.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

The ability to control our emotional impulses and view situations from multiple perspectives are among the most valuable life skills we can develop. They shape how we navigate uncertainty, respond to change and tackle the challenges that contribute to our personal growth.

Life and money have plenty in common—they are both complex, unpredictable and at times, simply a pain to deal with. We may not be able to change the systems that influence them, but personal growth gives us the wisdom and emotional fortitude to change the way we approach them.

Using five simple sketches, we apply the lessons of personal growth to managing money and illustrate how small actions and shifts in perspectives can help you become better at growing your wealth.

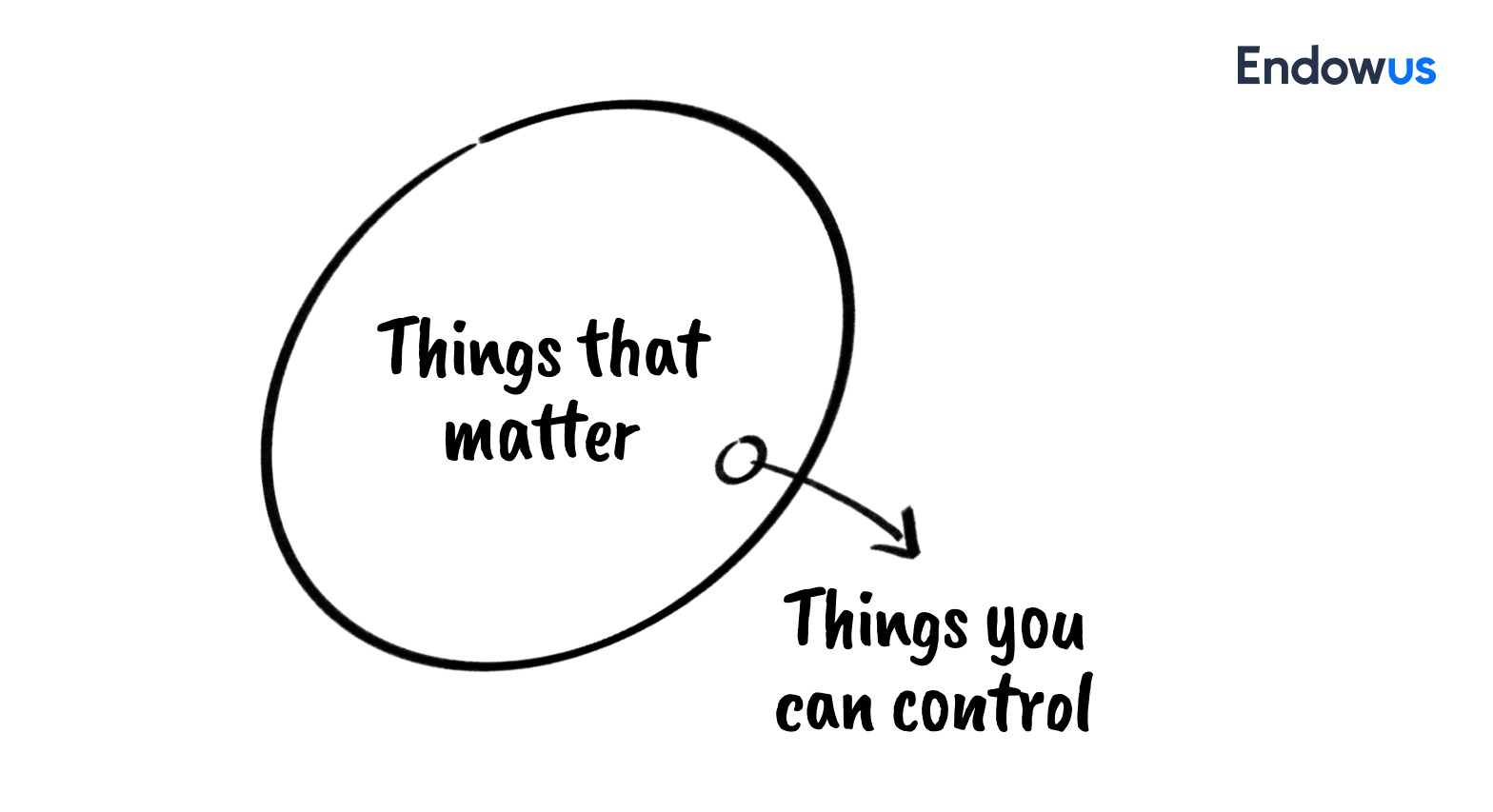

1. Things that matter vs. things you can control

The vast, outer space represents the more complex forces of things that matter. They may be the opinions of others, global events and the economy, historical events, and luck that influence our circumstances. The irony is this: Most people obsessively try to grip and manage the outer circle and mistake influence for control.

