow mismatches can be existential. But the reasons companies forego returns may at times go beyond caution.

Forecasting uncertainty creates over-buffering. Most yield-generating instruments with attractive rates — fixed deposits, in particular — carry lock-up periods or early termination penalties. Because cash flow forecasts are imperfect, treasurers tend to hold larger buffers than necessary. The result is a potentially significant pool of capital earning nothing, with potential for inflation-driven erosion.

Traditional banks underserve the SME segment, as these firms generate limited fees compared to large corporates or multinationals. In practice, this means fewer product offerings, less proactive advice, and limited access to the institutional-grade instruments available to larger clients.

In addition, comparison shopping can be time-consuming for the leadership of a small firm. Evaluating fixed deposit rates across multiple banks requires setting up accounts, managing separate logins, and splitting relationships — none of which improves a company’s standing with any single institution. Finance teams at (typically) lean SMEs rarely have the bandwidth to run that process.

Beyond fixed deposits, a range of yield-enhancement products exists — some straightforward, some not. Enhanced money market certificates, for example, are structured products that embed a fixed deposit within a structured note. The headline yield is higher, but so is the potential risk. These distinctions are easy to miss without specialist knowledge.

It is also worth noting that fixed deposits are not risk-free. The March 2023 collapse of Silicon Valley Bank and UBS’s rescue of Credit Suisse are sobering reminders that beyond the deposit insurance limit, deposits rank no higher than unsecured creditors. In Singapore, the Singapore Deposit Insurance Corporation (SDIC) insures up to a maximum of S$100,000 of deposits held with member banks and finance companies — a limit that may be insufficient for businesses with larger cash balances.

A better approach: money market funds for corporate cash

One instrument that deserves more attention from corporate treasurers is money market funds (MMFs).

An MMF is a type of mutual fund that invests across a diversified portfolio of short-term, high-quality instruments - typically government Treasury bills (T-bills), commercial paper, and certificates of deposit. The combination of diversification, high credit quality, and short duration means MMFs are designed to preserve capital while generating a return broadly in line with prevailing short-term interest rates.

Critically, MMFs offer daily liquidity - unlike fixed deposits, there is no lock-up period and no early redemption penalty. Proceeds from a sale are typically returned within three to four business days - a meaningful advantage for businesses that need to maintain operational flexibility.

The scale of institutional adoption speaks for itself. According to Bloomberg, as of early 2026, investors have added more than US$162 billion to U.S. money market funds (MMFs), driving total industry assets to a record high of over US$8.27 trillion.

