.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

.png)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

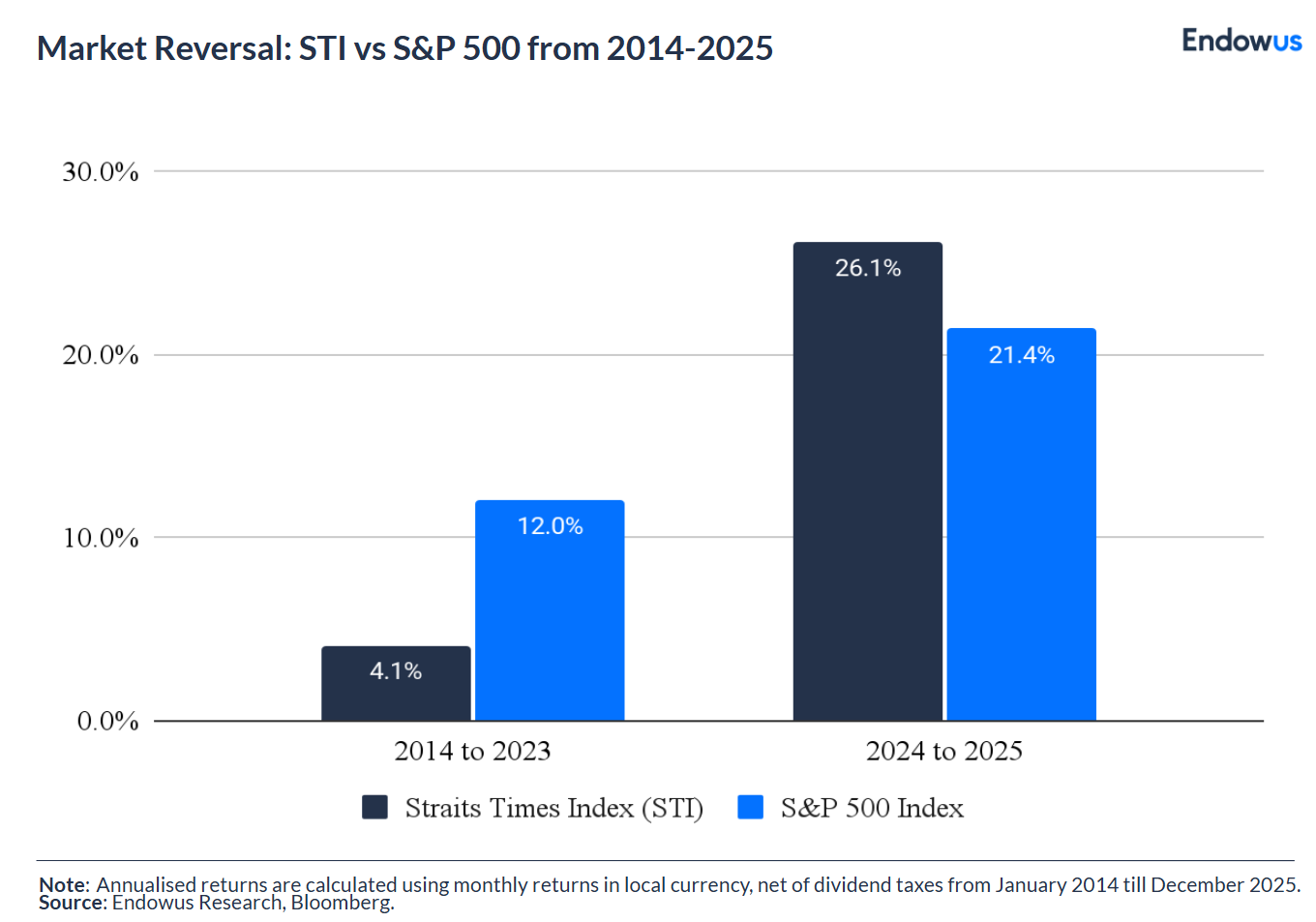

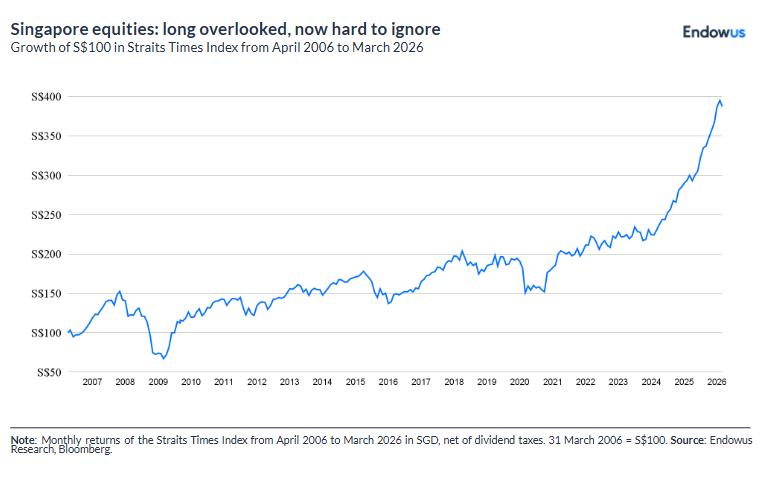

- The Straits Times Index ("STI") has been historically underinvested, lagging the more growth-oriented S&P 500 in performance in the decade between 2014 and 2023. More recently however, the performance has improved, with the STI crossing 5,000 for the first time in February 2026 and outperforming the S&P 500 in SGD terms in 2025.

- Substantial efforts are ongoing to revitalize the Singapore market, including a large injection of public money through the MAS's S$6.5 billion Equity Market Development Programme ("EQDP"), with the goal of increasing liquidity and public exposure especially for the less-owned, more under-researched corners of the market.

- The Endowus Investment Office has curated a selection of Singapore equity funds—including EQDP-mandated strategies—available on Endowus Fund Smart, for investors seeking targeted domestic exposure alongside their global portfolio.

Singapore's stock market has a recent history of underperformance compared to equity markets in the United States—especially as growth stocks became the predominant component of the investment universe.

In the decade between 2014 and 2023, the S&P 500 grew by 12.0% on an annualised basis. In comparison, the Straits Times index, which includes the top 30 companies listed on the Singapore Exchange (“SGX”) grew by only 4.1% annualised.

This was not necessarily due to deteriorating fundamentals, but reflected investors mainly seeking “growth” exposure through technology names abroad. This trend decreased SGX capitalization, fueling a vicious circle of derating, capital flight and further price depression.

Conditions began to change in 2024, with the STI returning 26.1% annualised over the 2024–2025 period and crossing the 5,000-point mark for the first time in February 2026. Over the same two years, US stocks (as measured by the S&P 500 index) returned 21.4% annualised, and global equities (as measured by the MSCI ACWI index) returned 20.4% annualised, both trailing Singapore's market.

*Note: ^The index value of the Straits Times Index, which refers to the free-float market capitalisation-weighted performance of its constituent stocks.

For investors who have long viewed Singapore equities as the steadier, less volatile—but also less exciting —sleeve of a portfolio, this may be welcoming news.

However, the real question is whether this rally can be sustained, and what could be the drivers of a more structural re-rating of—for Singaporean investors—domestic stocks.

