.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

.png)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- The diverse preferences and appetites across various asset classes indicate the difficulty of pinpointing "the best investment opportunities" in 2025.

- Fund managers favour public market equities and fixed income, with private equity and private credit gaining popularity for diversification.

- US equities are the preferred equity market after two years of strong gains. Despite concerns about inflation and geopolitics, traditional inflation hedges like real assets are not a priority.

- Quality stocks are favoured over growth stocks in 2025. Fund managers expect quality stocks, with consistent earnings and strong financials, to outperform in 2025 amid economic uncertainties.

- The AI and robotics theme remains popular among fund managers, driving the tech stock rally and leading to the emergence of the "Magnificent 8" tech companies. The cybersecurity theme ranked second.

Endowus conducted a market outlook survey with over 50 fund management companies in December 2024, in hopes of sentiment and pulse of what risks and opportunities lie ahead in the next 12 to 24 months. Among the questions asked were their expectations on Trump’s administration and policies, inflation and growth of the two largest economies – the US and China in the face of the regime shift, as well as whether a smoother rate-cutting path of the US Federal Reserve will be coming.

Read Part I here about macroeconomic observations, interest rate path, as well as top risks in the markets in 2025.

Opportunity set: Public to private, equities to fixed income

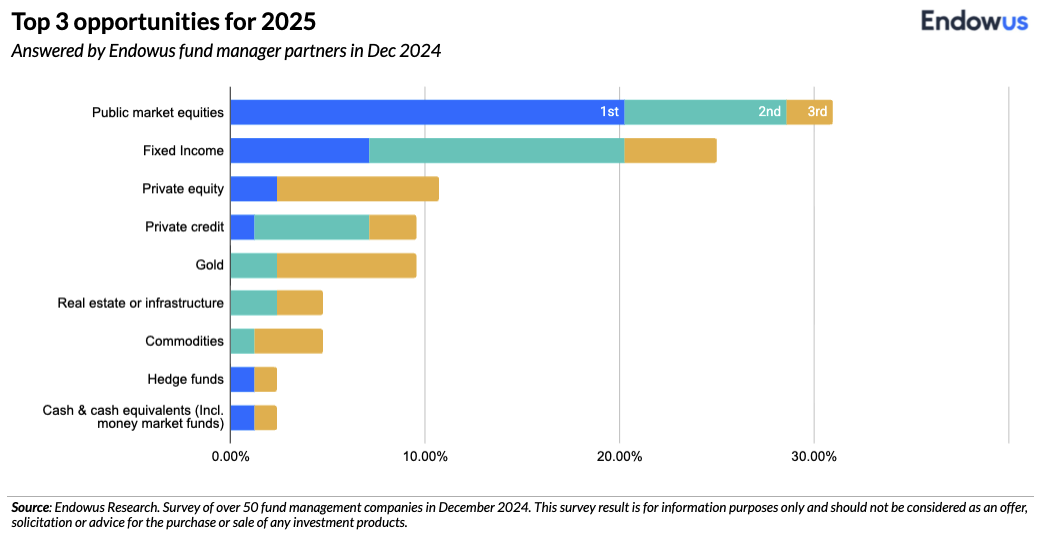

The diverse preferences and appetites across various asset classes indicate the difficulty of pinpointing “the best investment opportunities” each year, and the landscape in 2025 is no exception.

One in five fund managers picked public market equities as their most preferred asset class in 2025, and more than 30% believed it ranks as among the best three opportunities. Fixed income trailed behind as the second best, representing 25% of the managers.

While inflation and geopolitics are ranked among the top three concerns in the same survey, the traditional inflation-hedging real assets – such as gold, real estate, infrastructure, and commodities – were not top-of-mind asset classes for allocation. Only a single-digit percentage of fund managers ranked them as second or third best.

Money market funds and other cash equivalents were chosen as the best opportunity by a small fraction of the respondents against the backdrop of fleeting cash yields and reallocation to other fixed income assets.

Alternative solutions show varied levels of interest. Private equity and private credit strategies are ranked third and fourth altogether, respectively, as the need for portfolio diversification continues to rise.

