.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

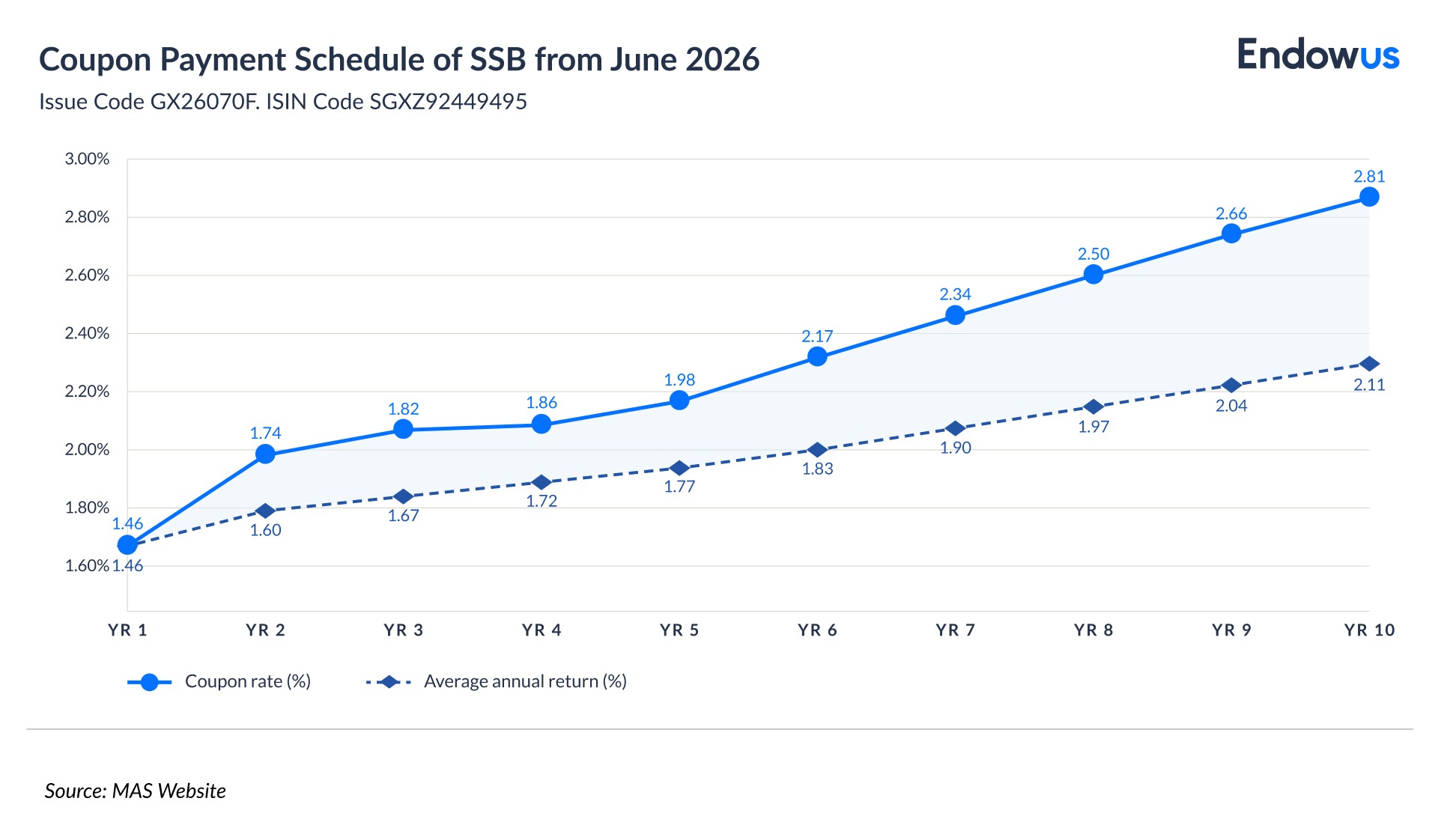

- Singapore Savings Bonds (SSB) are government-backed securities offering step-up interest rates—currently 1.46% in year one rising to an average 2.11% per annum over 10 years for the June 2026 issue—with capital guaranteed by the full faith and credit of the Singaporean government and no penalty for early redemption.