Singapore’s financial markets structural issues

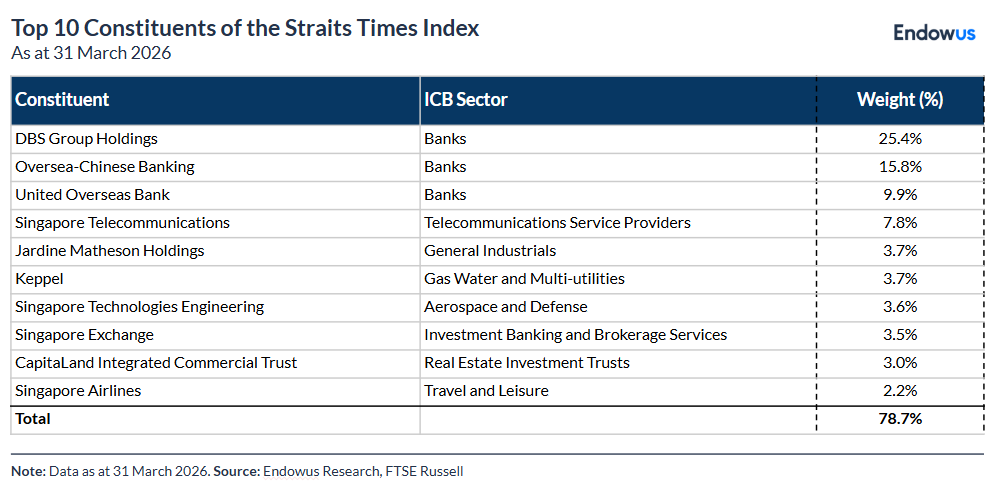

Singapore’s equity market has been plagued for many years by factors that limited its full potential. Besides low liquidity and its high level of concentration in the low-growth financial sector, an additional obstacle to long-term sustained performance is the decreasing number of new IPOs. Even successful, local high-growth tech startups—such as Grab and Sea Group—chose to list on foreign exchanges in search for deeper capital pools and higher trading volumes. So bad was the situation that at some point, delistings were outpacing new listings, slowly shrinking the market's depth—yet an additional threat to potential diversification—contributing to the downward spiral.

On the issue of concentration, the combined STI index weight of the three local banks (DBS, OCBC, and UOB) is higher than 50%, which incidentally means that hundreds of smaller listed companies have remained unresearched. This created a self-reinforcing dynamic. Without research coverage, institutional investors, which typically provide liquidity, stayed clear. The limited liquidity in turn made these smaller companies unsuitable for retail players, who as a result stuck to the familiar blue chip firms.

Corporate behaviours also did not help valuations. According to The Straits Times, 57 per cent of the listed companies on the mainboard and the Catalist board of the SGX are trading at a price-to-book ratio below 1—meaning investors believe each one of these companies is worth less than the sum of its assets. And Singapore's smaller listed companies are not just trading at historically steep discounts, they are also attractively priced relative to comparable companies on the other side of the world: a typical US small-cap stock trades at a price-to-book ratio of 2.29 times, based on the Russell 2000 Index as of 31 March 2026.

The reason for this gap is that, historically, most Singapore’s corporations treated cash as a safety net rather than a working asset, while never being pressured to prove that keeping profits in the business creates more value than deploying it productively, or returning them to shareholders (via dividends or share buybacks). This is precisely one of the issues Singapore's reform agenda is designed to address.

Government intervention to push equity markets re-rating is not a new strategy. Other countries have implemented it successfully in the past—namely Japan and Korea.

Japan’s experience in particular shows the benefits of nudging companies to put cash to work. After a decade of governance reform that raised expectations around capital efficiency, corporate share buybacks in Japan are on track to reach an all-time high in fiscal year 2025, beating the previous year record for the fifth time in a row.

Singapore's EQDP, alongside complementary measures like the S$30 million "Value Unlock" package and the enhanced Grant for Equity Market Singapore (“GEMS”) research grant, is attempting to produce—and in a way it already has—similar results.

Enter EQDP

The Equity Market Development Programme (EQDP) is an attempt by the Singaporean government to increase the local market’s attractiveness for both investors (demand) and potential new listings (supply). The initiative is government-funded and its direct, practical goal is to incentivize the local fund management industry to increase participation in Singapore-listed equities. In practical terms, MAS and the Financial Sector Development Fund (“FSDF”) allocate capital to Singapore-based asset managers that manage equity strategies focused on Singapore-listed stocks, and more specifically on small and mid-cap companies that have historically been under-researched and under-owned.

The original financial commitment was S$5 billion, which was expanded to S$6.5 billion in the 2026 Budget, an indication that the government has confidence in the potential re-rating this initiative could produce. As of early February 2026, MAS had already allocated S$3.95 billion across nine appointed asset managers and plans to select the next batch of EQDP members around mid-2026.

The programme is still in its early stages, but there are already encouraging signs that the dynamic is starting to shift.

