.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

Global markets surged in October as the artificial intelligence (AI) boom continued to dominate investor sentiment. The tech-heavy Nasdaq closed the month on a strong note, buoyed by record earnings from Amazon, Alphabet, Microsoft, and Meta, each highlighting massive capital expenditure in AI infrastructure.

The rally was not confined to the US—Taiwan’s exports hit a record US$61.8 billion, up nearly 50% year-on-year, driven by demand for advanced chips and AI technologies. Semiconductor and cloud providers remained at the center of the rally, pushing the S&P 500 Index past 6,500 points. Yet, beneath the optimism, concerns about valuations and sustainability linger, introducing volatility toward the end of the month

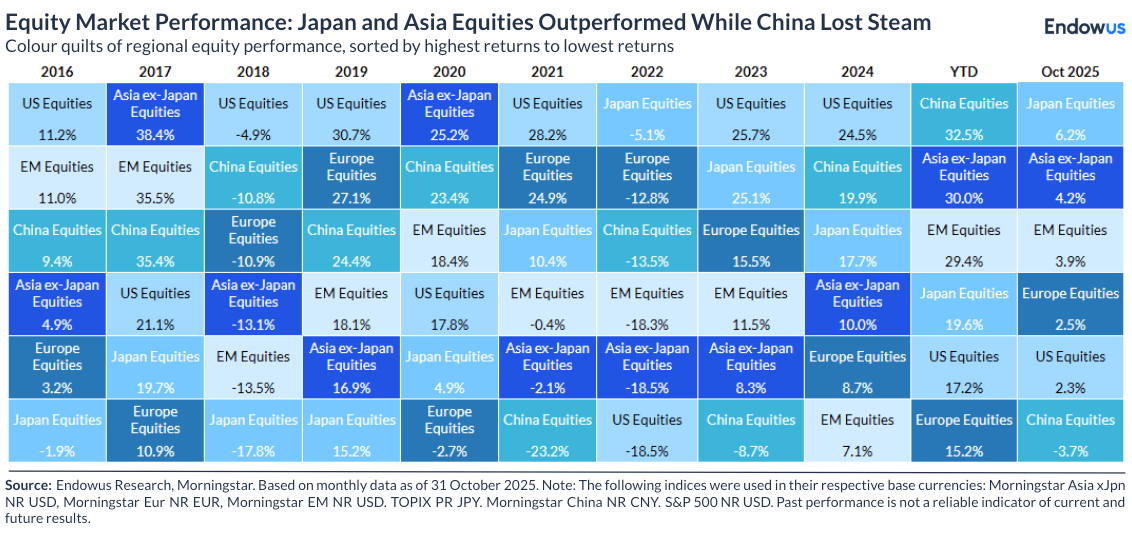

Global equity

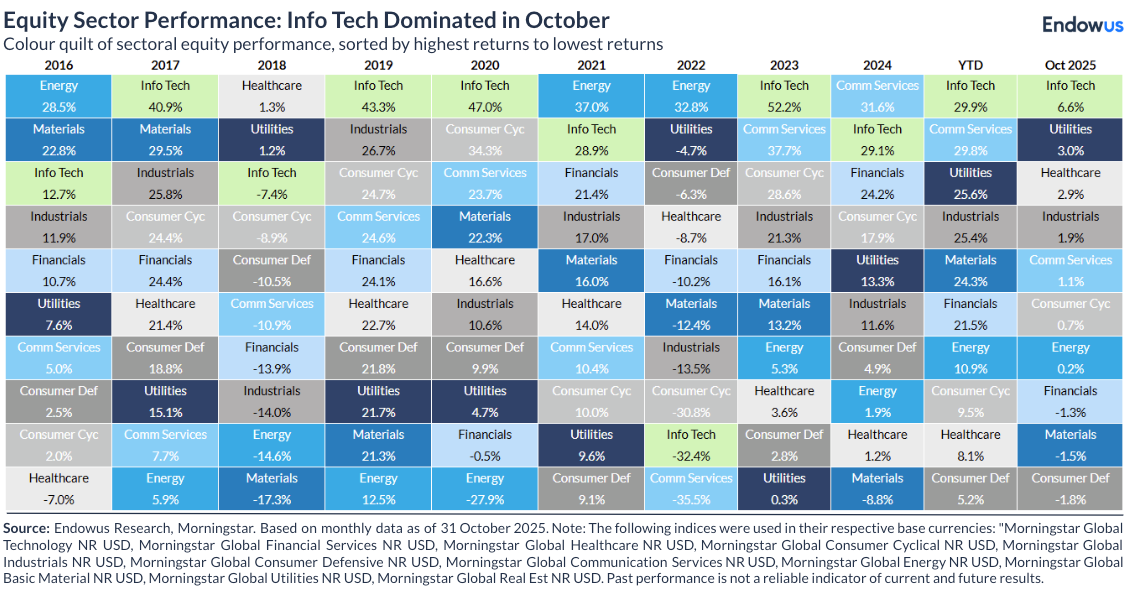

In October, global equities rose 2.2%, thanks to the strength of the technology sector which rose 6.6%. Growth stocks outperformed significantly, gaining 4.2%, while value stocks fell 0.6% for the month. There was a large divergence in sector performance with financials, materials, and consumer defensives in negative territory while tech, utilities, and healthcare posted positive performance.

