.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

July continued to be a strong month for risk assets, particularly equities, as the Morningstar Global Markets Index rose 3.2% for the month on an SGD basis. The underperformance of the USD against SGD reversed in July, as the greenback appreciated by about 2.1% against SGD. This helps the performance of USD-denominated assets when translated into SGD.

July continues to be risk on

The Magnificent 7 stocks—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla—drove performance on the back of strong earnings, with growth equity outperforming value equity.

Trade resolutions between the US and Japan and between the US and the EU were reasons why markets continued to be “risk-on”. We saw signs of exuberance, however, as lower quality growth names and companies with high short interest (i.e. those that hedge funds are fundamentally short) outperformed.

While uncertainties around tariffs continue, we noticed an interesting development around the earnings of US companies.

According to Goldman Sachs, 56% of companies in the S&P 500 Index that have reported second quarter earnings have revised up their earnings guidance for 2025, noting that companies are navigating tariff uncertainties better than expected through supply chain management, increasing prices, and cutting other costs. We believe a more resilient earnings outlook compared to previous expectations may be another reason we are seeing stronger equity markets.

Fixed income, on the other hand, had a tougher time as interest rates moved higher in July (10-year Treasury yields rose by 15 bps to 4.374%) amid a hawkish Fed and continued resilience in economic data. Moreover, the correlation between the USD and yields returned to positive. In early August, a much weaker July payroll data and downward revisions to May and June turned the narrative quickly to further rate cuts, bringing interest rates down again.

What’s next?

The market narrative continues to oscillate, and future predictions continue to be very difficult to make. Going through the volatility in April and subsequent rally, which continued in July, we have witnessed how important it is to have “time in” the markets rather than “timing” the markets. Diversification by asset class, region, and sector continues to remain key.