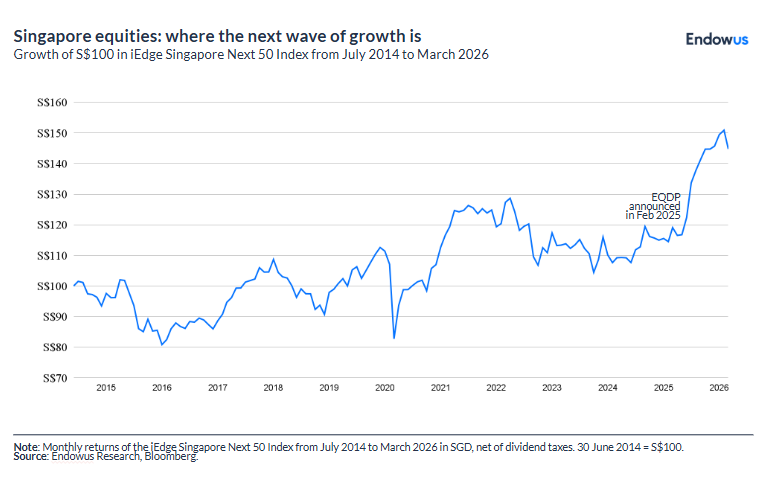

Beyond the headline STI performance, institutional interest in the mid-cap segment, which refers to companies ranked just outside the top 30 by market capitalisation, has also begun to pick up. One useful barometer for this is the iEdge Singapore Next 50 Index, which tracks the performance of the 50 next largest companies listed on the SGX Mainboard, just below the 30 large-caps included in the STI. This segment is more diversified than the STI itself, with meaningful exposure to REITs, industrials and domestically anchored businesses. It is also where the EQDP’s focus on improving liquidity and research coverage is likely to have the most tangible effect.

Early institutional engagement with these mid-cap names has started to improve, suggesting that the EQDP’s capital deployment is beginning to draw attention to parts of the market that have long been overlooked. If Singapore’s experience follows the pattern seen in Japan and South Korea, where policy-driven reforms triggered a sustained re-rating that started in mid-caps before broadening out, the iEdge Next 50 may prove to be one of the more interesting spaces to watch.

Singapore’s reforms: a comparison with Japan and Korea

Singapore is not the first market in the region to attempt this kind of reform-driven transformation. As noted above, and more in detail here, Japan and Korea have already gone through a cycle of corporate governance reforms, which were implemented with the goal of decreasing local market discounts.

The key takeaway is that for both countries, these reforms worked, but took time to affect prices.

