.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

.jpg)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

It is easy to assume that those closest to the markets have their personal investments figured out, especially in a city like Singapore, where news and money both travel at a lightning speed.

The quiet irony is that the opposite is common. At Endowus, we hear stories of people in banking and finance who spend their days analysing the market and doing buy and sell trades by day, yet default to holding cash or rolling over fixed deposits when it comes to their own money. Lack of time and energy is often cited as a reason.

Alex, a 38-year-old finance professional in CBD, Singapore, in our diary story is not one person, but a reflection of many. This diary brings together those shared experiences – the hesitation, the overthinking, the quiet discomfort.

27 October, the embarrassing lunch

Mood: A bit sheepish.

Recounts a casual lunch with a colleague who was excitedly discussing their portfolio’s performance.. I just nodded along. When they asked what I was into, I mumbled something about “playing it safe.” The truth? My salary goes into my bank account, and every 3-6 months, I roll over my fixed deposit.

For someone who analyses markets for a living, it’s deeply embarrassing. The classic “cobbler's children have no shoes” scenario. Retirement feels like a problem for a future, less-tired version of me.

29 October, the “analysis paralysis” doomscroll

Mood: Overwhelmed.

Spurred on (or inspired?) by Monday's lunch, I spent an hour after work “researching.”

Fell down a rabbit hole of market news, analyst reports, and conflicting opinions. One headline says China is poised for a rally; another predicts a correction. It feels like both sides make sense, but neither is actually helping me decide. I had 18 tabs open—slightly better than my work laptop, but with zero conviction.

It feels like every time I’ve considered buying, it’s been at a peak. I have a few stocks I bought on a whim over the years—no rhyme or reason, just a hot tip from a group chat. It’s a portfolio that looks like a garage sale. I closed all the tabs. Ordering from Grab is an easier decision, and I still have coupons that I can use (it’s how they trap you).

7 November, the “someday” trap

Mood: Procrastinating.

It’s been over a week. I promised myself I’d sort out my finances. But a huge deal came up at work, and I’ve been pulling 14-hour days. The thought of spending my Saturday morning figuring out ETFs versus mutual funds feels like a punishment.

I know that my cash flow is sufficient for my lifestyle today, but how much do I need in retirement? At this rate, when can I even afford to retire? It's so easy to just let it slide, to tell myself I'll deal with it “when things quiet down.” But when does that ever happen in Singapore? I keep telling myself I have time. I’m starting to wonder if that’s just a story I tell to feel better. It's the weekend, and I should start soon. Hate to see that my “do more with my money” plan is perpetually pushed to someday, but I’d rather rest…

18 November, a different kind of advisor

Mood: Cautiously optimistic.

A colleague at work recommended I speak to an independent wealth advisor. My first thought was, “I don't have time for that.”

But I went. I laid it all out: the long hours, the fixed deposits, the random stocks, the fear of buying at the top. The advisor didn't judge. Instead, they asked about my life, not just my money. What did I want in 5 years? 10 years? Did I want to buy property? Travel more?

Instead of asking what I wanted to buy, they asked what I wanted my life to look like and what I am actually investing for.

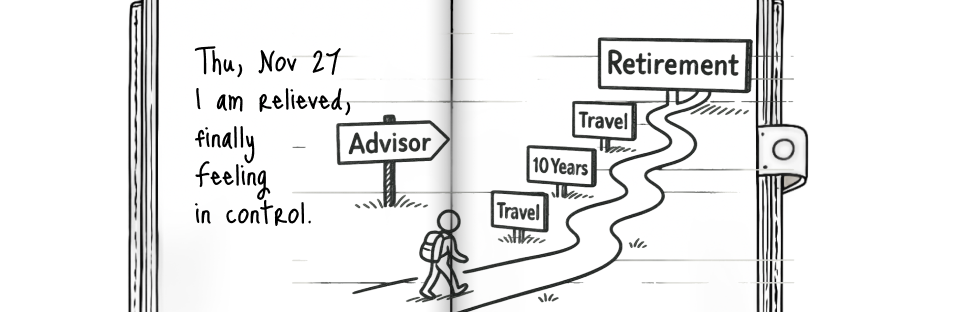

27 November, the plan is the point

Mood: Relieved. In control.

Had my follow-up meeting. We built a real plan. Not a get-rich-quick scheme, but a disciplined, automated strategy. A portion of my salary now gets invested automatically each month. It's globally diversified and aligned with the goals we discussed.

The biggest revelation? The goal isn’t to be a stock market genius. It’s to have a system that works for you, especially when you don't have the time or energy to manage it yourself. For the first time, I feel like my personal finances are finally catching up with my professional life.

Investing well does not have to mean doing more

Alex’s story is familiar to many in the industry. It’s not about a lack of knowledge—it’s about time, energy, and the mental space to make decisions for yourself.

The good news is, investing well does not have to mean doing more. One way is to put the best outcome along the path of least resistance by making investing simple, easy and automatic. Importantly, it needs to be aligned with what matters to you.

The math isn’t hard, and the benefits are clear. For finance professionals who’ve been putting their own goals on hold, there’s a way to move forward with clarity and confidence. Endowus is here to help make that easier.

Read more: The science behind why we are bad at saving for retirement

Retiring with a bucketing strategy

Webinar: Wealth — the wellness trend for women

Sparking joy: How to Marie Kondo your finances

%20F1(2).webp)

.webp)

.webp)