.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- The recent volatility driven by a sudden spike in oil prices and the prospect of further escalation in the Middle East, is making investors across the globe nervous.

- Investors should be aware of behavioural biases, such as overconfidence and recency bias, that can impact decision-making.

- Building a resilient portfolio involves diversification across asset classes to mitigate risks and align with an investor's goals and risk tolerance.

- Conflict-free advice and guidance can support investors in making evidence-based investment decisions.

- Click here to get started on your wealth and retirement savings journey with Endowus today.

This article has been reproduced from SCMP, originally published on 14 August 2024. Certain updates have been made for accuracy and relevance. The core substance of the original reporting has been preserved.

The recent volatility driven by a sudden spike in oil prices and the prospect of further escalation in the Middle East, is making investors across the globe nervous. Singapore’s benchmark index, the Straits Times Index (STI), was down close to 2% as of 25th of March, 2026 from its 26th of February, 2026 high of 5000.

In a context where war—alongside private credit-related negative headlines—is keeping investors on their toes, what lessons can we draw from their reactions to past crises, and most importantly, how do we make sense of their decisions?

Learn financial science and behavioural science

Q: What role does science play in individuals’ investing success?

Gregory Van: Investors must understand that making decisions driven by short-term emotions often leads to poor outcomes. Controlling behavioural biases plays an enormous role in long-term success as an investor. But in order to do so, you need to better understand how the markets work.

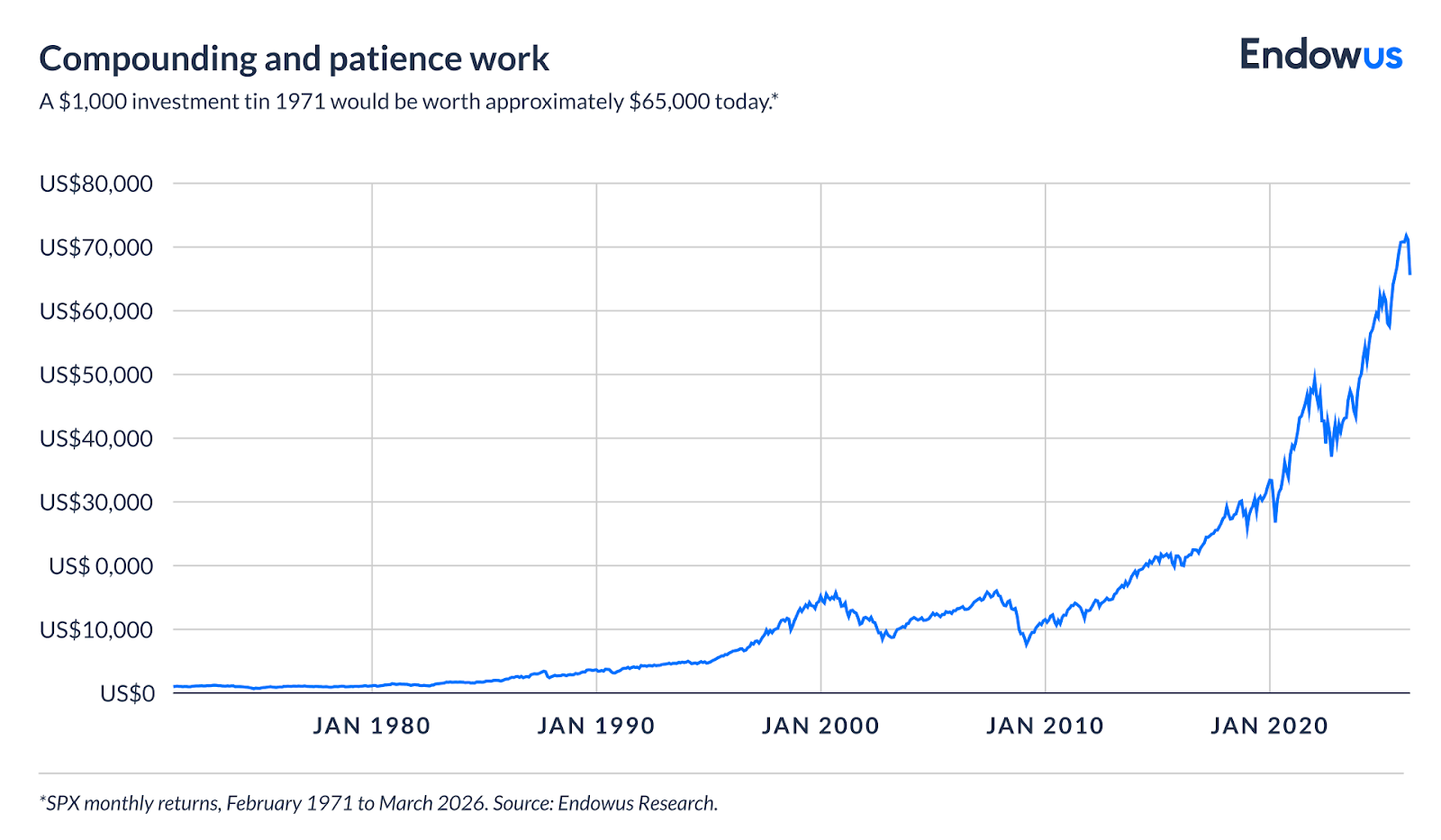

First, you need to first understand the financial science—the evidence for why a basket of assets will appreciate over time and why it’s suitable for the purpose of your investment. In fact, if you invested $1,000 in the S&P 500 in 1971 and stayed invested through the various downturns, you would have approximately $65,000 today.

