.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

The Endowus Investment Office reviews the payout targets regularly. For the latest payout targets, please refer to the Income Portfolios product page.

This article is updated as of Sep 2025, and the original article was first published in Dec 2021 at the launch of the Income Portfolios.

Income investing has been an evergreen theme in Asia, and Singapore is no exception. In our investor survey in 2025, 49% of respondents in Singapore expressed that generating alternative income streams is one of the top objectives with their investments. This is consistent with high demand for income-focused funds and products, with a clear preference for regular payouts.

With the perennial demand for income, there have been many income funds offered in the market. In addition, annuity, endowment and insurance-linked products from insurance companies are among the common tools to produce income, but investors are gradually wary of the subpar historical returns given the embedded high fees.

Your demand, we listen

Given the market backdrop, the idea of constructing an income portfolio at Endowus came to fruition following a client survey. In 2021, we found out through a survey a nearly unanimous demand of an income-distributing portfolio.

At Endowus, our approach to investing has been one that mirrors the institutional investor approach, which is advised on a multi-manager and multi-fund model. This is also how we think an income portfolio should be constructed – with diversified sources of income from funds managed by the best accessible portfolio managers.

As a result, the series of three Income Portfolios – Stable, Higher, and Future, was launched targeting investors at various life stages, with differing needs and unique financial circumstances.