Corporate bonds are favoured across the credit spectrum

Within the fixed income space, corporate bonds across the credit spectrum are generally favoured. About a third of the fund managers picked investment grade credit as the sub-asset class with the most opportunities. Historically, investment grade corporate bonds have performed well in an environment with falling interest inflations, slowing growth, and rate cuts. High yield credit followed with 25% of the managers picking this asset class.

In search of higher yields, the risk appetite for bond investors remains elevated and high yield corporate is not the only hunting ground. Emerging markets were the top opportunities for 18% of the managers. While government and quasi-sovereign issues were the least popular, the sub-category received 11% of the votes.

Shifting sentiment: A staunch supporter of US exceptionalism or a follower of momentum?

In our 2023 survey, when asked the same question, the favourite equity market among respondents was emerging markets, followed closely by China. US equities were a distant fourth. This year’s results marked a significant shift from the sentiments expressed, and US outperformance – delivering returns of more than 20% for two consecutive years perhaps played a large part in the preference.

On one hand, an increasing number of daily market commentaries vie for acting as the harbingers warning about the stretched valuations in the US. Despite this, US stocks continued to be the much clearer geographical favourite among investors.

In contrast, Chinese equity markets, confronted by a slew of endogenous structural and economic issues, recorded a comeback after several weak calendar years. These factors combined have seemingly hindered the restoration of investor confidence in China and emerging markets as a whole.

Growth delivered. Will value and quality style too?

A narrow band of a tremendous rally continues to be fuelled by a mega-sized artificial intelligence stock boom. Growth style remained a mainstay in global equity returns.

There was an expectation that the interest in growth stocks would wane, making way for quality and value styles to return. Despite the repeated and wishful use of the word “rotation” for some, what actually rotated in 2024 was consistently the market cap ranking among the Magnificent 7 stocks. AI chip heavyweight Nvidia Corp made multiple attempts to dethrone Apple Inc. as the world’s most valued company, while Tesla Inc. went through ups and downs.

The tremendous rally in mega-sized technology stocks was driven by the artificial intelligence boom. BATMMAAN silently arises – the new grouping refers to Broadcom, Apple, Tesla, Microsoft, Meta Platforms, Amazon.com, Alphabet, and Nvidia. In other words, the “Magnificent 8.”

An overwhelming majority of fund managers (70%) bet on quality stocks to outperform relative to other styles and factors in 2024. This year, 54% of fund managers expect quality to outperform, followed by value and small-cap stocks.

Quality companies typically have consistent earnings and robust financial statements. These characteristics could help companies navigate the challenges such as stringent monetary policies, escalating debt levels, and declining consumer spending. These companies are likely to also provide some downside protection in an uncertain investment environment.

Artificial intelligence as a theme also garnered the most support (41%) from fund managers as it not only outperformed other structural investment themes but the broad market index in 2024. With a wider adoption of artificial intelligence and robotics across different industries, the demand for cybersecurity and data protection is also on the rise, representing 19% of managers.

Last word: Are you FOMO for BATMMAAN?

The rosy outlook for growth and the seemingly unbeatable nature of US equities appear promising. Catchphrases surrounding the Magnificent 7 stocks and the emergence of the new BATMMAAN group adds to new rounds of the “fear of missing out”. However, history has taught us painful lessons about the dangers of recency bias and the downsides of concentration.

Forecasts are inherently uncertain. The divergence in views expressed by fund managers make it challenging to draw a consensus on where the best opportunities lie.

Rather than best opportunities, one should be after an allocation best-suiting one’s risk tolerance and financial needs and wants based on the unique financial circumstances. What one can be reliant on is a globally, sectorally diversified approach to investing.

One of the main benefits of global diversification is the ability to access a wide range of investment opportunities. Different regions and countries may experience varying economic cycles and market conditions. By investing globally, investors can take advantage of potential growth opportunities in different parts of the world while reducing their exposure to any single market.

To get started with Endowus, click here.

Webinar: 2021 Global outlooks and market trends

Lessons from past bear markets with Barton Biggs

Webinar: Endowus Insights 2021: Paving a new way forward

%20F1(2).webp)

.webp)

.webp)