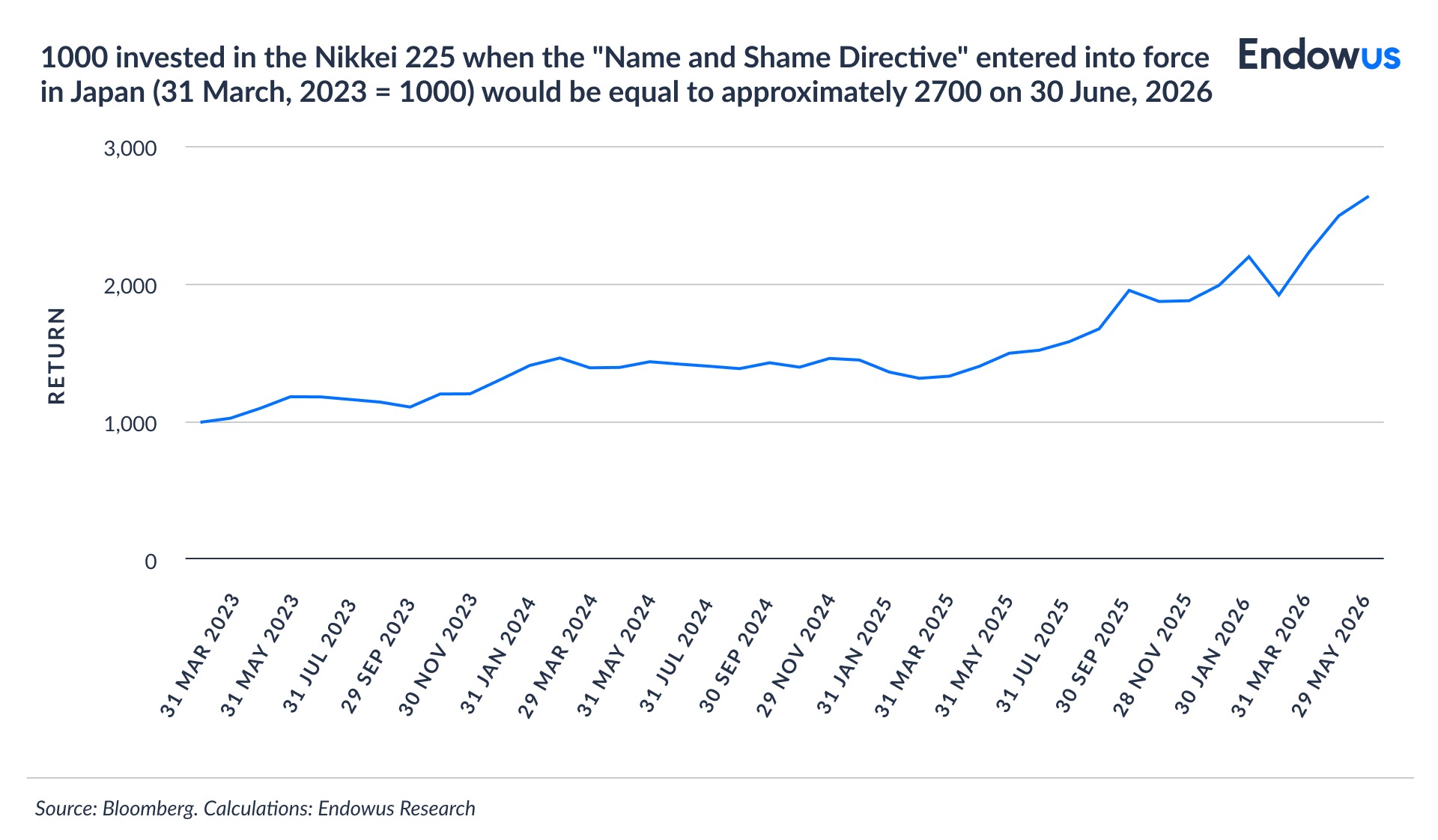

Japan started in 2014 with the Stewardship Code, followed by the 2015 Corporate Governance Code. The real turning point did not come until the 2023 “name and shame” directive from the Tokyo Stock Exchange (“TSE”), which forced companies to manage cost of capital actively. Eventually, this sustained pressure eventually saw Japanese equities surge to record highs in 2025.

