.webp)

.webp)

.webp)

.webp)

Singaporeans are embracing the move to top up their CPF and SRS funds.

In October 2024, it was reported that CPF top-ups in the eight months of the year had already hit over S$3 billion, which was up 15% from the same period in 2023. We are also seeing more SRS account holders today, and the tally of SRS contributions rose to over S$18 billion by end-2023.

Given the rising popularity of such top-ups to retirement schemes in Singapore, here is a useful guide to the latest updates.

CPF top-up methods for income tax relief

There are many ways you can top up your CPF contribution, though not all can be tax deductible to reduce your taxable income. The tax relief methods recommended below are also constrained by the maximum personal tax relief of S$80,000.

1. Contribute to the CPF accounts of your loved ones

You can give your parents and spouse a mini CPF monetary gift by topping up their CPF account. If your parents are over 55 years old, and their CPF RA savings haven't exceeded the current Full Retirement Sum (FRS), you will be able to make cash top-ups to their accounts and enjoy tax savings.

If they are younger than 55 years old, their CPF SA must be at the current FRS after subtracting the sum of SA savings and net SA savings withdrawn for investments. That gives you the maximum amount of top-ups they can receive, and for which you get tax relief benefits.

To be eligible for tax relief for any CPF SA/RA cash top-up for your spouse, your spouse’s income in the previous year should not exceed S$4,000. From YA 2025, this cap will increase to S$8,000.

The maximum tax relief you can get from cash top-ups is now capped at S$8,000. If you top up both your own and a loved one’s CPF, you can get a total tax relief of up to S$16,000. This can significantly reduce your tax burden, especially if you're in higher income tax brackets.

It is also a perk for your loved ones, as CPF accounts earn competitive interest rates, with a combined annual interest rate of up to 6% for funds in their OA, SA and RA.

Not only will they get to enjoy a higher interest rate compared to a bank savings or fixed deposit account, it'll also help to increase their lifelong monthly payout through CPF Life.

Note: Cash top-ups to a recipient eligible for the MRSS (Matched Retirement Savings Scheme) are only eligible for tax relief on amounts beyond S$2,000, which is the MRSS grant cap.

2. Contribute to your MA and SA

You can prioritise topping up your CPF MA over your CPF SA since you can use your CPF MA for various medical purposes and to pay the premiums of your hospitalisation policies, including MediShield Life/Integrated Shield Plans.

You can also use it to pay for approved day surgeries such as wisdom tooth extractions, or approved chronic conditions such as asthma and psoriasis.

The annual tax relief available for contributions to your own MA and SA is capped at S$8,000. This incentive can help individuals effectively manage their healthcare costs while contributing to their long-term financial planning.