- By law, the government cannot spend SSB proceeds; they are instead deployed into the national reserves framework, managed over the long term alongside Singapore's sovereign wealth, making SSBs a structural tool for domestic debt market development and household financial inclusion.

- SSBs are potentially effective as the capital-stable anchor of a diversified portfolio—pairing them with a growth-oriented investment account may allow investors to earn steady bond income while pursuing long-term wealth accumulation.

The Singapore Savings Bond (SSB) programme was launched in October 2015, as a mechanism to give individual investors access to long-dated government returns with downside protection. The main goal—reinforced by the limited “tickets1” allowed—was to increase financial inclusion and allow Singaporeans to participate in financing government reserves.

The June 2026 tranche (SBJUN26) offers a first-year rate of 1.46%, rising to a 10-year average of 2.11% per annum. Rates have moderated from the cycle highs of 2022–2023—when 10-year averages briefly reached 3.4%—but SSBs remain attractive for investors and savers who prioritise capital protection and predictable income.

This guide explains how SSBs work, how the government structures and uses the issuance programme, what current and historical rates tell us, how to apply step by step, and how to deploy SSBs effectively within a broader portfolio. It also addresses the one question MAS itself is explicit about: what the government does—and does not—do with the money raised.

What are Singapore Savings Bonds?

Singapore Savings Bonds are special-category Singapore Government Securities (SGS) designed specifically for individual investors. They are fully backed by the Singapore government, carry an AAA credit rating from major international agencies, and are issued every month by the Monetary Authority of Singapore (MAS).

Key parameters for 2026:

- Minimum investment: S$500

- Maximum individual holding: S$200,000 across all outstanding SSB issues

- Maximum per application: S$50,000 per issue

- Tenor: up to 10 years; step-up interest structure increases the rate each year

- Interest: paid every six months, credited to your Central Depository (CDP)-linked bank account or SRS account

- Transaction fee: S$2 to apply, S$2 to redeem early

- Eligibility: Singapore citizens, permanent residents, and foreigners aged 18 or above; individual investors only—no corporate accounts

Importantly, SSBs are non-transferable and have no secondary market. You hold them, earn interest, and redeem them if you wish to exit before maturity—at face value plus accrued interest, with no capital loss.

One frequently misunderstood eligibility point: SSBs may be purchased using Supplementary Retirement Scheme (SRS) funds, but not with Central Provident Fund (CPF) monies.

How does the government issue SSBs—and what does it do with the money?

SSBs are issued by MAS on behalf of the Singapore government, typically once per month. MAS sets the issuance size, application window, and allotment mechanics. The programme is governed under the Government Securities (Debt Market and Investment) Act and operates alongside the broader Singapore Government Securities market, which includes SGS bonds and Treasury bills (T-bills).

The proceeds cannot be spent

Under Singapore law, the government is explicitly prohibited from using the proceeds raised from SSB issuances to increase spending. The proceeds feed into the national reserves framework, not operating expenditure.

In practice, SSB proceeds contribute to what the government classifies as public sector surplus monies. These are placed with MAS as government deposits, which in turn have historically supported the accumulation of reserves. Excess reserves are periodically transferred to the government for long-term investment. While the number of total reserves is considered a matter of national security and is thus not publicly disclosed, a prudent assessment puts them in the territory of S$1 trillion.

By borrowing domestically through instruments like SSBs and SGS bonds, the government also withdraws Singapore dollar liquidity from the banking system. That contributes to the structural appreciation pressures on the Singapore dollar that MAS manages as part of its monetary policy framework. The proceeds remain within the reserves ecosystem rather than entering the government's spending accounts.

Why issue SSBs?

