.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

.jpg)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Return outcomes depend heavily on strategy, manager selection, and market conditions.

- Diversification benefits are uneven. Like infrastructure and transport real estate, they offer low correlation to traditional stocks and bonds. Others like private equity and some hedge funds may face similar risks as public equities.

- Alternatives can enhance portfolio resilience, but they come with trade-offs like illiquidity and higher fees.

- Allocation to alts should be tailored to individual risk tolerance, time horizon, and liquidity needs, not driven by headline returns alone.

Alternative investments have moved from niche to mainstream – especially following regional regulators’ push. But for many investors, they still raise fundamental questions.

From return potential to risk perception, illiquidity to diversification, the world of private markets and hedge funds can feel opaque. This article tackles four of the most common questions beginners ask—offering clarity on performance, cost, portfolio fit, and allocation strategy.

Whether you're exploring alts for the first time or refining your understanding, this article will help answer the five most common questions.

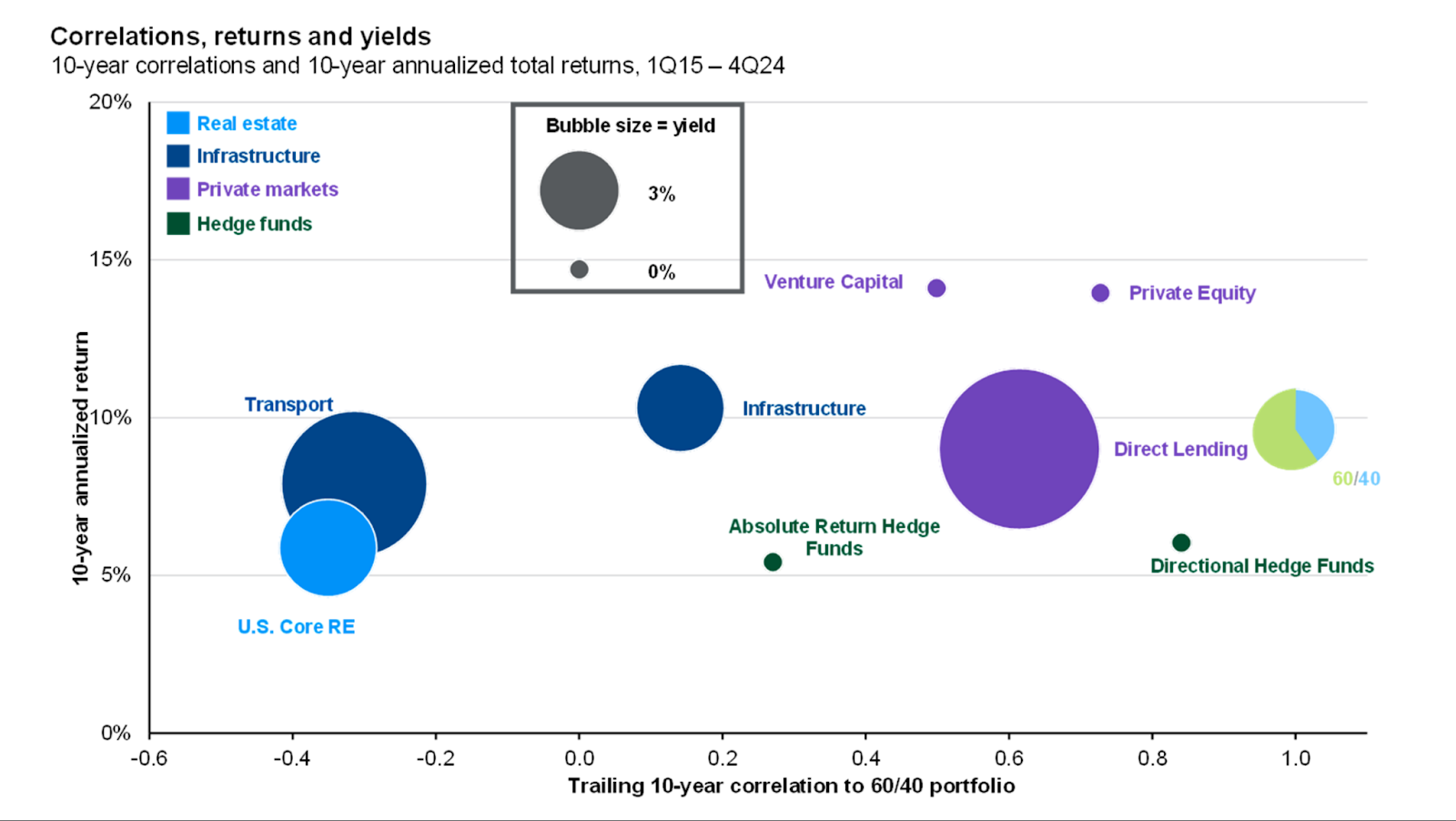

1. Do private markets and hedge funds really generate higher returns?

Private markets are a motley crew, and so are hedge funds. They stand for a diverse collection of strategies, and this means their performance can vary significantly.

For private markets, the data from the past decade suggests that the strategies have generally delivered higher returns than traditional portfolios, though outcomes can vary widely by strategy and vintage. Private equity and private credit also appear strong, with returns around 15% and 10% respectively, and the latter offering notably high yield.

Hedge funds present a more mixed picture—while some strategies outperform the 60/40 benchmark, directional hedge funds hover around the same ~5% return with higher correlation.

