.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

April proved to be a month of striking contradictions: Brent crude ending the month above US$110/bbl despite the mid month pull back, the Strait of Hormuz still severely disrupted, inflation reaccelerating amid higher energy costs—and yet global equity markets staging one of their most powerful monthly rallies in years.

Investors emphatically looked through the geopolitical turbulence to embrace a narrative of resilient corporate earnings, robust AI demand, and the prospect of a durable ceasefire between the US and Iran. The result was a decisive rotation back into technology and semiconductors, reversing much of March's risk-off damage and lifting global equities to new highs.

The Nasdaq surged 15.6%, while the Philadelphia Semiconductor Index rose nearly 40%, reflecting renewed enthusiasm for the AI supply chain. Even at its maximum drawdown in response to the Iran conflict, the S&P 500 had fallen less than 10%, as expectations for strong earnings growth offset declining price-to-earnings valuations.

The macro backdrop remained complicated. The Federal Reserve held interest rates unchanged for a third straight meeting, citing high uncertainty from the Middle East war, in what was likely the last gathering under outgoing chair Jerome Powell. Traders now expect the Fed to remain on hold until 2027.

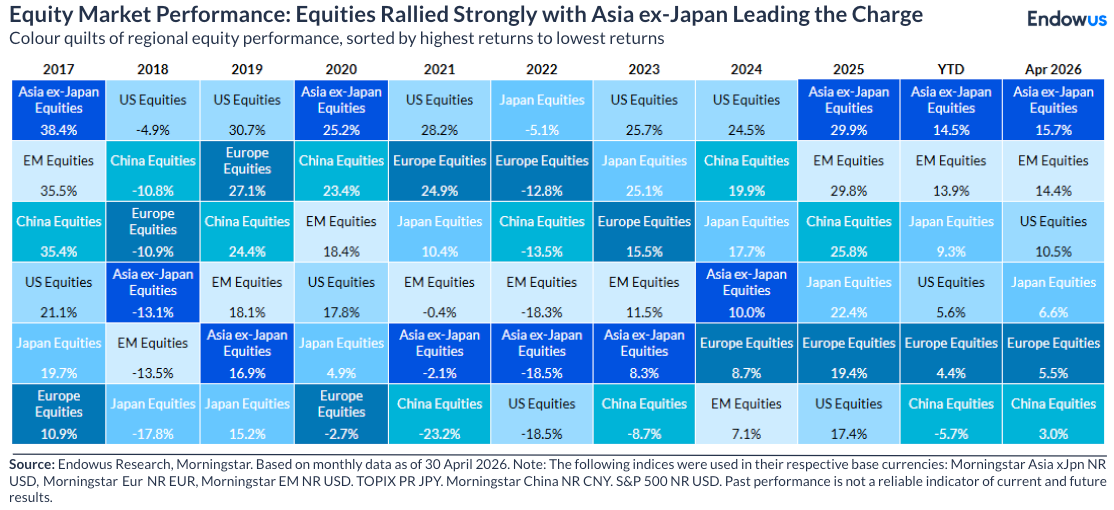

Global equity

From a regional perspective, emerging markets and in particular, Asia ex Japan, were the standout of the month, powered by extraordinary gains in Korea (+34%) and Taiwan (+24%), thanks to the strength in semiconductors. The recovery was also driven by a broad improvement in global risk sentiment, easing trade and growth concerns, stabilising US yields, and a softer dollar, which together supported capital flows back into higher-risk assets.

Asia ex Japan, particularly Korea and Taiwan, continue to be the best performing regions YTD following a strong 30% performance in 2025.

Within developed markets, the US led with the S&P 500 returning 10.5%, driven by a strong earnings season from both technology and financials.

Japan and European equities also rebounded strongly after a sharp decline in March, when markets were pressured by concerns over slowing global growth, elevated energy prices, and persistent inflation.

