.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- The CPF Ordinary Account (OA) earns 2.5% per annum (p.a.) in 2026, while the Special, MediSave, and Retirement Accounts (SMRA) earn 4% p.a. from 1 July to 30 September 2026.

- Members below 55 earn an extra 1% on the first $60,000 of combined CPF balances. Members 55 and above earn an extra 2% on the first $30,000 and an extra 1% on the next $30,000.

- The 4% floor on SMRA rates has been extended to 31 December 2026, giving Singaporeans certainty on their retirement savings returns.

- Effective CPF interest rates can reach up to 6% p.a. for those 55 and above, making CPF a core building block for retirement planning.

- Invest your CPF OA with Endowus—Singapore's first and leading digital advisor for CPF investing—to grow returns above the OA floor.

The CPF interest rate is the cornerstone of long-term savings for working Singaporeans. As of Q3 2026, the Ordinary Account earns 2.5% per annum (p.a.), while the Special, MediSave, and Retirement Accounts continue to earn 4% p.a.. Bonus interest tiers can push effective returns up to 6% p.a. for members aged 55 and above.

Understanding how each CPF account interest rate is calculated, how the bonus tiers work, and how to make voluntary top-ups can meaningfully grow your retirement nest egg over time.

What is the CPF interest rate in 2026?

Your CPF accounts earn different interest rates, providing the foundation for your retirement savings.

From 1 July 2026 to 30 September 2026, the Ordinary Account (OA) earns 2.5% p.a., and the Special Account (SA), MediSave Account (MA), and Retirement Account (RA) earn 4.0% p.a., with the rates reviewed quarterly.

The SA, MA, and RA (SMRA) rate is pegged to the 12-month average yield of 10-year Singapore Government Securities (10YSGS) plus 1%, subject to a floor of 4% p.a.

Bonus interest stacks on top of the base rates. Members below 55 earn an extra 1% on the first $60,000 of combined CPF balances. Members 55 and above earn an extra 2% on the first $30,000, and an extra 1% on the next $30,000. This bonus interest is credited to the SA or RA to grow retirement savings.

What is the latest CPF OA interest rate in 2026?

From 1 July 2026 to 30 September 2026 (Q3 2026), the CPF OA interest rate is 2.5% p.a., which is the legislated minimum.

The OA interest rate is calculated as a three-month average of major local banks' interest rates, using a formula of 80% fixed deposit rates and 20% savings rates. It is reviewed quarterly and subject to the floor of 2.5% p.a..

Yields on Singapore T-bills and fixed deposit rates have trended lower over the past year. Even so, OA savings continued to enjoy the floor rate, even as the prevailing computed rate remains well below the 2.5% floor.

The first $20,000 in your OA earns an additional 1% interest (or 2% if you are 55 and above), giving you an effective rate of 3.5% to 4.5% p.a. on that tranche. This extra interest is credited to your SA or RA to build retirement savings.

What is the latest CPF SA and MA interest rate in 2026?

From 1 July 2026 to 30 September 2026 (Q3 2026), the CPF SA and MA interest rate is 4.0% p.a.

Both rates are computed based on the 12-month average yield of 10-year Singapore Government Securities plus 1%, subject to the 4% p.a. floor. The rate is reviewed quarterly.

The 4% floor on SMRA rates has been extended again to 31 December 2026, giving members certainty on returns through a volatile interest rate environment.

Bonus interest applies the same way as it does for the OA. Members below 55 earn an extra 1% on the first $60,000 of combined CPF balances. Members 55 and above earn an extra 2% on the first $30,000, then an extra 1% on the next $30,000.

Note on SA closure for members 55 and above: Since 19 January 2025, the SA will be closed when a member turns 55. Their SA savings are transferred to the RA up to the Full Retirement Sum, with any excess moved to the OA.

What is the latest CPF RA interest rate at age 55 and above?

From 1 July 2026 to 30 September 2026 (Q3 2026), the CPF RA interest rate is 4.0% p.a.—the same base rate as the SA and MA. With bonus interest, the effective rate can reach up to 6% p.a. for members aged 55 and above.

The RA is formed at age 55 by transferring savings from the OA and SA to meet the prevailing Full Retirement Sum.

RA savings used to pay for premiums of CPF’s annuity scheme, CPF LIFE, will continue to earn the prevailing CPF interest rates. The interest earned is factored into members’ monthly payouts even after payouts have commenced.