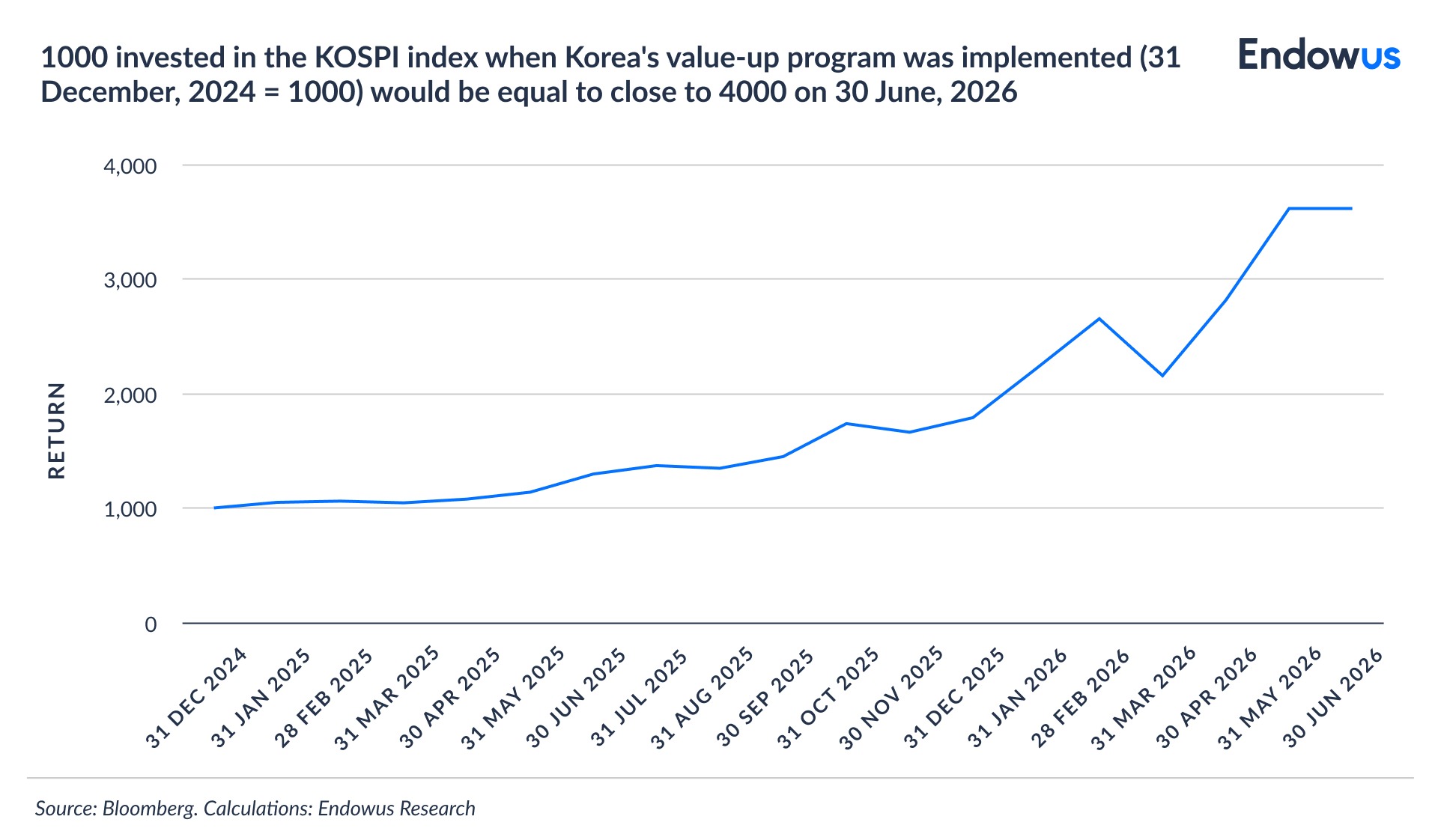

Korea’s program—launched in 2024—mirrored Japan’s by encouraging voluntary disclosures and offering tax breaks for shareholder returns. By 2025, South Korea became the top performer in emerging markets equities, generating a sharp 79.2% return in local currency terms, with continued upside in the first half of 2026. Korea’s stellar performance is also heavily correlated with the strong momentum of its semiconductor industry, and benefits from an engaged retail investor base.

Having noted the differences, the analysis of how policy moves in both these countries affected equity market valuations allows us to draw a useful comparison with Singapore. While Japan and Korea focused on “supply-side” reforms—pushing companies to improve from within, Singapore EQDP intervened directly on the demand side, with S$6.5 billion of institutional capital deployed through appointed fund managers, and a S$50 million commitment to strengthen research coverage, a direct funding pool that has no equivalent in the Japanese or Korean playbooks.

Japan and Korea’s reforms also took over a decade to fully bear fruit because they relied on voluntary corporate participation. Singapore’s approach aims to compress that timeline by injective capital directly, but for long-term success it will also require genuine improvements in earnings quality and transparency.

Beyond capital injections and improved transparency, Singapore must also address its structural IPO pipeline challenge. This lack of high-growth listings—SGX has yet to become the magnet for regional tech unicorns—remains a concern and needs to be overcome for this momentum to become a “secular growth story.”,

On the positive side, given the relatively small size of Singapore’s S$1 trillion market, a S$5 billion capital injection represents a substantial boost—even more so as the firepower is concentrated on small and mid caps. In percentage of market cap, EQDP dwarfs Japan and Korea’s efforts.

What does this mean for Singapore investors?

For most Singapore-based investors, the local equity market has rarely been the most exciting allocation in their portfolio. Global diversification, particularly into high-growth US equities, has been the dominant narrative for the better part of the last decade.

However, with help from the EQDP, there may be an opportunity in value names—a factor that, in the long run, outperforms growth according to prevailing research. This makes local names beyond major banks potentially attractive. Beyond that, there is government buy-in to make Singapore’s market more attractive to both companies and investors—together with the Value Unlock programme, improved research coverage through GEMS, and the upcoming SGX-Nasdaq dual-listing bridge.

Finally, for investors with SGD-denominated liabilities, the currency effect is not trivial. MAS's exchange rate-based monetary policy has historically resulted in a steady SGD appreciation vis-a-vis the USD, which may potentially underpin SGD-denominated assets going forward. For Singapore investors, a weakening US dollar would erode a portion of USD-denominated returns. In contrast, locals invested in the STI would not bear any currency exchange risk.