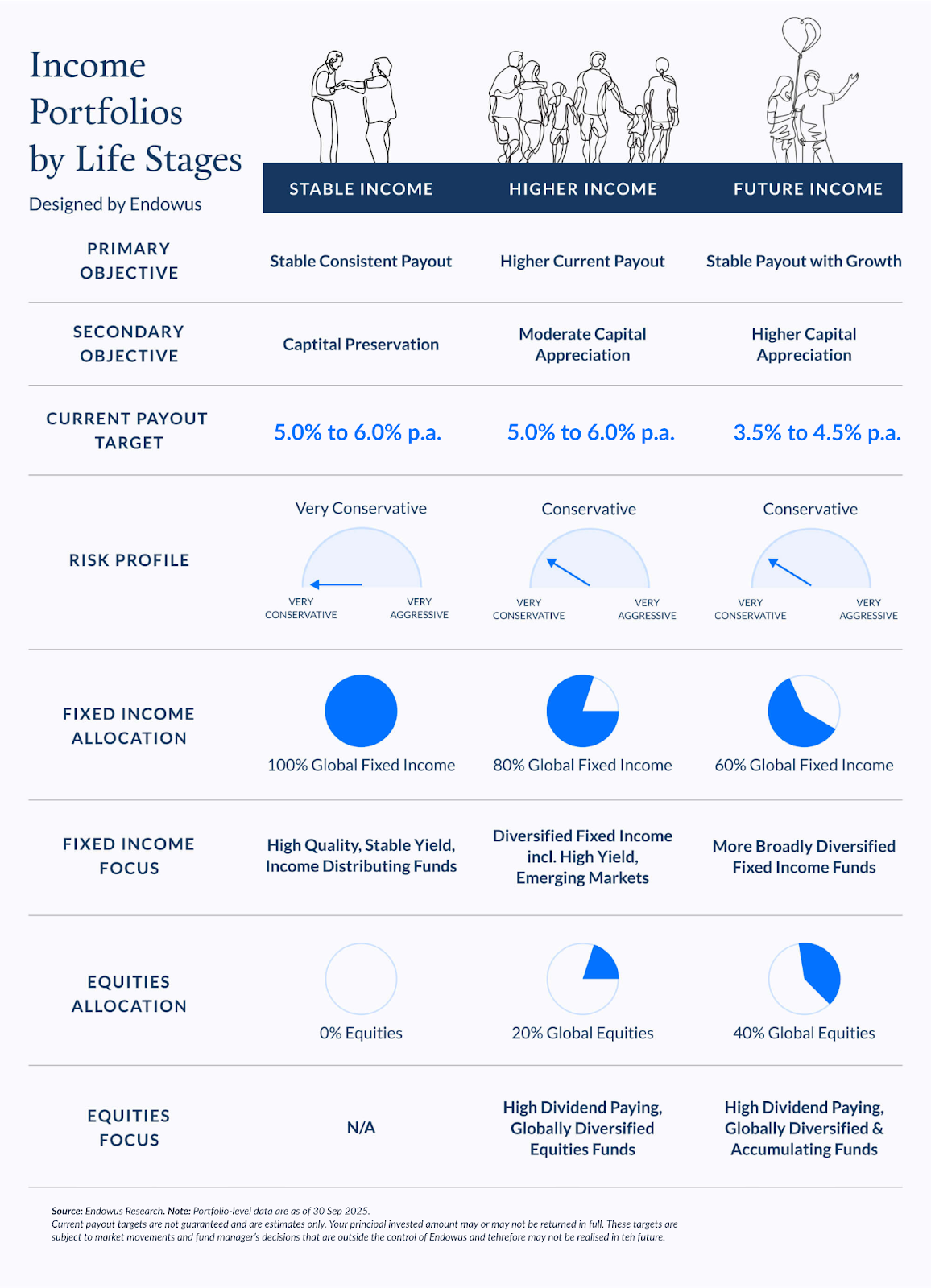

Stable, Higher, and Future Income: How to choose

How are risk levels set in Endowus Income Portfolios?

Risk levels across the Endowus Income Portfolios are primarily determined by:

- Asset allocation: The proportion of fixed income versus equities in each portfolio.

- Underlying fund selection: Choosing appropriate funds—such as high yield or high-quality fixed income funds—within the asset allocation to meet specific income and growth objectives.

This dual-layered approach allows the Endowus Investment Office to tailor each portfolio’s risk-return profile to suit different investor needs and life stages.

All three Income Portfolios are anchored by a dominant allocation to fixed income, but the degree and type of exposure vary. This variation in fixed income exposure directly influences the risk profile and payout characteristics of each portfolio.

How do payout targets and capital appreciation potential differ?

Asset allocation and risk parameters directly influence both the current payout target and the potential for capital appreciation. Each portfolio is designed to meet specific investor needs across the risk-return spectrum:

<divider><divider>

Stable Income Portfolio

Current payout target: 5.0% to 6.0% p.a.

- This is a 100% fixed income solution, with a shorter duration but higher credit risk than the Core Flagship Fixed Income Portfolio. It offers higher expected returns than Cash Smart solutions, which focus on capital preservation with minimal risk.

- Stable Income prioritises a stable and consistent payout, while minimising risk to preserve capital. With limited upside, its primary objective is capital preservation.

<divider><divider>

Higher Income Portfolio

Current payout target: 5.0% to 6.0% p.a.

- Higher Income invests in higher-risk fixed income assets—including high-yield, emerging market, and Asian bonds—that offer enhanced payouts in exchange for greater volatility.

- Additionally, it allocates 20% to global equities, primarily high-dividend funds and real assets, which have historically exhibited lower volatility than traditional core equities.

- Designed to maximise payout at an optimal risk-adjusted level, this portfolio balances higher yield with moderate volatility, striking a balance between income and growth.

Portfolio update in September 2025

In Sep 2025, the current target payout of the Higher Income Portfolio is adjusted to 5.0 - 6.0%, from 5.5 - 6.5% to reflect a recent increase in hedging cost between SGD and USD pair, which has caused certain fund managers to lower the payout, impacting the overall payout levels across all three income portfolios.

This in particular has caused Higher Income Portfolio’s payout yield to dip below the existing target payout range. In light of the prevailing interest rate cycle, it is only prudent to lower the current target payout range of the Higher Income Portfolio.