Q: What about individuals' behaviours? What’s the science or evidence behind them?

Gregory Van: There’s the behavioural science aspect in every one of us. At least 70% of people think that they are above-average drivers, despite the statistical impossibility.

This phenomenon is known as illusory superiority—a cognitive bias defined in social psychology wherein people overestimate their own qualities and abilities compared to others. In investing, we tend to believe that we are all better-than-average investors.

One of the investor blind spots and behavioural biases that we all are hard-wired to believe is being overconfident, making us tend to hold onto losers and sell winners.

Another example is that we place excessive weight on recent events. It is easy to extrapolate positive market moves like the AI-driven tech rally, expecting it to continue forever—that’s your recency bias speaking. Obviously, sensational headlines—“jitters,” “meltdown,” and “$1 trillion wipeout”—do not help calm the feeling of unease and make it seem like the stock market is behaving abnormally.

In fact, the markets are really just fluctuating the way it always does, dealing with crisis after crisis, and the million reasons to get out now or jump in immediately.

Building a resilient portfolio

Q: Given the psychological pitfalls commonly ingrained in our minds, what should we do with our money?

Gregory Van: When things start to go sour, the market unwinds on itself extremely quickly, faster than anyone can really control.

A diversified portfolio, with allocations across different asset classes and securities, helps mitigate risks and capture overall market returns that are aligned with an investor's goals and risk tolerance.

Diversification across asset classes has been an effective strategy to manage risk over time. Holding concentrated positions in individual assets exposes investors to unnecessary risks.

Guided by goals, supported by conflict-free advice.

Q: Knowing all the scientific knowledge, how do we know if our approach is based on evidence?

Gregory Van: Simply owning a stock, a cryptocurrency, a single bond, or a small basket of bonds is not an evidence-based approach. Investors who choose that approach are just at the whims of the market, of that company, or of that CEO.

When you are speculating and gambling, being too concentrated on one investment is OK, knowing the risk. To note, the markets have given multiple harsh reminders of how the value of any single stock or assets can wildly fluctuate.

Once people understand what they are investing for and towards—financial or life goals—and are properly positioned within the market, then the market can yield incredible returns.

In the face of recent market events, sticking to what your goals are is the key to avoiding being “thrown into emotional circles”. Investors must understand their investment horizons and their goals.

Q: Lastly, what’s my next step and how should I build my portfolio around these?

Gregory Van: Investors in Singapore and broader across Asia are starting to realise what it means to get conflict-free wealth services and to access real advice, real suggestions in terms of strategies and portfolios that suit people’s goals.

It is encouraging to see that retail investors in the region are increasingly grasping the importance of improving their financial literacy and of choosing appropriate wealth-management services.

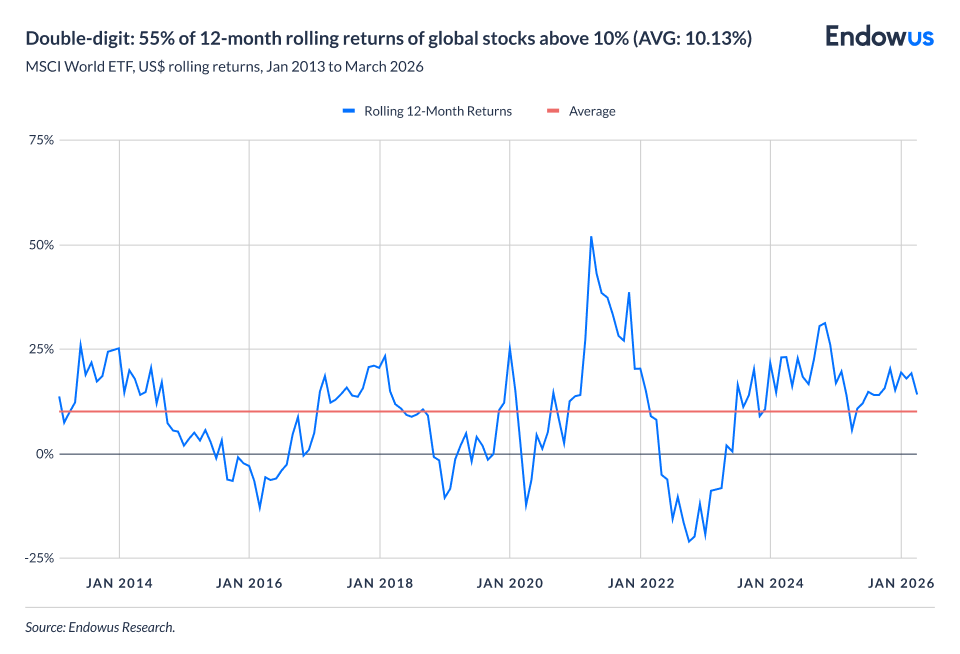

As I alluded to previously, financial markets have always skewed positively, which means that over time they move to the right, on an upward trajectory, and are expected to hit a new high over time.

Before reaching there, one has to know that the path is far from smooth. The rolling returns of 12-month periods can vary significantly, ranging from both significantly positive and extremely negative outcomes. This variability extends to even shorter periods as well.

This is why we suggest having a regular savings and investment plan and sticking to that plan, despite what markets do in the short term. These systems and plans such as dollar-cost averaging, are put in place to remove emotions from the decision-making process.

Forget your password? It's a good thing for your investments

The lesson of Hyflux: What water and diversification have in common

Free lunch: Diversification in investing is a gift

.jpeg)

%20F1(2).webp)

.webp)

.webp)