None of this means Singapore equities should replace global diversification, but for Singapore-based investors, it is worth considering some exposure to the domestic market due to this combination of traditional strength and meaningful reforms that can unlock rerating.

Accessing Singapore equities through funds On Endowus

For investors who want to participate in Singapore's equity market, there are a few clear ways to do so through Endowus. Endowus has been among the first in the industry to provide access to EQDP funds, partnering with the leading fund management partners to onboard and screen to offer potentially attractive exposure to Singapore equities through third-party funds.

Singapore equities as a satellite allocation

Because of the size of the exposure, adding EQDP exposure to a portfolio better works as a focused and intentional position that complements your core global portfolio.

Think of your portfolio in two layers. Your core captures broad, long-term global diversification across geographies and asset classes. Your satellite positions allow you to take a more targeted view on a specific theme, region, or opportunity. Given the structural tailwinds from the EQDP, the improving governance environment, and the re-rating potential in Singapore's small and mid-cap space, Singapore equities make a compelling satellite case today.

Why Singapore’s market structure matters for how you invest

Not all equity markets are built the same, and Singapore’s is heavily concentrated in the three largest financial names—DBS, OCBC and UOB—together constituting more than half of the entire benchmark.

For passive investors, a low-cost STI index fund or ETF is a straightforward, efficient way to own this large-cap universe. On the Endowus platform, the Amundi STI Index Fund offers a cost-effective, SGD-denominated fund that tracks the STI, giving investors clean exposure to Singapore’s 30 largest listed companies.

But this very concentration creates an interesting dynamic when it comes to the rest of the market. Outside the top 30, Singapore looks very different: hundreds of companies across REITs, industrials, consumer businesses, and technology, many of which are thinly covered by analysts and under-owned by institutions. These are not necessarily poor businesses, they are simply overlooked ones, which means they tend to be mispriced.

Where active management has an edge

Due to this unique setup and the nature of a single country, small sized market, it is precisely why active fund management could have the potential to add value. In large, liquid, well-covered markets like the US, active managers struggle to consistently outperform because information is widely available and almost instantly reflected in prices. Singapore’s mid and small-cap segment is the opposite: sparse research coverage, low institutional ownership and companies trading below book value because no one has been paying close enough attention.

A skilled active manager operating in this space, identifying companies with improving fundamentals ahead of broader market recognition has a genuine opportunity to generate returns beyond a passive benchmark. This is exactly the kind of mandate the EQDP-appointed managers are pursuing and why the programme specifically requires a meaningful allocation to small and mid-cap names.

Empirical evidence suggests that even in small markets like Singapore—and especially if the overall market does well—there is a high likelihood that by the law of averages some of these EQDP fund managers will outperform and others will underperform.

Therefore the need for an independent advisor to provide some guidance in choosing between the increasing number of funds launched in this program becomes even more evident and essential. This is where Endowus and its Investment Office comes in. The 13-people strong Investment Office is a unique value proposition for our clients, with its dedicated team focused on institutional grade fund manager selection, fund due diligence to portfolio creation and optimisation.

In practice, this suggests a layered approach. A passive STI fund works well as a cost-efficient foundation for large-cap Singapore exposure. An actively managed Singapore equity fund with a small and mid-cap tilt sits alongside it as the more targeted satellite position, one where the fee is justified by the genuine alpha potential in the less efficient parts of the market.

Using Cash and SRS

A distinctive advantage of investing through Endowus is the ability to deploy different sources of savings into the same strategy. Depending on the fund, you may be able to invest your cash savings or Supplementary Retirement Scheme (“SRS”) funds into Singapore equity strategies allowing your retirement savings to participate in the same market opportunity as your everyday portfolio.

Endowus Fund Smart offers 3 EQDP funds: Fullerton Value-Up and LGI Singapore Trust for retail investors and Avanda’s strategy exclusively for Accredited Investors. Find out from your client advisor to learn more.

With no sales and commission fees charged, you can access these funds at the lowest cost in Singapore. Explore Fund Smart now.

Webinar: Investing in a better future: Through the lens of an equity investor

Why ESG investing should matter to Singaporeans

When you can’t see the forest for the trees: A holistic approach to asset allocation

%20F1(2).webp)

.webp)

.webp)