What we should do is to accept the vastness of the external world, but focus 100% of our energies on the small, sovereign circle where we are in full control. It represents our efforts, reactions, habits and integrity— the only assets we truly own and can improve on. While small, they tend to have ripple effects on how we deal with uncertainties.

Applying this to investing, the market matters, but what happens in the market is often out of our control. Rather than hoping for the market to move in your favour, focus on how you can better manage your money to generate better outcomes.

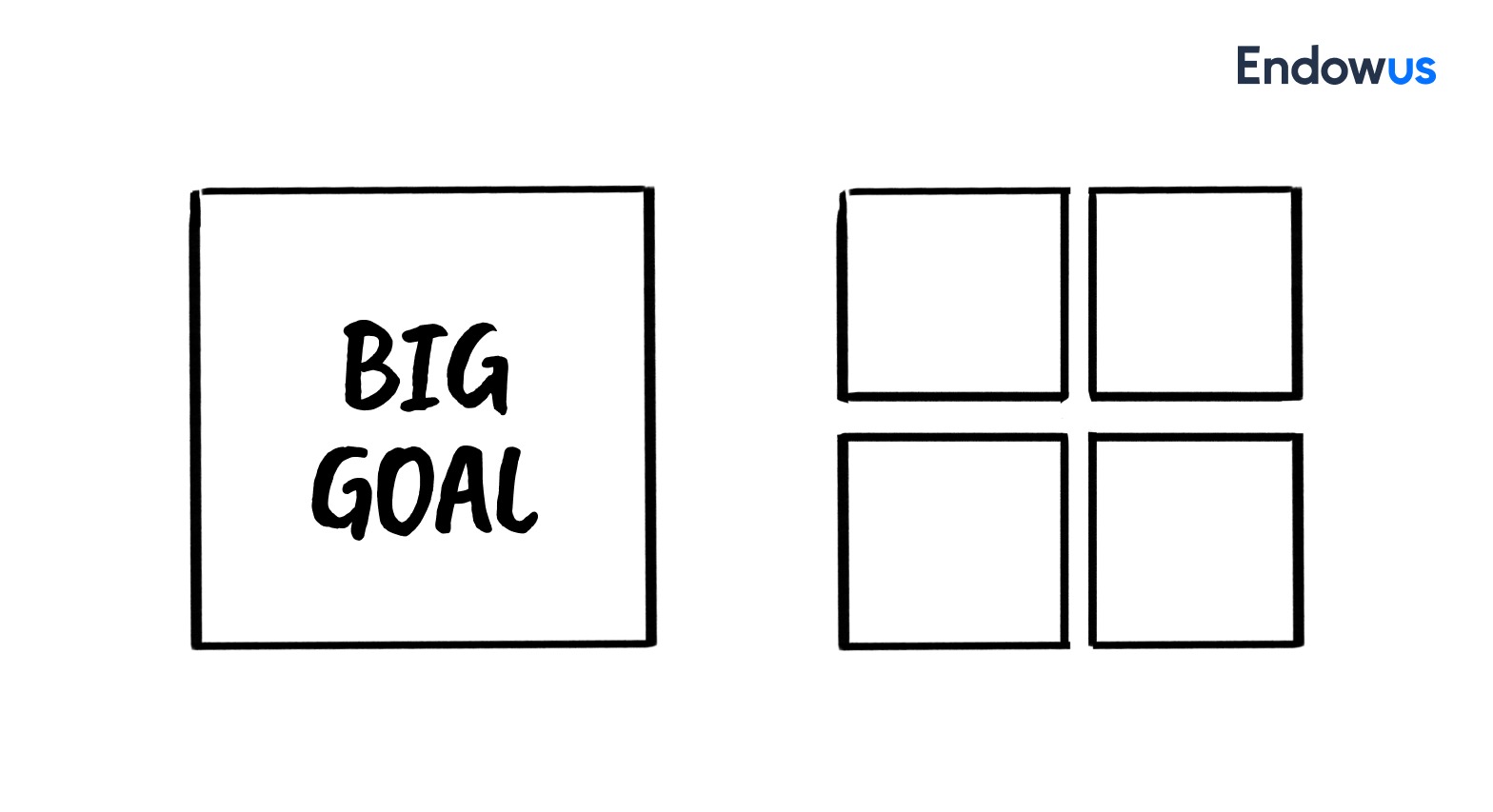

2. Break down your “get rich” goal into smaller steps

More often than not, we dream of lofty goals like getting rich, but they are usually too abstract to act on. When the goal is vague, so is the plan—this is how we get stuck in inertia, and progress stalls.