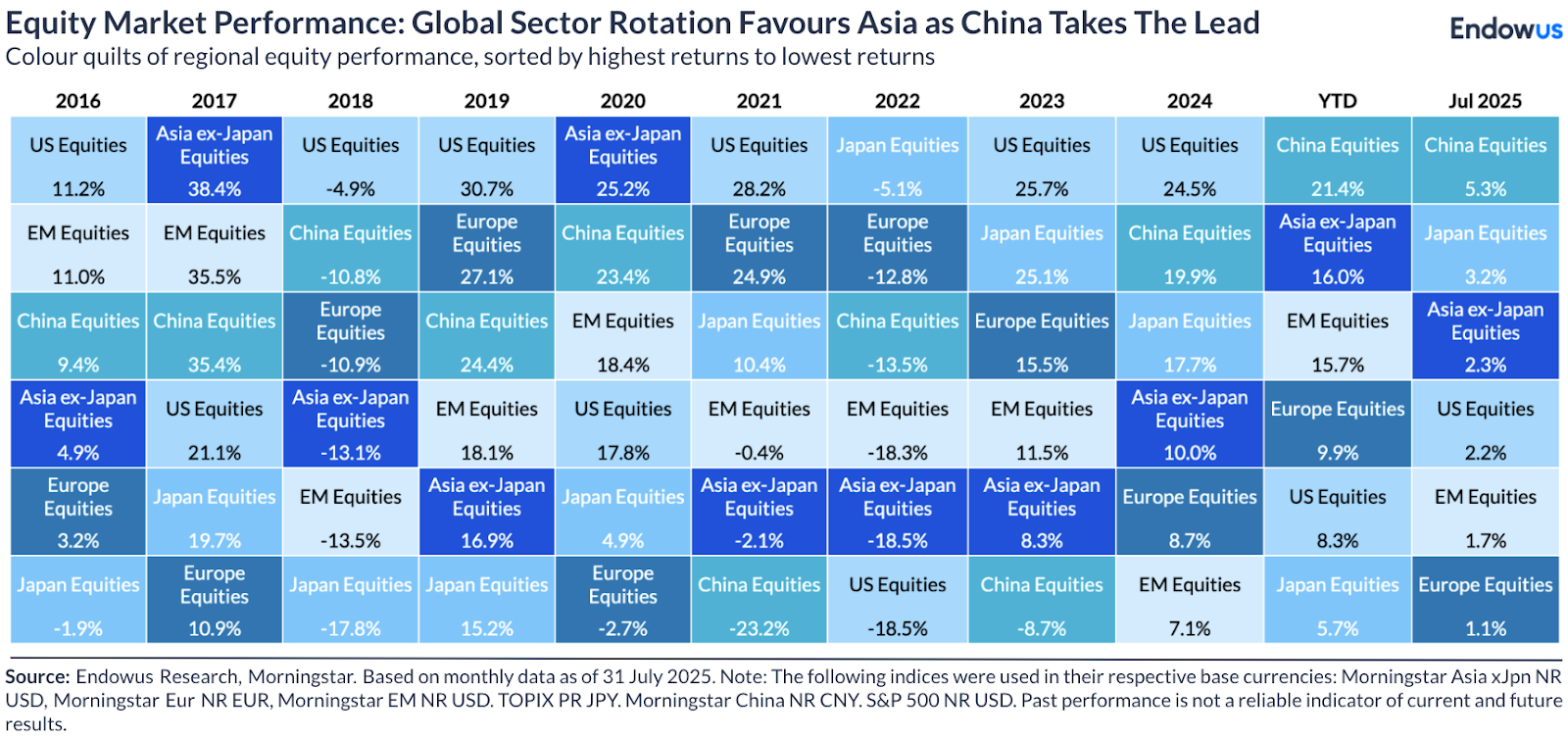

Global equity

China was the best performing region year-to-date as well as for equities in July. That being said, China’s performance in July has diversified away from information technology, which was the main contributor to performance in the first half of 2025. It was the healthcare, insurance, and communication services sectors that outperformed in the offshore market, and materials and telco that outperformed in the onshore market.

Asian markets overall continue to provide considerable diversification benefits away from the US markets as we see liquid markets like China, Japan, & Korea put up strong performance.

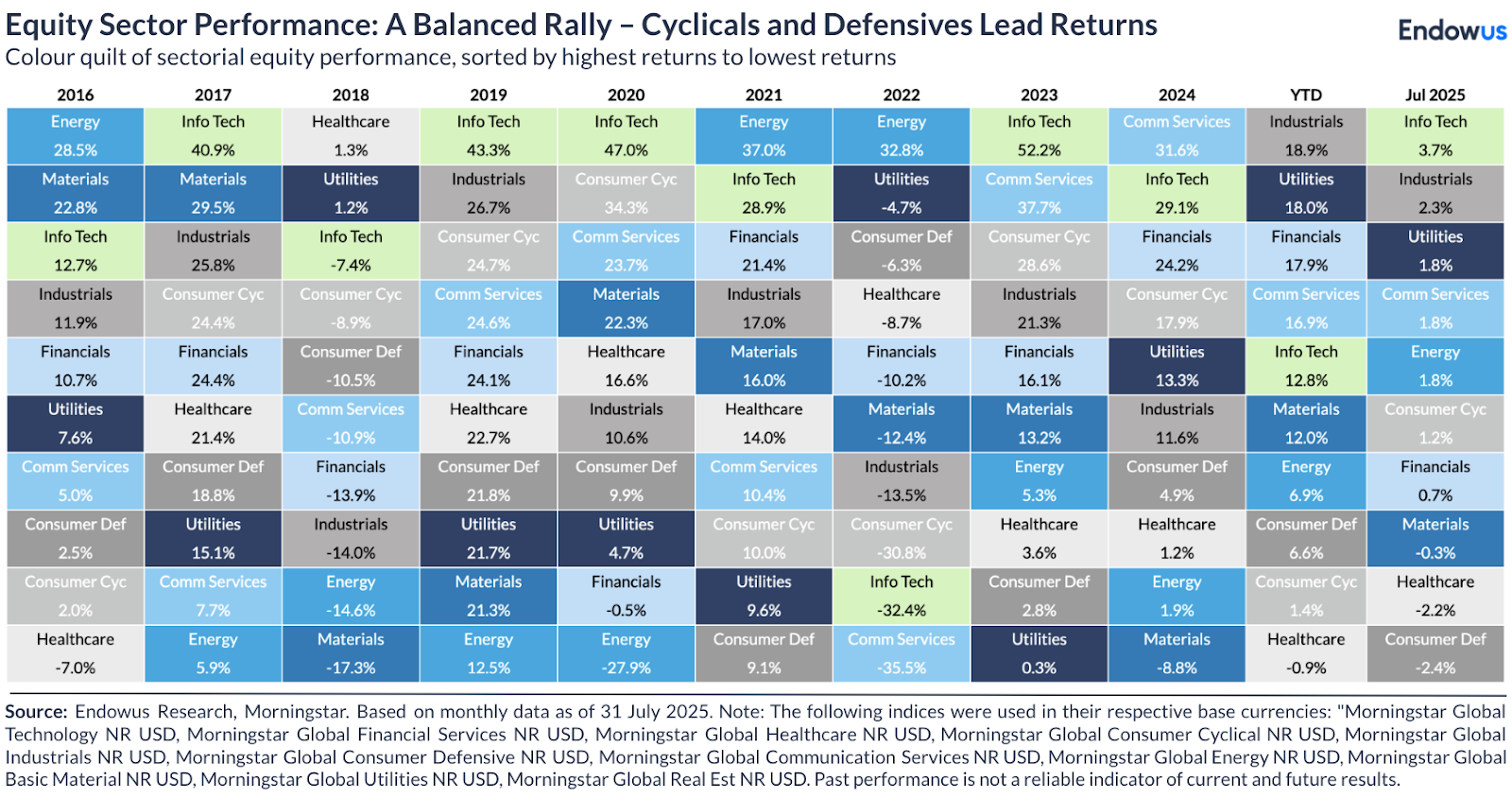

By sector, technology was the winner in July, continuing its recovery from its lows in early April as the AI theme, which has been propelling growth and earnings, continues to perform in the sector.