Private market opportunities are often limited to a smaller pool of assets, which can increase the chance of generating alpha. Without strict benchmarks—and with tools like shorting and derivatives in hedge funds—managers have more flexibility to outperform. Plus, because investors commit long-term capital, they may earn an illiquidity premium from companies willing to pay more for stable funding.

The takeaway is that return outcomes vary widely across strategies, even within the same asset class. Performance depends heavily on manager selection and market conditions, making due diligence critical to success.

2. If private markets and hedge funds generate higher returns, should I allocate more of my portfolio into these assets?

The answer is not a simple yes or no. The decision is never about a blanket prioritisation of one asset class over another. While private assets can offer unique risk-return characteristics and potential benefits, it is crucial to consider a comprehensive set of factors before making any investment decisions.

Private markets can offer compelling return and yield profiles, they also come with trade-offs: illiquidity, longer investment horizons, higher fees, and greater dispersion in outcomes. Traditional assets still play a critical role in providing liquidity and transparency, especially in volatile or uncertain environments.

The optimal approach is about thoughtful integration, which is allocating to alternatives in proportion to one’s risk tolerance, time horizon, and need for diversification. Prioritising alternatives may enhance portfolio resilience and return potential, but only when balanced against the foundational strengths of traditional assets.

For instance, an investor with a very long time horizon – let’s say with decades until retirement – and a high tolerance for risk might find a carefully selected private equity allocation suitable, as they can absorb the illiquidity and potential short-term volatility for the prospect of higher long-term returns. Conversely, someone nearing retirement with a lower risk appetite and a need for more immediate access to funds might prioritise more liquid and stable traditional assets.

Your personal circumstances, financial objectives, and comfort with risk should always drive your allocation decisions.

3. I heard that private market strategies and hedge funds are expensive. Is that true?

Yes, they are generally more expensive, especially when compared to low-cost unit trusts and passive index funds. Performance-based fees are common. But the higher fees are not arbitrary. They reflect the complexity of strategies, reward skill and performance, open up access to exclusive asset classes, and in some cases, help align incentives between general partners (GPs), who manage the investments, and end-investors.

In hedge funds, fees are often structured under the well-known “2 and 20” model. A 2% management fee is charged annually on assets under management. A 20% performance fee is applied to profits, typically above a hurdle rate (a minimum return) and subject to a high-water mark, ensuring fees are only paid on new gains.

For private market strategies, an annual management fee is charged on committed capital for closed-ended funds and on net asset value (NAV) for evergreen structures. Another cost is carried interest, which is a share of the profits that fund managers earn only if the investment performs well.

That brings us to the question of “is it worth it?” These can be worth it if the strategies deliver net-of-fee alpha, diversification, and access to opportunities unavailable elsewhere. But the burden of proof lies with the GPs to deliver, and with you as the investor to assess whether the solution fits your broader goals.

4. Does the inclusion of private market investments help diversify my portfolio?

Yes, and to a varying degree.

Several alternative strategies, particularly in real assets and private markets, show low to even negative correlation to a traditional 60/40 portfolio. Transport real estate and infrastructure, for instance, exhibit correlations near -0.3 and -0.1, respectively, while still delivering solid returns and attractive yields.

In contrast, some hedge fund strategies—especially directional ones—track closely with public markets, limiting their diversification benefit.

Similarly, private equity tends to be correlated with public equities, as both involve ownership stakes in companies and share the risk of capital loss when underlying valuations decline. They are also influenced by broader economic factors, including market conditions, company performance, industry trends, and macroeconomic shifts such as interest rate changes and inflation. While private equity may offer an illiquidity premium, its exposure to business cycles and company-specific risks often mirrors that of public equity.

The key is to analyse each alternative investment on its own merits and its expected behaviour relative to your existing portfolio.

5. Does the illiquidity of private market strategies and hedge funds make volatility irrelevant?

Illiquidity can obscure volatility, but it doesn’t eliminate it.

Private market strategies often report smoother return profiles due to pricing on a less frequent basis, often based on “events” such as the pricing of the latest fundraising round of the company. These methods of estimating the value of an asset can mask underlying market fluctuations. This perceived stability may offer psychological comfort during periods of public market stress, but it doesn’t mean the assets are immune to risk.

Economic downturns, shifts in credit conditions, or operational challenges can still materially impact performance—just not always in real time.

Hedge funds, depending on their strategy, may also exhibit dampened volatility, especially in less transparent or less frequently traded positions. Ultimately, while illiquidity can reduce mark-to-market noise, it doesn’t negate the importance of understanding the true risk embedded in these strategies.

Therefore, while the reporting of volatility might be less frequent due to illiquidity, the underlying risk of significant value changes remains very real and can be substantial.

Conclusion

Alternatives or not, the potential for higher returns is inherently tied to the assumption of risk.

Whether through illiquidity, complexity, or market exposure, every investment decision carries trade-offs. Private markets may offer compelling upside and diversification benefits, but they demand patience, selectivity, and a clear understanding of underlying risks. Hedge funds, too, can provide unique—yet their effectiveness depends heavily on strategy and execution.

Ultimately, the question isn’t whether alternatives are better than traditional assets, but how they fit within a broader, well-calibrated portfolio. Thoughtful allocation—grounded in objectives, time horizon, and risk tolerance—is what turns access into advantage.

How hedge funds can help you ride through market volatility

Is wine a good investment? The liquid illiquid asset

How US private credit can endure downturns

.jpg)

%20F1(2).webp)

.webp)

.webp)