The reality of wealth isn’t a single, spectacular event; it’s a range of small actions. Break the single, overwhelming number into a series of achievable, short-term milestones.

You can do the same with investing. Say, you aim to be a millionaire at retirement. Create a plan with reasonable milestones, such as accumulating your first S$100,000 at 30, so that you can fairly assess your progress and hold yourself accountable to the plan. It may come in the form of a dollar-cost averaging approach, where you invest a certain amount of money every month and allow it to grow and compound towards your final goal.

Read more: How to get rich in Singapore

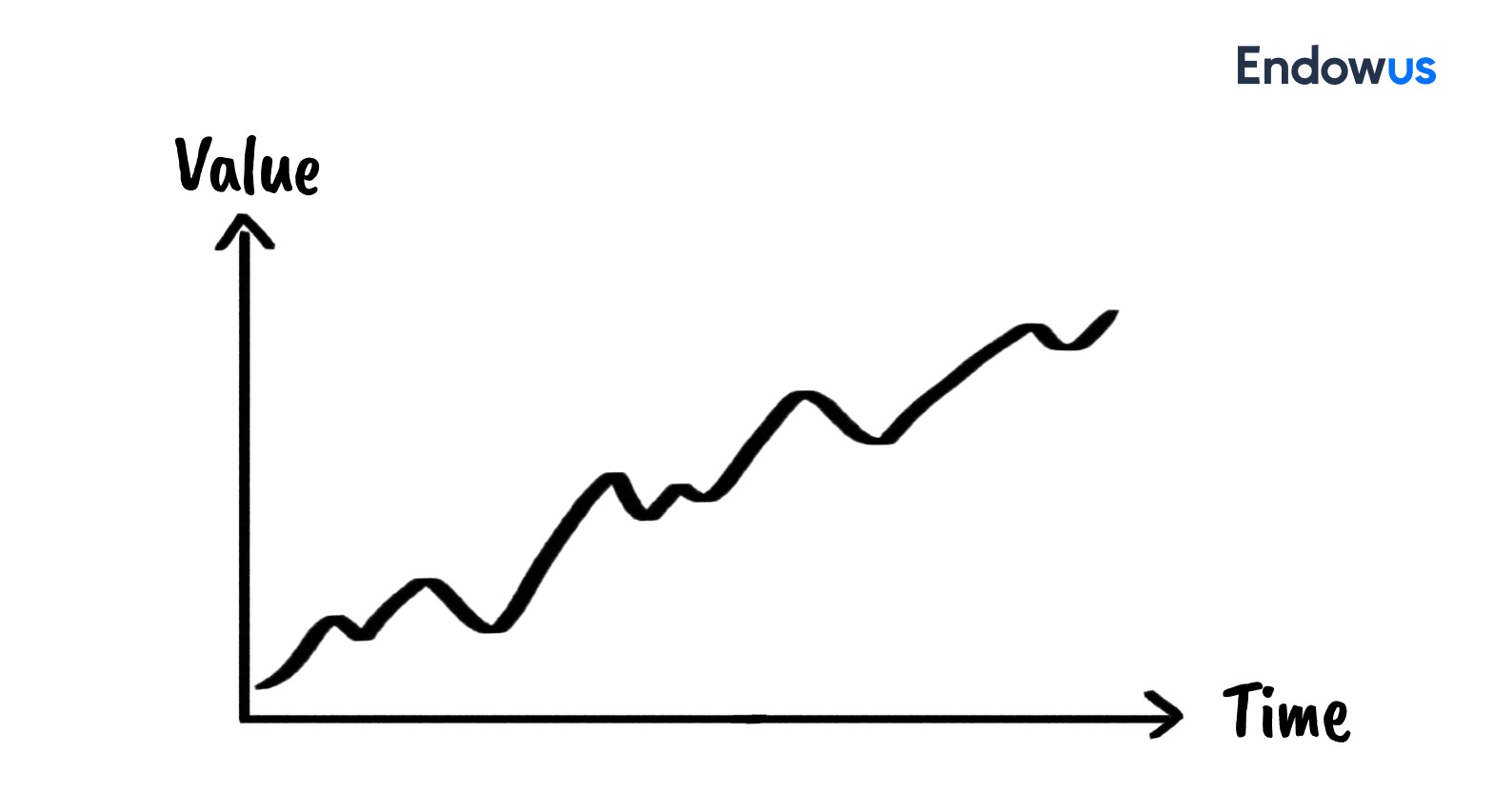

3. Personal growth and the markets have more in common than you think

Personal growth and financial markets share a profound, underlying rhythm. Both are defined by a continuous cycle of volatility, risk, and the eventual potential for significant return.

Relationships, knowledge, and health all take time and effort to nurture, and it is the same for investing. There will be good and bad times, and it is especially the setbacks, failures, and doubts that will test your resolve.

The key to success is long-term strategy and emotional discipline. Instead of chasing quick wins, looking at the bigger picture: are your decisions effectively contributing to your long-term growth, personally and financially?

Ultimately, both the market and the self thrive on patience, adaptation and resilience. Growth is never linear, but small, consistent daily efforts (saving or studying) eventually accumulate into massive, life-altering gains. Being able to withstand temporary ups and downs will pay off in the long run..

4. Mind the gap: What you get vs What’s given

Investors seeking the best outcomes should pay close attention to what’s eating into returns: emotions that cloud judgement, and fees that hide within fine print.

What markets give you is the raw, objective performance of an index or fund—what the investment could have delivered if held perfectly. What you get is the actual growth realised in your portfolio. The space between them is the gap where wealth dissipates.

The shortfall is primarily made up of behavioural costs and actual expenses.

- Mistimed transactions are the most significant factor. Driven by fear during market downturns and greed during rallies, investors often buy high and sell low. This poor market timing results in missing the most powerful upswings and locking in losses.

- Funds with higher return volatility tend to have wider gaps – the dramatic swings act as a trigger, prompting investors to transact more frequently and emotionally.

- Expense ratios, commissions, and hidden costs are subtracted directly from the total return before it reaches the investor. While a smaller component than behaviour, minimising costs is one of the easiest ways to ensure more of the Market Return is captured.

The market is a patient machine designed for long-term growth. The only way to close this gap is to minimise your own interference and the fees you pay: set a plan, automate your contributions, and trust the process.