According to Morningstar, about one third of the year’s valuation increases occurred in October alone, driven by the AI boom with hyperscalers accelerating capex.

Towards the end of the month, however, the markets took a breather due to the concerns over an AI bubble and stretched valuations.

By region, Korea and Japan were the best performing markets, with their October return up 18% and 6%, respectively.

Korea was especially strong, thanks to the dual driver of AI beneficiaries as well as corporate reform. Japan rose on the back of an anticipation of expansionary fiscal and monetary policies by the country’s first female prime minister.

China equities on the other hand, took a breather after strong performance up to September.

On a year-to-date basis, Korea and China are still the best performing regions.

On a sector basis it was all about AI and technology as Info Tech and Communication services retook the crown for best performing sector year-to-date for now three years in a row. Financials, materials and consumer sectors on the other hand struggled to perform. It is interesting to note that Healthcare (and biotech) are starting to perform after a prolonged period of underperformance, while utilities, despite being a defensive sector, is performing well, thanks to strong power demand from AI built-out and application.

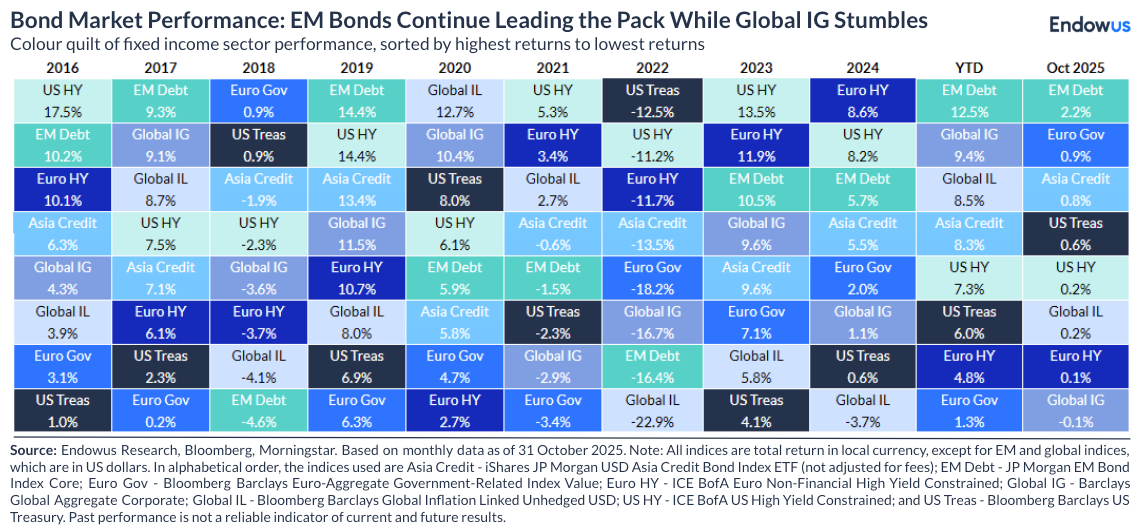

Global fixed income

Fixed income overall delivered positive performance on a hedged basis thanks to lower base rates with 10 year treasury falling 7 basis points (bp) to 4.08% for the month and 2 year treasury falling 3 bps to 3.57%.

The US Federal Reserve cut rates by 25 bps in Oct (following a 25 bp cut in Sep) despite the lack of recent data (ex CPI) due to the government shutdown. The Fed also decided to end “Quantitative Tightening” having reduced its balance sheet by US$2.3 trillion.

The US government shutdown began on 1 October and lasted 43 days, ending on 13 November when the House of Representatives passed a new spending bill that President Trump signed shortly afterward. During the closure, about 670,000 civil servants were furloughed, disrupting essential services and halting economic data collection.

Emerging market debt continued to perform well in October while global government bonds benefited from moderately lower interest rates. Credit spreads widened somewhat in October with investment grade and high yield credit underperforming the global bond market. Overall funds with longer duration and less credit risk did better in October.

Commodities

Commodities were up for the month, though volatility remained evident beneath the surface. Gold saw a sharp intra-month pullback, sliding from above US$4,300 to lows near US$3,886, its strong year-to-date rally. Meanwhile, crude oil extended its sluggish trend, with prices posting their third consecutive monthly decline amid oversupply concerns and rising inventories.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)