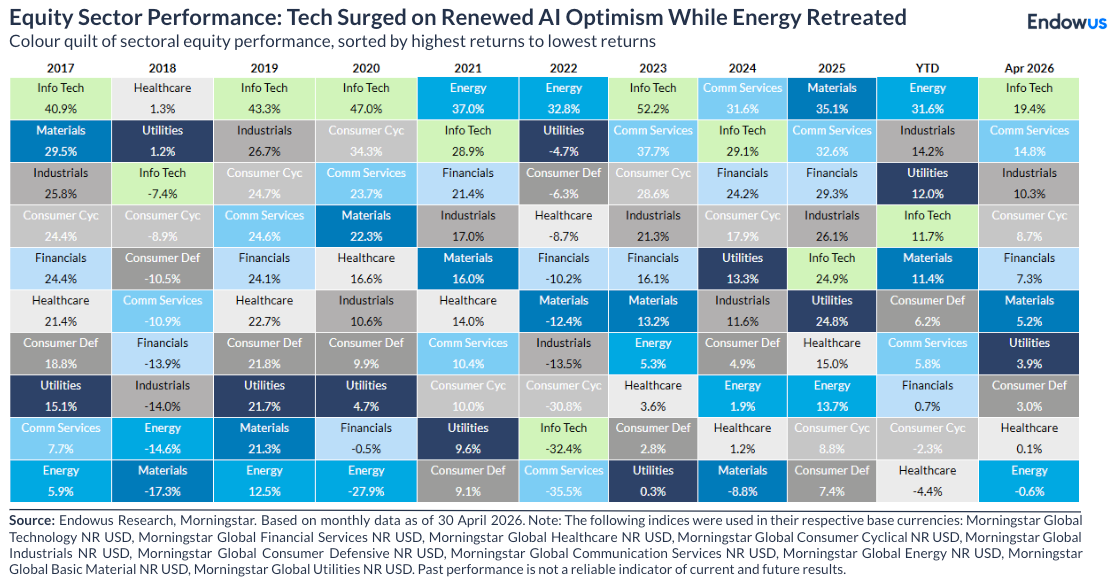

By sector, the rotation was unambiguous.

Investors rotated decisively away from defensive value and yield exposures toward higher-beta, growth-sensitive areas of the market. Across all regions, volatility, momentum, and growth factors outperformed as confidence in the global economic outlook improved. The AI theme reasserted itself powerfully, with semiconductors and hardware leading globally.

The Energy sector was weak in April along with defensive and value sectors such as Healthcare and consumer staples. The energy sector, however, continues to be the best performing sector YTD at +32% as of end April.

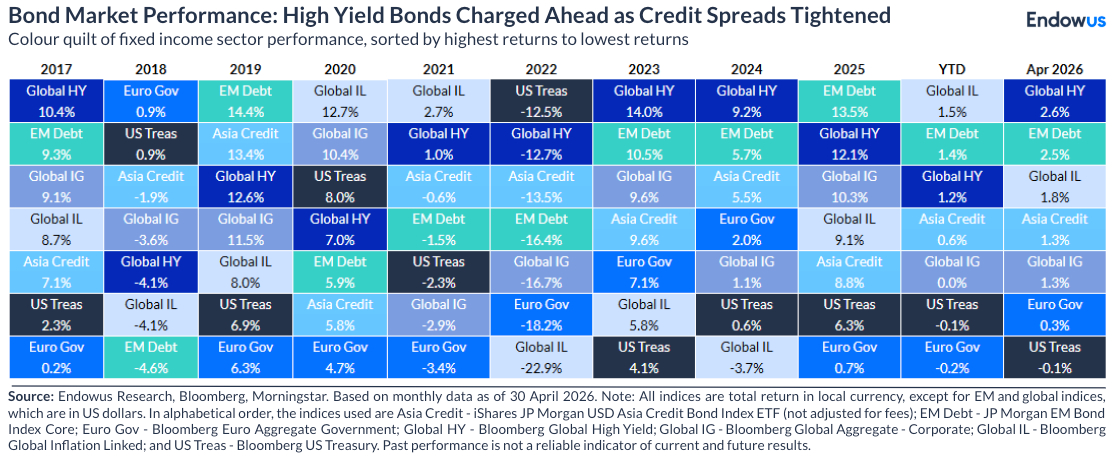

Global fixed income

The fixed income picture in April was more challenging than in recent months, as the sharp rise in energy prices reignited inflation concerns and pushed rate-cut expectations further out the curve.

Government bond markets were mixed in April, with performance largely driven by renewed inflation concerns following the rise in energy prices. Markets moved quickly to reprice the path of monetary policy, with expectations for rate cuts pushed out, or in some cases replaced by expectations for further tightening.

The 10-year US Treasury yield rose to approximately 4.37%, while the 2-year note yield reached around 3.86% for the month. Meanwhile, the 30-year bond yield topped 5.0% at points during the month ending the month at 4.97%.

The Bloomberg Global Aggregate Index nonetheless managed to show a positive return, supported by tighter credit spreads despite the yield move. Global high yield and emerging market debt was the best performing category of the bond market given the risk on recovery and tighter spreads in April.

Commodities

Oil prices remained extremely elevated throughout the month. Brent crude pushed above US$110 per barrel by month-end, with significant intra-month volatility as ceasefire negotiations repeatedly broke down before a tentative two-week ceasefire was announced.

Gold had a notably more muted month, closing April essentially flat at approximately US$4,618/oz. A sizable drop in market volatility—as risk appetite returned—was a major negative contributor, though this was countered by strong ETF inflows, a moderately weaker US dollar, and dip-buying following the sharp March sell-off.

The USD remained under modest downward pressure for much of the month, reflecting the broader risk-on tone, though elevated energy prices and a more hawkish repricing of Fed expectations provided intermittent support at the margin.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)