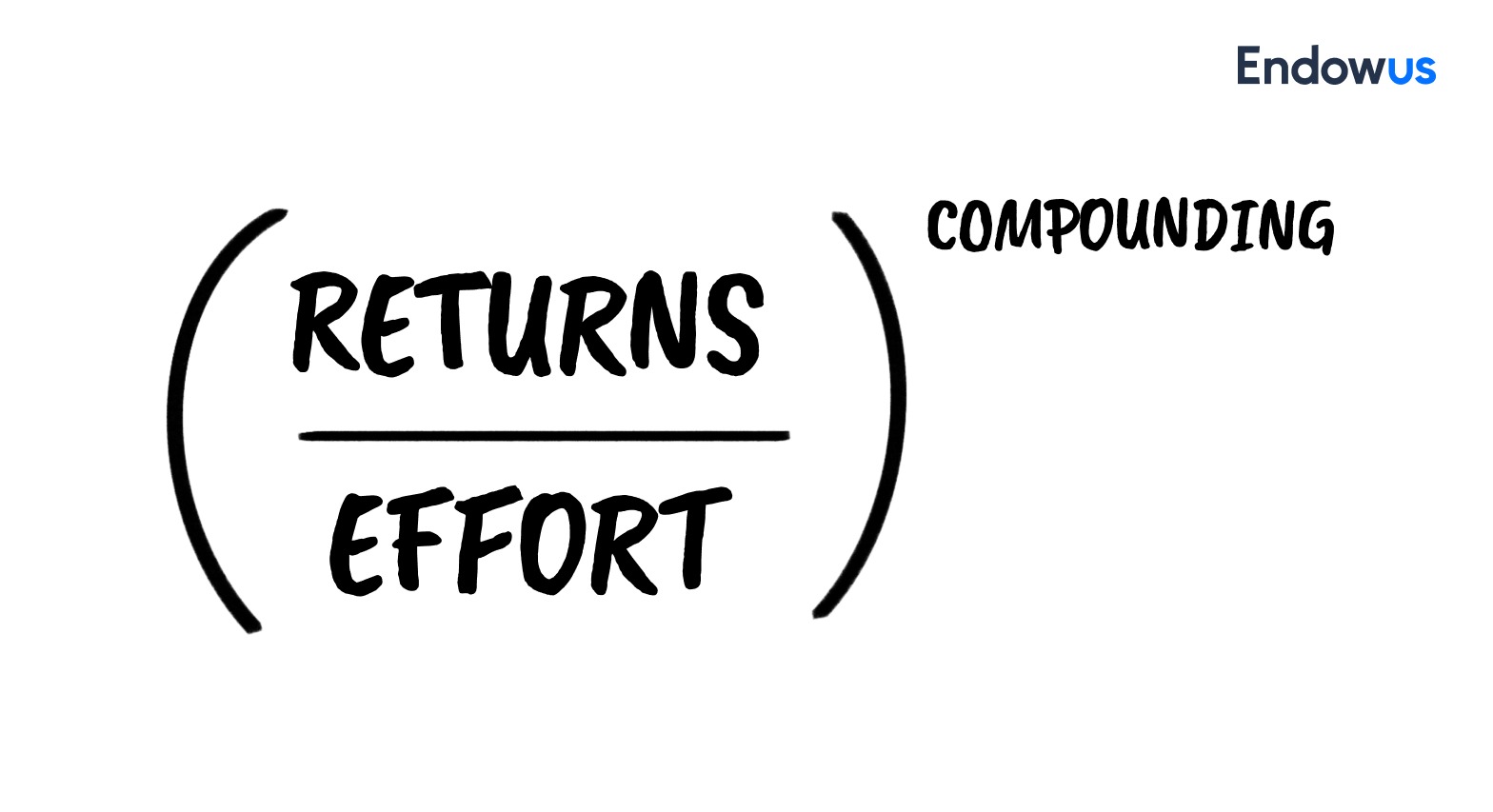

5. Revisiting the formula of wealth

In the last sketch, we want to challenge a core belief in achievement: that maximum effort equals maximum return and re-examine the true function of effort in building wealth.

The pitfall of that belief is the cost of hyper-effort—the time and mental energy spent trying to generate an extra few basis points are often subject to diminished marginal utility, and in investing, introduce unnecessary risk.

After achieving the efficient frontier, that time spent can be more valuable when invested in career growth, health, or relationships—assets that yield lasting, non-financial returns.

People also often overlook the power of compounding. Compounding is time-dependent, and does not scale with activity level. Excessive effort (frequent transactions) often interrupts the compounding process by reducing the capital base or forcing premature withdrawals.

The smartest effort is not the most effort, but the most targeted effort. It should be to apply just enough effort to set up the initial conditions (secure the base, automate the savings, lower the fees) and then step back to let time and compounding take the lead.

Sometimes, the simplest path to a larger outcome is putting a cap to activity—staying invested, staying consistent, and letting exponential growth work its magic undisturbed.

Take actions

The path to mastering your personal growth and the path to financial security are one and the same—both demand execution over endless deliberation.

The action you can take right now is to identify the biggest drag on your growth—either a behavioural flaw (fear-based trading, procrastination) or a structural flaw (high fees, vague goals)—and commit to eliminating it today. Then, turn the insight into immediate, zero-effort action, and they can be:

- The small circle: Identify one major source of anxiety outside your control (e.g., the daily market news) and commit to ignoring it for one week. Focus that freed-up energy entirely on refining one small, controllable habit.

- Automation: Go set up an automated monthly contribution to your diversified portfolio. This act permanently minimises the Effort divisor in your wealth equation and removes the opportunity for emotional interference.

The most efficient way to apply these principles is by simplifying your investing life. The market rewards discipline and consistency, not over-activity. Close the loop between insight and action: Endowus makes it simple to set up your disciplined foundation. Start your compounding system today.

How to start managing and investing your money (#adulting)

.png)

Are gambling and investing similar?

.png)

Goal-based investing and why it matters

%20F1(2).webp)

.webp)

.webp)