Effective CPF interest rates for members aged 55 and above

The 4% floor extension to 31 December 2026 applies to RA savings as well, including amounts already committed to CPF LIFE.

CPF interest rate history: how have they changed over the years?

CPF interest rates have remained remarkably stable over the years. Since July 1999, OA interest rate has held a floor of 2.5% p.a., while SA and RA have held a floor of 4% p.a. From October 2001, the floor rate of MA increased from 2.5% to 4.0% p.a.

These rates have historically outperformed many low-risk savings products in Singapore, which is part of why CPF remains a core retirement building block.

In recent quarters, the SMRA formula (12-month average 10YSGS + 1%) has occasionally produced rates above the 4% floor. The CPF Board paid 4.08% in Q1 2024, 4.05% in Q2 2024, and 4.14% in Q4 2024. Since Q1 2025, the formula has stayed below 4%, and the floor has held the rate steady at 4%.

The government has extended the 4% SMRA floor to 31 December 2026, providing certainty through the current rate environment.

How can you maximise your CPF interest earnings?

Three practical levers can meaningfully grow your CPF interest earnings over time.

Transfer your OA to SA: Transferring surplus OA funds to the SA captures the higher risk-free return. Consider $10,000 transferred at age 30 and left untouched until age 55. At 4.0% per annum in the SA, the balance grows to approximately $26,700. At 2.5% in the OA, it reaches roughly S$18,500. The difference—around $8,100—reflects the effect of 25 years of compounding on what appears to be a modest rate gap.

Make voluntary cash top-ups to your SA or RA. Regular top-ups grow your retirement savings at SMRA rates and may also qualify for tax relief under the Retirement Sum Topping-Up Scheme.