Investment grade flexible income funds continue to be able to generate income that’s akin to high yield funds in the current environment, where high yield spread is particularly tight. In light of this, we are comfortable with the Higher Income Portfolio generating an income level that is similar to that of Stable Income.

It is important to note that the Higher Income Portfolio has delivered better growth in terms of total return than Stable Income, with prudent addition of credit and equity risk. This means that after receiving the income, investors in the Higher Income Portfolio would have seen a stronger increase in their capital year-to-date.

Our Investment Office is monitoring and will take actions to improve the Portfolios, if we believe there are better building blocks or is room to optimise the Portfolios further.

<divider><divider>

Future Income Portfolio

Current payout target: 3.5% to 4.5% p.a.

- Built for long-term compounding growth, Future Income features greater equity exposure, enabling the potential for capital appreciation over time.

- It includes high-dividend stocks, real assets, and globally diversified equities through the Dimensional World Equity Fund, which systematically tilts toward value-oriented, profitable, and smaller companies—offering broader diversification than traditional market-cap weighted indices.

- Like Higher Income, it also includes selective exposure to higher-risk fixed income assets, such as high-yield, emerging market, and Asian bonds. This portfolio is best suited for investors seeking wealth accumulation and growing future income.

<divider><divider>

What makes Income Portfolios different?

When building the Portfolios, several salient points were taken to heart from our clients and designed and optimised through quantitative and qualitative due diligence and screening performed by the Endowus Investment Office. Here are what clients expect our Investment Office to deliver:

- An independent, multi-manager, Best-in-Class income solution that is designed by the Endowus Investment Office.

- A portfolio that will meet the different needs of clients at different life stages, cash flow needs, and risk appetite.

- An Investment Office to actively monitor and update the portfolios, sometimes recommending portfolio changes appropriate to either improve risk-adjusted returns or lower costs in a meaningful way. This leaves them to get on with life as they invest passively and seamlessly on the Endowus online platform, always knowing it is advised, managed and with the lowest negotiated costs possible.

Who are the Endowus Income Portfolios for?

Our survey revealed three distinct groups, shaped largely by age and family structure:

- Stable Income – For older investors, nearing or in retirement, prioritise capital preservation and seek a stable, passive income stream from their accumulated savings.

- Higher Income – For the sandwich generation, juggling family expenses and mortgages, needs higher income now while still growing their capital for the future.

- Future Income – For younger investors aim to build wealth early, supplement regular expenses with passive income, and grow their savings for higher future payouts.

Income Portfolios are tailored for every investor who wants regular payouts while still growing their wealth. The above life-stage personas are some of the use cases. Each portfolio offers a clear breakdown of:

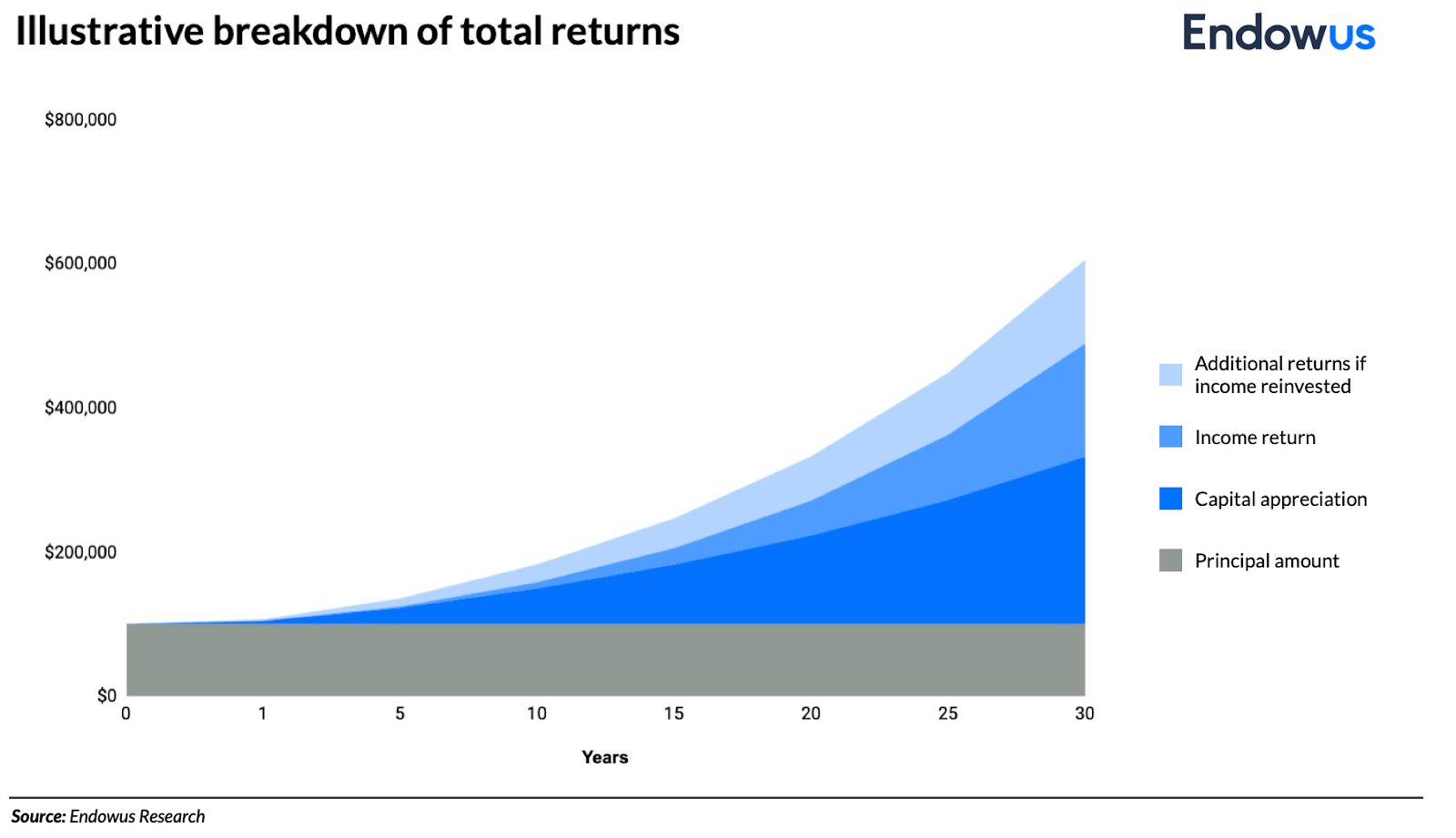

- Current payout target: The estimated monthly income you receive.

- Capital appreciation: The potential long-term growth of your invested capital.

Together, these form the total return of Endowus Income Portfolios. Payouts are typically monthly and fixed by percentage or dollar value. While actual amounts may vary, with payout targets set by underlying fund managers, we aim to provide a reliable estimate.

Although market fluctuations can cause double-digit drawdowns, the key focus of Income Portfolios is maintaining a steady payout. That consistency matters more than short-term changes in portfolio value.

Note: The Endowus Investment Office reviews payout targets regularly. For the latest figures, visit the Income Portfolios product page.

In the meantime, the Endowus Core Portfolios—Flagship, ESG, and Factor—are designed for long-term wealth accumulation. They’re broadly diversified, low-cost, and built on passive, strategic asset allocation. These portfolios are non-distributive, meaning dividends and payouts are automatically reinvested to compound returns over time. If you don’t need regular income, staying invested in Core Portfolios is ideal.