The programme serves two complementary purposes. First, it deepens Singapore's domestic debt market by expanding the investor base for government securities beyond institutional participants. Second, it functions as a financial inclusion tool—giving retail investors, including smaller savers who cannot access institutional bond markets, a capital-safe product with returns linked to long-dated SGS yields.

MAS reviews the programme periodically. It has committed to issuing new SSBs every month until at least 2030.

How are Singapore Savings Bond interest rates set?

SSB rates are not set arbitrarily. MAS anchors each tranche's 10-year average return to the average daily Singapore Government Securities benchmark yields—across the one, two, five, and 10-year terms—from the preceding calendar month. This means SSB rates are structurally linked to broader interest rate conditions in Singapore and globally.

A key structural feature: the step-up design rewards patience. An investor who redeems after one year earns the year-one rate only. Holding for the full decade compounds each year's incrementally higher coupon. This mirrors the long-dated SGS yield curve that underpins the calculation.

Rates peaked during the 2022–2023 global rate-hiking cycle. The November 2022 tranche carried a 10-year average of approximately 3.4%—the programme's historical high. Since then, rates have declined as global monetary policy shifted toward easing, settling at the current range.

How to buy Singapore Savings Bonds: a step-by-step guide

Before applying, confirm you have an individual Central Depository (CDP) Securities account with Direct Crediting Service (DCS) activated, and a bank account with DBS/POSB, OCBC, or UOB. Alternatively, SRS investors may apply through their SRS operator bank.

Application window

Each monthly tranche opens for applications on the first business day of the month at 6pm and closes on the fourth-last business day at 9pm. For the June 2026 tranche, the application closed on 25 May 2026.

Step-by-step: cash application via internet banking

- Log in to your internet banking portal (DBS/POSB, OCBC or UOB)

- Choose your preferred issue code.

- Indicate if you are using Cash or SRS funds.

- Enter the amount you wish to invest, in multiples of S$500 (maximum S$50,000 per application).

- Confirm the application. A S$2 transaction fee is charged at this point.

- Allotment results are typically announced on the third-last business day of the month, and the bonds will be issued on the 1st business day of the following month.

Step-by-step: SRS application

- Log in to internet banking of your SRS operator bank.

- Navigate to your SRS account and select 'Invest' → 'Singapore Savings Bonds'.

- Select the tranche and enter your desired amount. Interest on SRS-purchased SSBs is credited to your SRS account.

Redemption

Submit a redemption request through the same banking channel during the redemption window. Proceeds—principal plus accrued interest—are credited to your CDP-linked bank account by the second business day of the following month. There is no penalty for early redemption; you receive accrued interest up to the redemption date. A S$2 transaction fee applies.

Singapore Savings Bond vs fixed deposit vs T-bills vs CPF OA

Each instrument in Singapore's capital-safe landscape serves a different purpose. The comparison below reflects approximate conditions as of mid-2026; rates for fixed deposits and T-bills fluctuate and should be verified at application.

The core trade-off for most investors comparing SSBs against fixed deposits and T-bills is between rate certainty and rate level. SSBs lock in a 10-year step-up schedule at the point of purchase. If market rates subsequently fall—as they have since 2023—holding an older SSB tranche purchased at higher rates becomes advantageous, and vice versa.

What are the benefits of investing in Singapore Savings Bonds?

- Capital guarantee: the Singapore government commits to returning your principal in full.

- Step-up structure: returns increase every year you hold. This rewards long-term savers without locking them in—if your circumstances change, you redeem without penalty.

- Tax-exempt interest income: SSB interest is fully exempt from Singapore income tax for individual investors.

- SRS-eligible: SSBs are accessible via Supplementary Retirement Scheme (SRS) funds, allowing investors to layer government bond returns on top of existing SRS tax relief benefits.

- No market risk: SSBs have no secondary market and no mark-to-market pricing. Unlike SGS bonds or bond funds, their NAV cannot fall.

- Accessible entry point: the S$500 minimum and monthly issuance make it possible to build a position gradually over time.