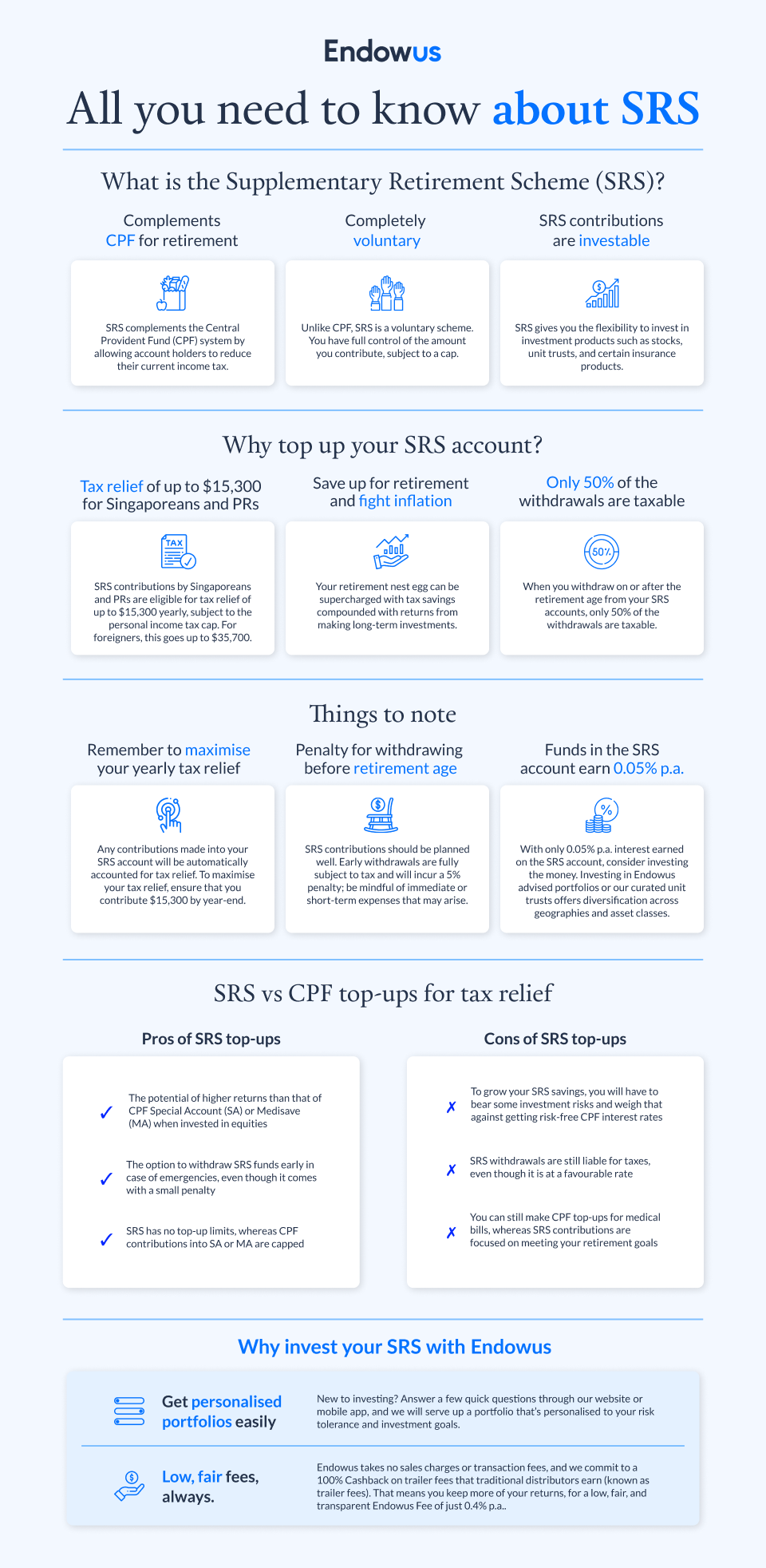

The SRS top-up method for income tax relief

In 2024, the maximum SRS contribution is S$15,300 for Singapore citizens and permanent residents and S$35,700 for foreigners. The entire top-up amount qualifies for tax relief.

Investing your SRS funds is crucial to beating inflation and growing your retirement savings. The SRS offers flexibility for investors, as you can invest your SRS funds in a wide range of assets like stocks, bonds, and unit trusts.

Consider a diversified portfolio that includes equities for higher returns, alongside more stable assets like bonds for risk management. Ultimately, the right allocation will depend on your risk tolerance and time horizon. For instance, younger investors might favour equities, while those nearing retirement may prefer conservative options to preserve capital.

Withdrawals from SRS are only taxed at 50% of the withdrawal amount when you have reached the statutory retirement age (determined by the year you put your first dollar in).

Bonus: Find out how you can make SRS withdrawals at retirement age, tax-free – How to get tax relief in Singapore through SRS.

Topping up your Supplementary Retirement Scheme (SRS) account to lower taxable income

If you have been investing consistently and are comfortable with the volatility of the stock market, you can look at topping up your SRS account as well. You can also take greater risk with investing through SRS.

In the scenario where you really need the cash from SRS, you also have the option to withdraw it with a 5% penalty, and the amount withdrawn will be taxable.

How should you decide between CPF or SRS top-ups?

When deciding between topping up your CPF or SRS account, it’s essential to consider factors such as your age, financial goals, and retirement needs. Both CPF and SRS top-ups offer tax relief, but they differ in terms of accessibility, returns, and flexibility. Here’s a detailed comparison to help you make an informed decision.

Which account to top up is highly subjective and is ultimately a very personal decision. Your age also affects the decision as well — if you are older, topping up SRS or even your CPF SA makes more sense because you have a shorter lock-in period.

Before topping up both accounts to maximise tax reliefs, note again that there is a maximum personal tax relief of S$80,000. If you have a high CPF contribution from work (that is, tax relief up to S$37,740) and other tax reliefs such as Working Mother’s Child Relief (WMCR), you will not get extra tax relief from these top-ups.

For those who are younger, you may prefer to top up the SRS account first because of the potential higher returns from SRS. A consistent, dollar cost average (DCA) approach for SRS investment (at no additional transactional cost through Endowus) will give you a better chance of hitting a 6% to 7% returns from investing in a 100% equity portfolio. You can check out the historical returns of the funds that we carry, and try playing around with the portfolio allocation. Investors who choose to do this would aim to grow their retirement savings faster than any CPF top-ups.

To be clear, there is value in having cash on hand versus having it locked up in CPF or SRS. As a rule of thumb, we would not recommend you to try to save on taxes if your obligations are below the 7% tax bracket, but again, if you are older, this consideration may change because the lock up period is shorter. Do note that since SRS is a tax deferral account, the more money you have in it, the more you may have to pay in taxes when you withdraw.

Case studies: How to slash your taxes with CPF and SRS top-ups

To better understand how CPF and SRS top-ups can help reduce your income tax, let’s look at two real-life examples. These case studies illustrate how individuals at different life stages can strategically use CPF and SRS to maximise their tax savings while preparing for retirement.

Example 1: A 35-year-old saving S$3,000 on taxes with CPF top-ups

At 35, with an annual income of S$100,000, this individual tops up S$7,000 to their CPF Special Account (SA), qualifying for tax relief. By lowering their taxable income to S$93,000, they save S$805 in taxes at an 11.5% tax rate. On top of this, the CPF SA earns 4–5% interest, growing their retirement funds.

Example 2: A 55-year-old leveraging both CPF and SRS for maximum relief

This 55-year-old, earning S$120,000 annually, tops up S$7,000 to their CPF Retirement Account (RA) and contributes S$12,750 to their SRS account. With a total tax relief of S$19,750, the new taxable income is reduced to S$100,250, saving S$1,382 in taxes at a 7% tax rate. This approach secures both guaranteed returns from CPF and potential investment growth through SRS.

By utilising CPF and SRS top-ups, both the 35-year-old and 55-year-old significantly reduce their taxable income while preparing for retirement. The key is to align your top-up strategy with your financial goals and life stage to achieve the maximum tax relief.

To get started with Endowus, click here.

Next on the Endowus Fin.Lit Academy

Read the next article in the curriculum: How you can help your parents better manage their CPF

.png)

%20F1(2).webp)

%20(1).gif)

.webp)

.webp)