Income Portfolios custom-built with global fund managers

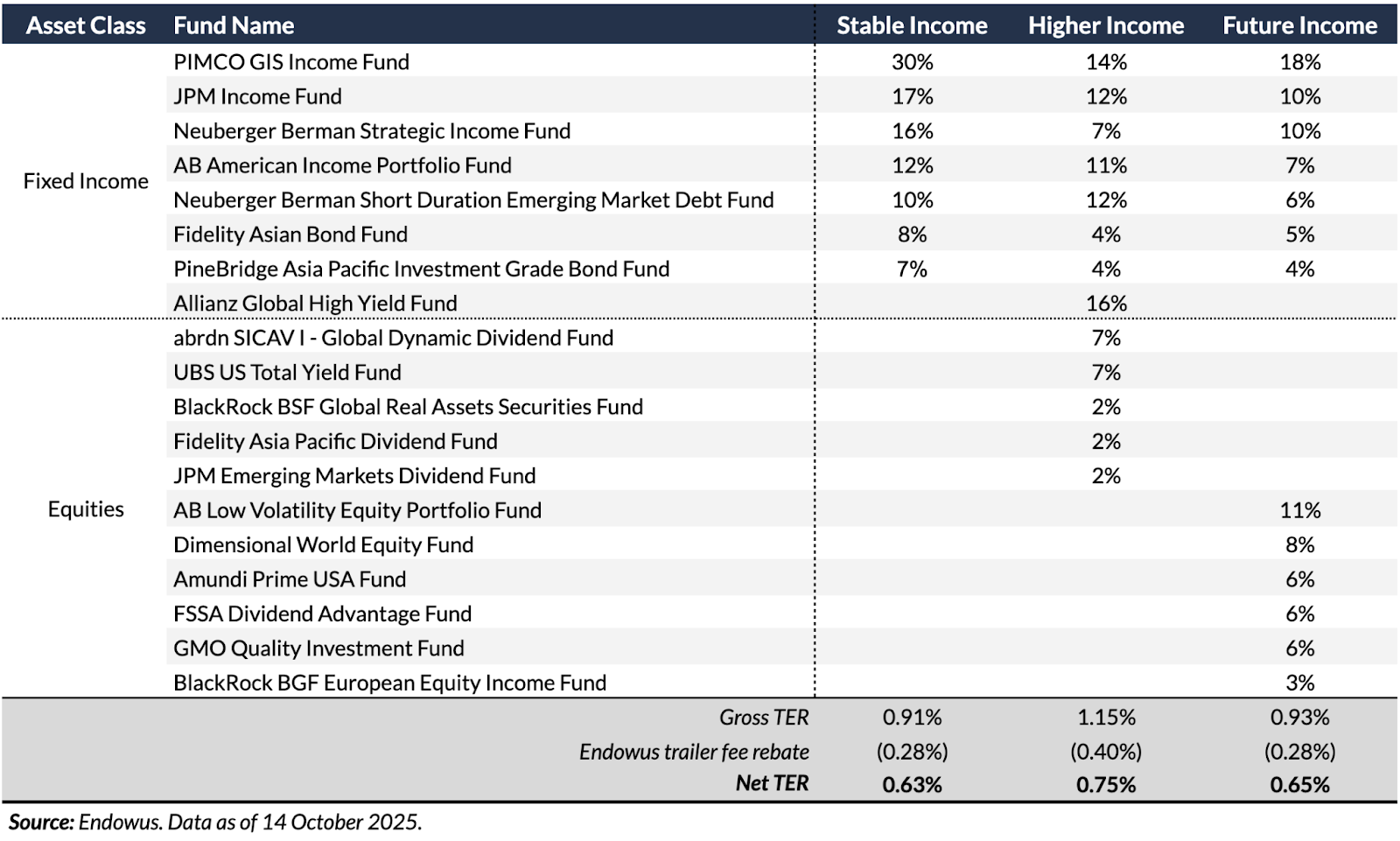

The Income Portfolios are built using a curated basket of income-generating assets, accessed through carefully selected funds. These assets span global high-yield bonds, investment-grade bonds, government bonds, securitised instruments, emerging-market bonds, and dividend-paying equities.