Risks and considerations

SSBs carry no credit risk and no capital loss risk. They do, however, involve trade-offs that investors should understand before committing funds.

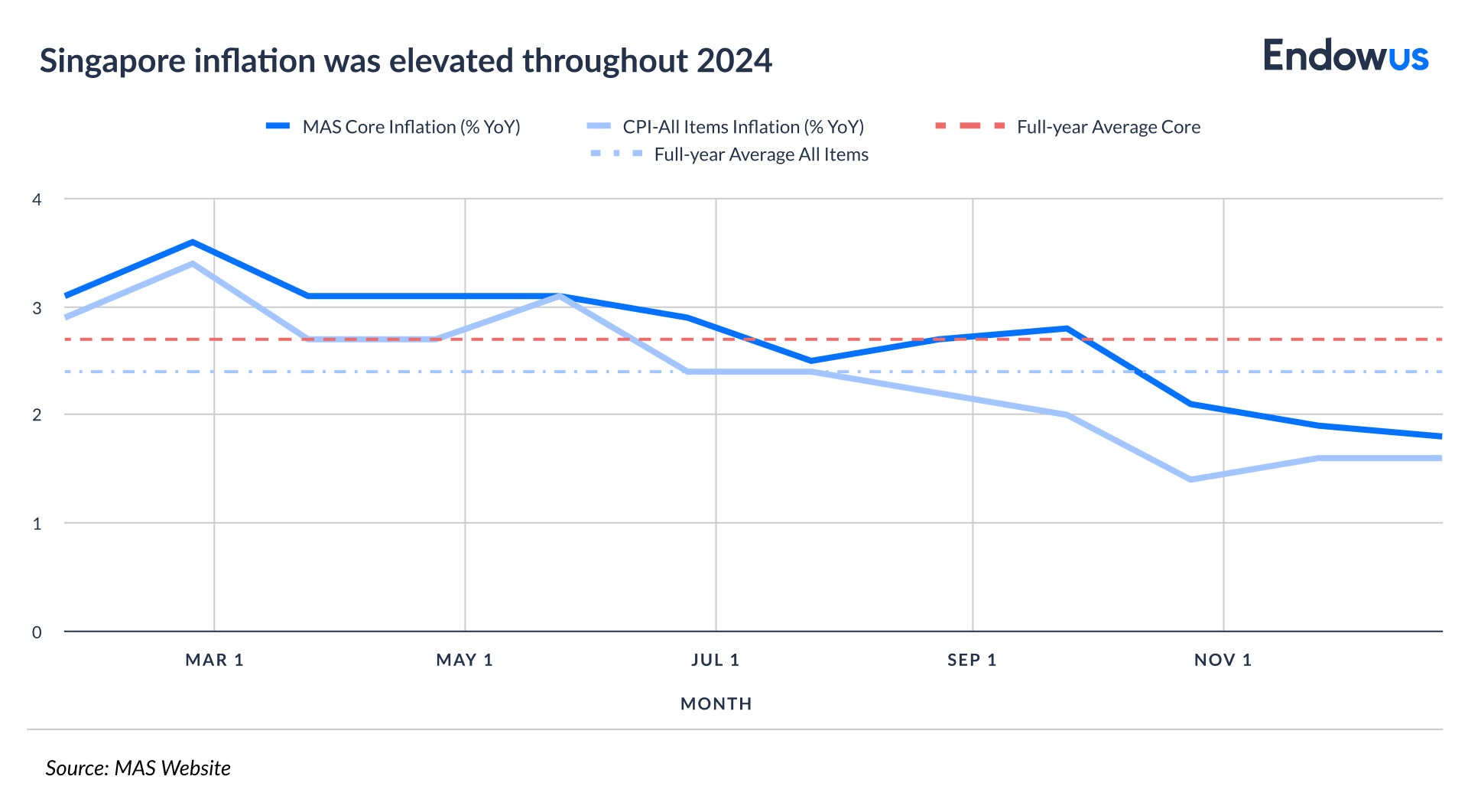

- Opportunity cost: At current rates (~2.11% 10-year average), real returns after inflation may be minimal. While inflation remains subdued, MAS core inflation averaged approximately 2.7% in 2024 (see chart below).