What this looks like in practice

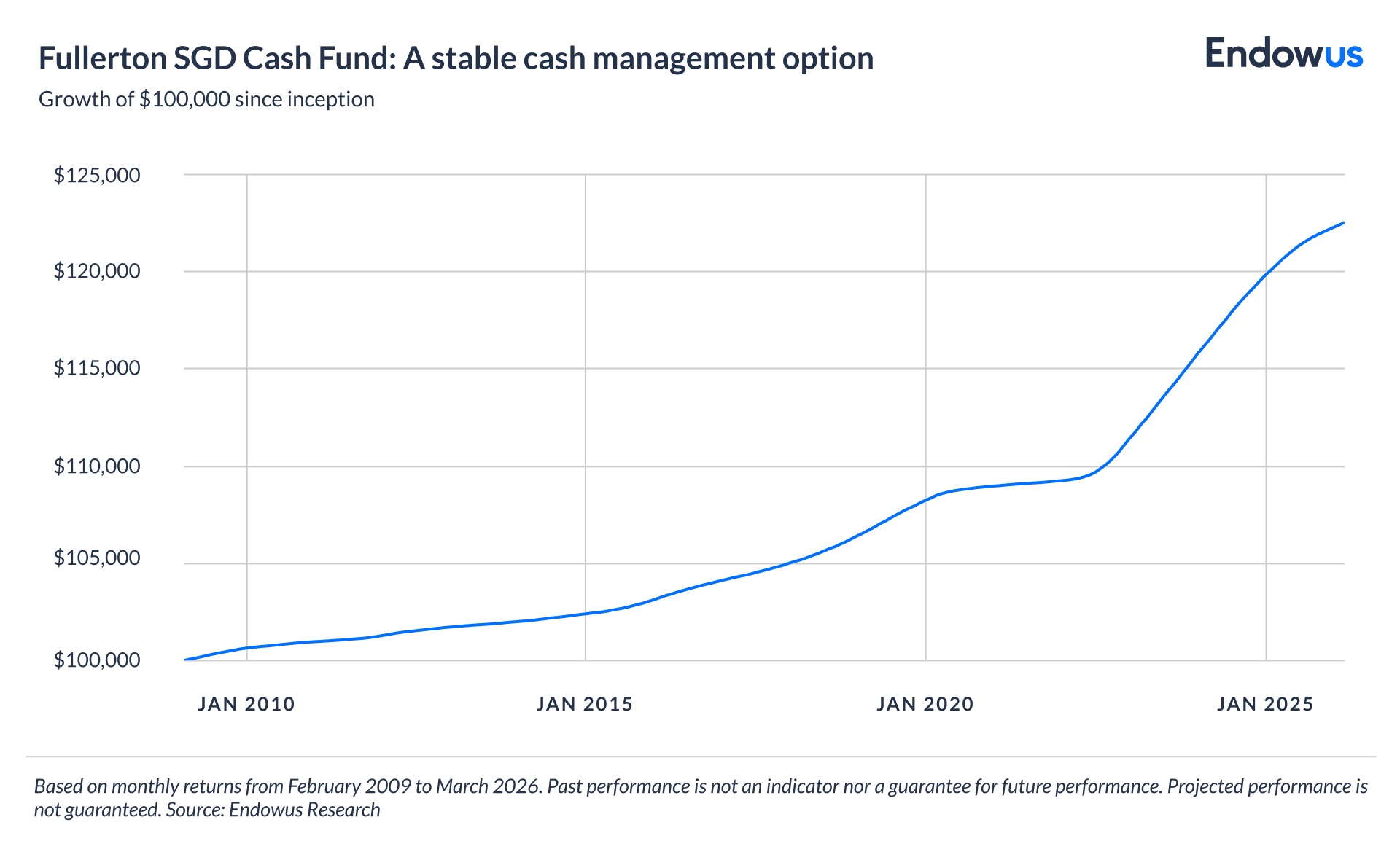

The Fullerton SGD Cash Fund, for example, has been in operation since February 2009. Its track record spans the global financial crisis (GFC), the Covid-19 drawdown, and the subsequent rate hike cycle. Since inception, its maximum drawdown has stood at just -0.03% — a loss recovered by the following day. On a monthly basis, the fund has delivered consistently positive returns throughout this period.

Endowus offers MMFs in SGD, USD and EUR—explore them on the Endowus Fund Smart funds list.

How Endowus addresses the gap for SMEs and startups

Endowus Treasury Solutions brings together the instruments, access, and expertise that most SMEs cannot easily assemble on their own — on a single, regulated platform.

Institutional fund access and fee efficiency

Endowus provides access to institutional share class funds — the same vehicles typically reserved for large institutional investors — alongside an industry-first 100% Cashback on trailer commissions. Combined, these features may reduce fund fees by up to 50%, directly improving net returns on deployed corporate cash.

A curated investment universe

Beyond money market funds, Endowus offers access to more than 400 best-in-class funds spanning fixed income, equity, and multi-asset strategies across more than 50 leading global fund managers. Every fund on the platform has been assessed through the Endowus SMART+ proprietary framework — evaluating the investment firm, team, investment process, performance track record, fee structure, and business practices. This is not a fund supermarket. It is a filtered, adviser-constructed range.

Institutional advisory services

The Endowus Investment Office constructs customised portfolios and provides clients with a clear view of what they own and why. For corporate mandates, this typically includes analysis of historical returns and maximum drawdown, yield to maturity (YTM) relative to credit rating, YTM relative to portfolio duration, and fund liquidity profiles.

Dedicated relationship management

Each corporate client is assigned a dedicated advisor. Our advisory team brings experience from institutions including Morgan Stanley, UBS, Nomura, Saxo, DBS, and Citibank.

Multi-currency solutions

Endowus offers investment solutions in SGD, USD, AUD, CHF, EUR and GBP, with access to competitive FX rates passed through from wholesale brokers without added spread.

Asset safety and regulatory standing

Endowus Singapore is licensed and regulated by the Monetary Authority of Singapore (MAS). By law, client monies and assets are fully segregated from Endowus's own balance sheet, with a complete ledger of all holdings maintained at all times.

Endowus does not offer leverage and does not lend out client assets. All invested assets are held by fund-appointed custodians — a structural safeguard built into the platform from inception.

To find out more about corporate cash management, please visit this link or contact us at institutional@endowus.com.

Frequently asked questions about corporate cash management

Why is cash management important for SMEs and startups?

Idle corporate cash carries a real opportunity cost, particularly in an elevated interest rate environment. Cash held in a non-interest-bearing current account earns nothing while inflation erodes its value. For SMEs and startups, where every dollar of working capital matters, even a modest yield on excess balances can fund operating expenses, extend runway, or contribute meaningfully to the bottom line.

The challenge is that traditional banks tend to underserve smaller businesses, offering fewer product options and less proactive advice than they extend to large corporations, leaving SME treasurers to figure out yield-enhancement on their own.

Is it safe to invest corporate cash in money market funds?

Money market funds are designed to preserve capital, but they are not guaranteed and do carry some risk. They invest in short-term, high-credit-quality instruments and diversify across issuers and tenors, which significantly limits exposure to any single counterparty.

To find the most suitable solution, choose from three Endowus Cash Smart portfolios designed to cater to your business’ risk tolerance and unique cash management needs, based on factors like the expected investment time horizon, or when you might require cash for the next expense.

How should businesses manage cash in different currencies?

We generally advise our clients to match the cash to the currency of the liability. Additionally, FX conversion fees should be kept as low as possible. Endowus offers investment solutions in SGD, USD, AUD, CHF, EUR and GBP, with FX rates passed through from wholesale brokers without added spread.

How does onboarding of corporate cash management on Endowus work?

Corporate onboarding involves company verification (ACRA records for Singapore entities, equivalent for other jurisdictions), beneficial owner identification, and authorised signatory setup. Once live, the workflow is similar to managing a corporate bank account: subscribe to or redeem funds via the platform, with settlement typically T+3 for money market funds.

Each accredited* investor corporate client is assigned a dedicated relationship manager from Endowus's advisory team that brings experience from institutions including Morgan Stanley, UBS, Nomura, Saxo, DBS, and Citibank—for portfolio construction, drawdown analysis, and yield-to-maturity reviews relative to credit rating and duration.

*Accredited investor corporate clients refer to firms with net assets that exceed S$10,000,000 in value as determined by your most recent audited balance-sheet/ balance sheet, otherwise, your corporation’s entire share capital is owned by one or more persons, all of whom are accredited investors as defined in section 4A of the Securities and Futures Act.

Webinar: Choosing the right robo advisor in Singapore - Comparing Endowus with the rest

Webinar: Endowus Q2 2021: Performance review and market insights

Webinar: Endowus Q3 2021 Performance review and market insights

%20F1(2).webp)

.webp)

.webp)