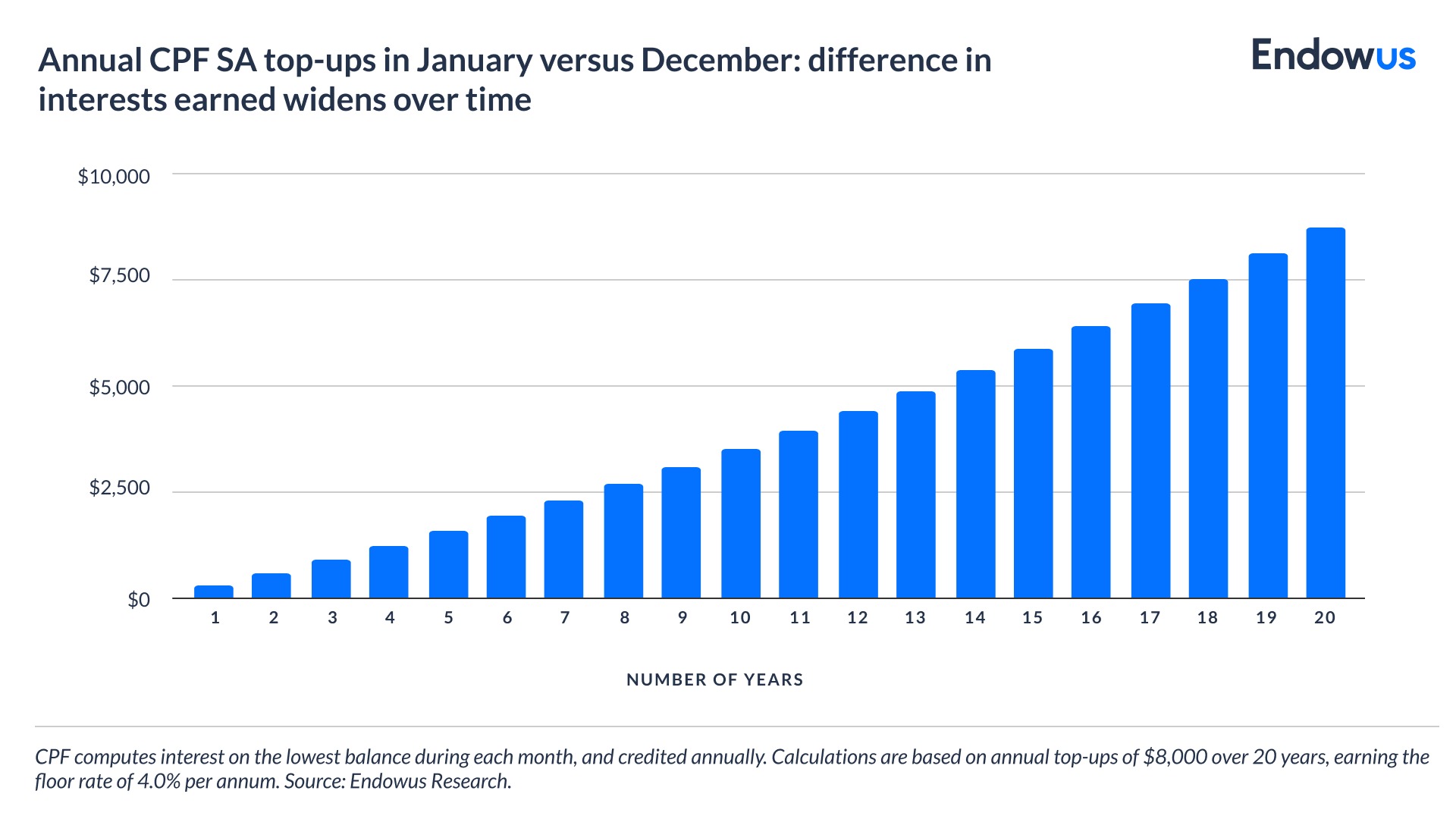

Top up early in the year, not late. CPF interest is computed on the lowest monthly balance and credited annually. A January top-up captures a full year of interest; a December top-up earns almost none for that year. For $8,000 contributed annually to the SA at 4% over 20 years, the January timing yields over $8,700 more than the December timing.

If you want to aim higher than CPF OA's 2.5% floor, you can also invest your OA savings via the CPF Investment Scheme (CPFIS). Over the long term, a globally diversified equity portfolio has historically delivered returns above the OA rate, though with higher short-term volatility.

All in all, the earlier you start, the earlier your returns begin to compound. With effective CPF rates of up to 5% p.a. for members below 55 and up to 6% p.a. for those 55 and above, even modest contributions compound significantly over decades. Saving $100 a month from age 26 at a 4% annual return accumulates over $116,000 by age 65. Wait until age 36 to start, and you would need to save approximately $170 a month to reach the same amount.

Frequently asked questions about CPF interest rates

What is the CPF interest rate in 2026?

In 2026, the CPF Ordinary Account earns 2.5% p.a., while the Special, MediSave, and Retirement Accounts earn 4% p.a. from 1 July 2026 to 30 September 2026. Members can earn additional bonus interest of up to 2% on eligible balances.

How is CPF OA interest calculated?

The CPF OA interest rate is calculated as a three-month average of major local banks' interest rates, using a formula of 80% fixed deposit rates and 20% savings rates. It is reviewed quarterly, with a legislated floor of 2.5% p.a..

When is CPF interest credited to my account?

CPF interest is computed on your lowest monthly balance and credited to your account annually, on 1 January of the following year. This is why topping up in January rather than December can meaningfully boost long-term interest.

Will the CPF OA interest rate ever rise above 2.5%?

In theory, yes—the OA rate would rise if the computed three-month average of local bank rates exceeded 2.5%. In practice, this has not happened since the 2.5% floor was set in 1999, as bank rates have consistently stayed below that level.

How much extra CPF interest can I earn?

Members below 55 earn an extra 1% on the first $60,000 of combined CPF balances. Members aged 55 and above earn an extra 2% on the first $30,000, plus an extra 1% on the next $30,000—bringing the effective rate up to 6% p.a. on the first $30,000.

What is the 4% CPF floor extension and when does it expire?

The 4% floor on Special, MediSave, and Retirement Account interest rates has been extended to 31 December 2026. Without this floor, the SMRA rate would theoretically be set based on the 10YSGS + 1% formula. However, it is worth noting that SMRA has continued to enjoy the 4% p.a. despite calculated rates falling below this floor rate since October 2001.

Grow your CPF savings beyond the OA rate

Compound interest is powerful, but the OA's 2.5% p.a. floor sets a hard ceiling on how fast your CPF savings can grow if left untouched. Over the long term, a globally diversified equity portfolio has consistently delivered returns above the OA rate, with the higher short-term volatility cushioned by time in the market.

Invest your CPF OA with Endowus—Singapore's first and leading digital advisor for CPF investing, approved by the CPF Board with fees as low as 0.4% p.a.

To learn more about optimising your CPF savings:

Endowus CPF Portfolios outperform average returns of CPF Investment Scheme (CPFIS)-included funds in 2020

5 Things to know before investing your CPF

Webinar: Starting your CPF Millionaire journey early

%20F1(2).webp)

.webp)

.webp)