- Rate timing: Investors who purchased SSBs during the 2022 peak rates may be in a more favourable position. Those entering now at 2.11% are locking in a lower long-term return. The step-up structure partially mitigates this—later years earn more—but the compounded 10-year average reflects the prevailing SGS yield curve at the time of application.

- Liquidity lag: Redemption takes until the second business day of the following month. SSBs are not a substitute for an immediately accessible emergency fund.

- S$200,000 cap: The per-individual holding limit may constrain SSB's role for higher-net-worth investors seeking to deploy larger capital-safe allocations.

- No secondary market: You cannot sell your SSB to another investor; you can only redeem it back to the government. This is by design, but means SSBs cannot be used as collateral and cannot be sold at a premium when rates fall—the gain accrues as above-market income over the remaining tenor rather than as a realisable capital gain.

Investment implications: where SSBs fit in a portfolio

In our view, SSBs are best understood as the capital-stable anchor of a conservative allocation—not as a standalone investment strategy. The 2.11% current 10-year average available in June 2026 is unlikely to compound wealth meaningfully over a decade; it is a return for investors who need certainty, not growth.

Three potential deployment cases stand out:

- Medium-term cash reserves: Investors with a three-to-10-year time horizon who want to hold cash productively—earmarked for a property purchase, education funding, or retirement income—can use SSBs to generate predictable returns while retaining the option to redeem with one month's notice if plans change.

- SRS tax optimisation: SRS investors approaching the S$15,300 annual contribution ceiling face a portfolio construction question: where to deploy the balance between equity funds and capital-safe instruments. SSBs, eligible for SRS and tax-exempt on interest, offer a clean combination.

- Complement to growth portfolios: A portfolio holding globally diversified equity funds through Endowus can use SSBs as the stabilising component—a capital-safe buffer that limits portfolio drawdown without sacrificing long-term return potential from the equity allocation.

While Endowus portfolios are not backed by the full faith and credit of the Singaporean government, and returns are not guaranteed, they can potentially complement a low-volatility SSB allocation. For investors looking for daily liquidity, Endowus offers the Endowus Cash Smart suite, while the Endowus Flagship Portfolio is available for the long-term growth tier.

Frequently asked questions about SSBs

What is the current SSB interest rate?

The June 2026 SSB (SBJUN26) offered 1.46% in year one, rising to a 10-year average of 2.11% per annum. Rates are announced monthly by MAS and track the preceding month's Singapore Government Securities benchmark yields.

How do I buy a Singapore Savings Bond?

You need an individual CDP account and a bank account with DBS/POSB, OCBC, or UOB—or an SRS account if you are buying with SRS funds. Apply via internet banking or ATM during the monthly application window (opens the 1st business day, closes the 4th-last business day of the month). Each application carries a S$2 transaction fee.

Can I use CPF to buy SSBs?

No. SSBs may not be purchased using CPF funds. You may, however, invest in SSBs through your Supplementary Retirement Scheme (SRS) account.

Is SSB interest taxable?

No. Interest income from Singapore Savings Bonds is fully exempt from Singapore income tax for individual investors—an advantage over fixed deposits and T-bills, whose interest is taxable.

What happens if the SSB is oversubscribed?

Each applicant receives at minimum S$500. Allotment proceeds in S$500 increments until either the applicant's full amount is fulfilled or all bonds are allocated. In recent tranches (2024–2026), most issues have been under-subscribed, meaning full allotment is likely.

1In financial jargon, a “ticket” is the size of an allocation.

Do Crazy Rich Asians only invest in real estate?

Change is the only constant in life: Are index funds truly "passive"?

The real difference between unit trusts and ETFs

%20F1(2).webp)

.webp)

.webp)