Just as individuals have unique strengths and weaknesses, so do fund managers. A manager skilled in European dividend equities may not be equally adept in the US high yield bond market. That’s why Endowus takes a fund manager-agnostic approach—focused solely on identifying the highest-quality income funds to serve as the building blocks of our portfolios.

Unlike some solution providers that tie up with a single fund manager, Endowus is fund manager-agnostic and is simply single-minded in finding the highest-quality income funds as fundamental building blocks of the portfolios.

We have worked with fund managers who individually specialise in the different income niches — whether higher-yielding fixed income or real asset funds, or high-dividend equity funds. For the three Income Portfolios, we have worked with specialists fund managers who are leaders in their field both globally and locally, including familiar names, such as Aberdeen, Alliance Bernstein, Allianz Global Investors, BlackRock, Dimensional, Fidelity, First Sentier, JP Morgan Asset Management, Neuberger Berman, PIMCO, and Schroders.

The Endowus Investment Office is committed to scouring the globe for Best-in-Class funds and working closely with managers to introduce new strategies. This dedication ensures that investors gain access to institutional-grade portfolios with ease and confidence.

Underlying fund allocation of Endowus Income Portfolios

Why Endowus built the Income Portfolios

The Endowus Income Portfolios were created to meet real, unmet client needs—especially for those seeking consistent income without sacrificing long-term capital growth. Many existing solutions either erode capital to sustain payouts or deliver subpar returns due to poor design, high fees, or limited diversification.

To address this, the Endowus Investment Office focused on four key principles:

- Stable and achievable income distribution Balancing higher-yielding assets with high-quality ones that perform differently across market cycles to deliver consistent target payouts.

- Resilient portfolio construction Partnering with leading global fund managers to manage volatility and adapt to changing macroeconomic conditions.

- All-weather strategy Using a globally diversified, multi-asset, multi-manager approach to access income opportunities regardless of market or interest rate direction.

- Efficient asset allocation Strategically allocating between fixed income and equities to meet each portfolio’s objective—whether capital preservation or long-term appreciation.

Why Endowus for income solutions

Endowus Income Portfolios are independently constructed using a robust, holistic investment process. As an independent financial advisor, Endowus is uniquely positioned to select best-in-class income-generating funds across asset classes—without bias or conflict of interest.

Key differentiators include:

- Fund manager-agnostic approach Each asset class is treated as a building block, with the best product selected for its role—no preference for any single manager.

- Client-first fee structure Endowus is only paid by clients. Unlike other distributors, we do not receive hidden commissions from fund managers. Any trailer fees are rebated 100% back to our clients.

Endowus versus other passive income products

There are many ways to invest for income, but not all are created equal.

Here’s how Endowus stands apart:

- Built for real client needs Our portfolios were designed to address gaps in the market, offering institutional-quality solutions for a wide range of investor profiles.

- Avoiding capital erosion Many products promise high payouts—sometimes up to 8%—but do so by dipping into your principal. Endowus portfolios are structured to avoid this, focusing on capital preservation and growth.

- Designed to avoid decumulation All three portfolios—Stable Income, Higher Income, and Future Income—are built to maintain or grow capital. While underlying funds may occasionally tap into capital to smooth payouts, the overall structure supports sustainability in the long term

- Compared to insurance-linked products Many passive income products like annuities, endowment plans, and insurance-linked solutions have disappointed investors due to high hidden fees, poor asset selection, and weak performance. Endowus offers a transparent, high-quality alternative.

For more details of all three Endowus Income Portfolios, click here. To get started, follow this link.

Webinar: Choosing the right robo advisor in Singapore - Comparing Endowus with the rest

Webinar: Endowus Q2 2021: Performance review and market insights

Webinar: Endowus Q3 2021 Performance review and market insights

%20F1(2).webp)

.webp)

.webp)