.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

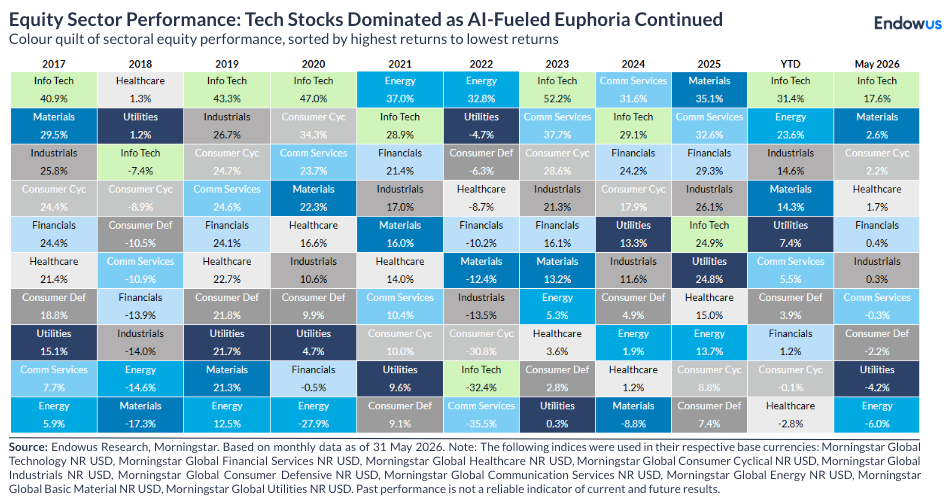

The April AI-driven rally continued in May, with the semiconductor sector posting its strongest two-month run on record and US—along with Japan, Korea, and Taiwan—equities closing at their respective all-time highs on the final day of the month.

Under the surface, however, the picture was more nuanced, with only 3 out of the eleven S&P 500 sectors in positive territory for the month (compared to 9 in April).

A sharp fall in oil prices through the second half of the month—driven by tentative progress in US-Iran peace negotiations—was seen as a potential catalyst to dampen inflation expectations, though market hopes for a more dovish Fed were tempered in early June by strong May nonfarm payroll numbers.

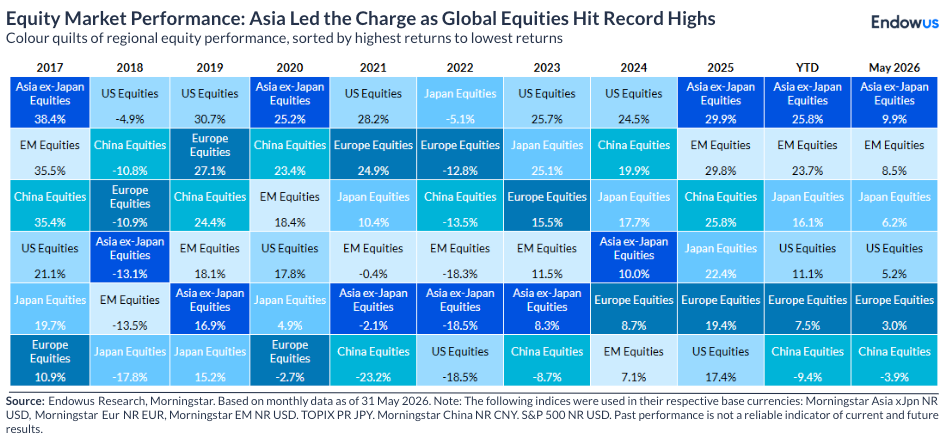

Global equity

The S&P 500 returned 5.4% in May after a 10.4% rally in April, to close out nine consecutive weekly gains. Technology was the dominant sector, driven by robust performance in semiconductors and AI hardware. The Semiconductor Sector (SOX) index gained 22.1% in May following a 38.4% surge in April, for a combined two-month return of 69.1%—its strongest two-month performance since its 1996 launch.

Asia ex Japan markets were once again the standout on a regional basis, returning 9.9% in May, led by Korea (+26%) and Taiwan (+16%), both posting outsized gains for the second consecutive month. Asia's Q1 2026 earnings growth was one of the strongest quarters in recent years, though heavily concentrated in technology and semiconductors.

European equities rebounded to end May on a higher footing (+3.0%), though the region faced headwinds from Middle East-related risks and notably weak macroeconomic data. China equities were the worst-performing major region for the month and YTD, dragged down by the sluggish returns of HK-listed Chinese companies.

By sector, technology continued its rally and was the overwhelming leader in May (+17.6%)—masking broader softness across most other sectors—driven by continued momentum in AI-related spending, semiconductors, and digital infrastructure investments.

Outside of technology, gains were modest, with materials, consumer cyclicals, and healthcare delivering positive returns. However, defensive sectors, energy, and rate-sensitive sectors all underperformed as capital continued to flow into high-beta, growth-oriented names.

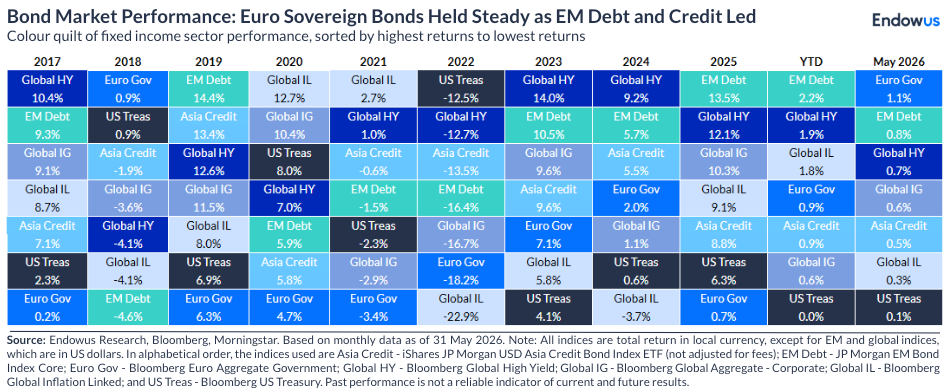

Global fixed income

Fixed income markets were notably more turbulent in May, with yields pushing higher as inflation concerns persisted before the potential relief, towards the end of the month, from lower oil prices. Market participants continued to push back their expectations for Fed rate cuts. The 10-year US Treasury yield ended May at around 4.44%, up 7 bps.

The Bloomberg Global Aggregate Index closed the month marginally up, following significant intra-month volatility. Credit markets held up better than government bonds, supported by solid corporate fundamentals. European bonds posted positive returns as rates moved lower on expectations of an imminent Middle East deal, and euro high yield bonds were the best performers in the fixed income complex. Global high yield and emerging market debt again outperformed, consistent with the broader risk-on tone.

Commodities

The most dramatic development in May was the sharp fall in oil prices through the latter part of the month. Brent crude opened May above $116/bbl before declining significantly as hopes for US-Iran peace progress emerged, with crude prices tumbling on diplomatic signals before partially recovering. At the end of May, Brent fell to $92, a decline of approximately 20% from the highs reached earlier in the month.

Gold had a difficult month, extending its consolidation. From the outset of May, gold faced headwinds as a firmer dollar, rising Treasury yields, and ongoing geopolitical uncertainty pushed gold toward the lower end of its recent range ending the month down 1.7% at $4,540.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)