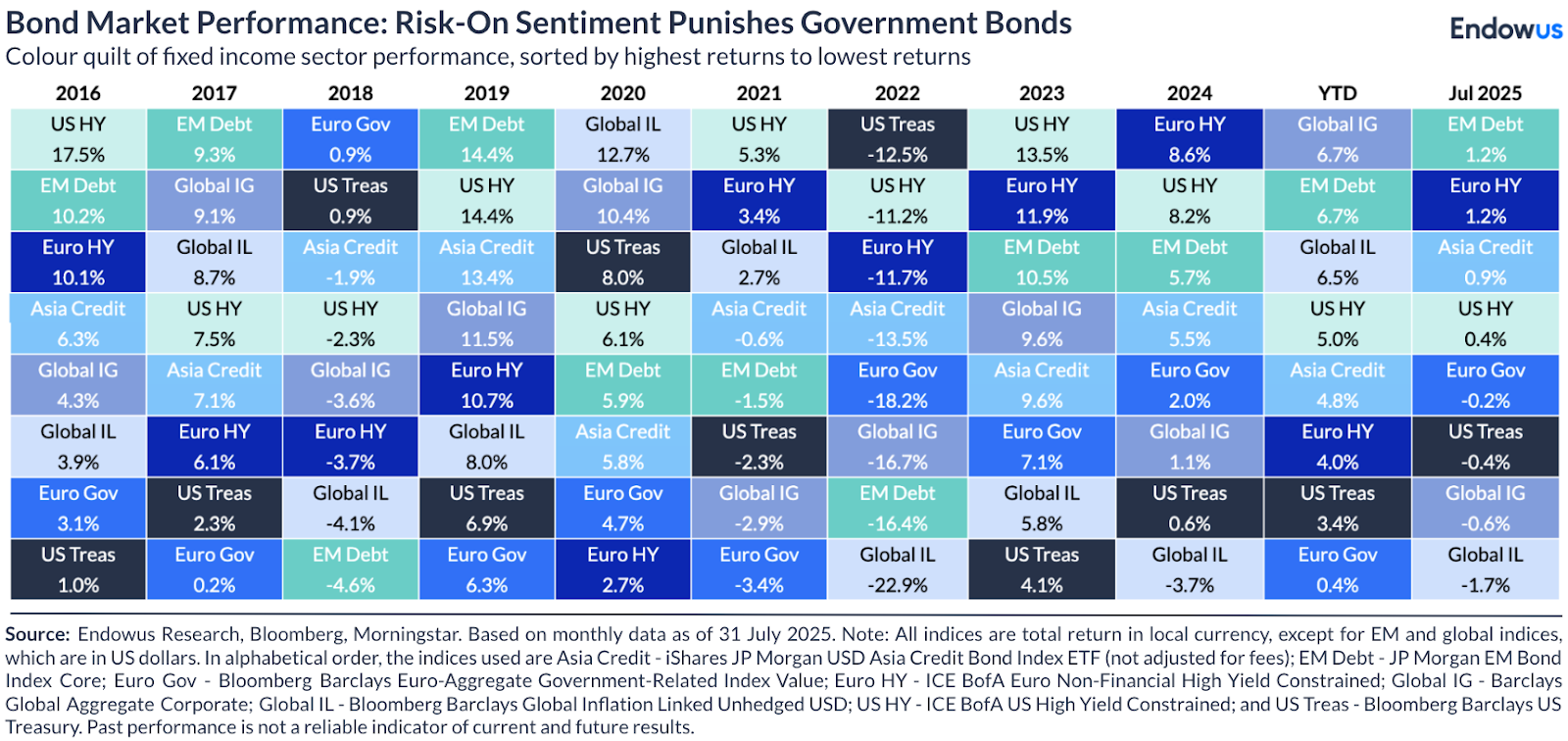

Global fixed income

In July, emerging market debt and euro high yield were the best performing sectors as high quality developed market fixed income struggled to perform amid higher interest rates. However, on a YTD basis, the overall fixed income segment has contributed to lowering the equity volatility and providing a steady return coming from its high starting base yield.

Similar to equities, we have seen emerging market debt provide diversification benefits from developed market debt (on rates, spread and currency basis) YTD, and thus the philosophy of regional diversification also applies to fixed income.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)