.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- For CPF members below 55, surplus Ordinary Account (OA) savings can be put to work by transferring them to their Special Account(SA) for higher interests (4.0% p.a. versus 2.5% p.a.) to compound over time. The trade-off is irreversibility and lost flexibility

- Before making an OA-to-SA transfer, consider cash top-ups, which qualify for tax relief, while OA-to-SA transfers do not.

- Those with surplus OA savings and have not reached the Full Retirement Sum in their SA balance may consider a transfer, but the decision should be part of a broader retirement strategy, not just based on differential interest rates alone.

For most Singaporeans, the Central Provident Fund (CPF) is the most reliable source of retirement income. The CPF Ordinary Account (OA) serves an important early purpose: it is the primary vehicle for servicing a housing mortgage, which for most members is their largest financial obligation. Once the mortgage is paid off, next comes the question of how to put the surplus OA savings to work.

One of the most common strategies is to transfer OA to their own Special Account (SA). At 4.0% per annum versus the OA's 2.5%, the SA compounds more efficiently over time. But the transfer is irreversible before age 55, and there are considerations—particularly around the Retirement Sum Topping-Up (RSTU) scheme—that affect whether and when a transfer makes sense.

Why OA and SA earn different interest rates

CPF accounts are structured around specific financial objectives.

The OA prioritises accessibility. Members may draw on OA funds for housing purchases and mortgage servicing, education, insurance premiums, and investments through the CPF Investment Scheme (CPFIS). This flexibility comes at a cost: the OA earns a lower base interest rate of 2.5% per annum.

The SA is designed for long-term retirement accumulation. Funds are largely inaccessible before retirement age, which allows the SA to offer a guaranteed 4.0% per annum floor, but with reduced liquidity options.

Members below age 55 also receive an additional 1% per annum on the first S$60,000 of combined CPF balances, with the OA component capped at S$20,000. This extra interest applies to both accounts, though it does not change the structural logic.

The financial case for OA-to-SA transfer

The primary argument for a transfer is straightforward: higher risk-free compounding over time.

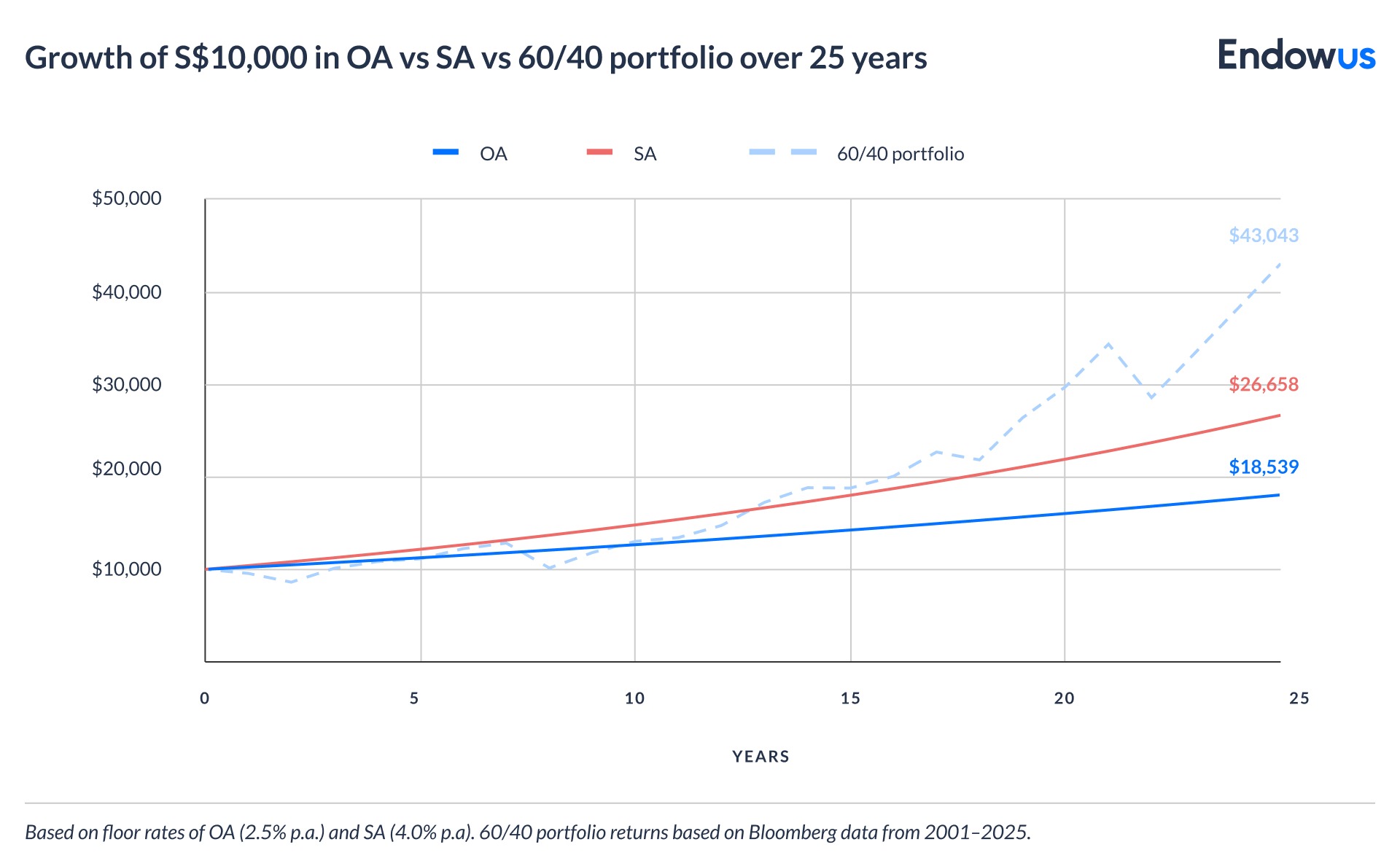

Consider S$10,000 transferred at age 30 and left untouched until age 55. At 4.0% per annum in the SA, the balance grows to approximately S$26,700. At 2.5% in the OA, it reaches roughly S$18,500. The difference—around S$8,100—reflects the effect of 25 years of compounding on what appears to be a modest rate gap.

For members who have already paid off their mortgage, OA balances above what is needed for other purposes, such as education, are surplus. Transferring those funds into the SA captures the higher risk-free return and, over a long enough horizon, builds meaningfully toward retirement milestones such as the Full Retirement Sum (FRS).

Trade-offs of OA-to-SA transfer: irreversibility and lost flexibility

The case against transferring is equally clear: OA-to-SA transfers are irreversible.

OA balances also carry optionality. Members can deploy capital through the CPF Investment Scheme (CPFIS) or retain the funds as a liquid buffer within the CPF system. A transfer to the SA removes all of these options for the transferred amount.

It is also worth recognising that the OA is not idle capital. At 2.5% per annum, with an additional 1% on the first $20,000, it offers a guaranteed return. The question is whether the incremental gain from the SA justifies permanently surrendering what the OA makes possible.

That answer depends on what the flexibility is actually worth at various life stages, differing across individual circumstances.

Should you make an RSTU cash top-up before considering an OA-to-SA transfer?

Before making an OA-to-SA transfer, it is worth considering whether you have capacity to make cash top-ups to your SA under the RSTU.

RSTU includes both cash top-ups to SA and OA-to-SA transfers, up to the FRS. Cash top-ups qualify for personal income tax relief of up to S$8,000 per calendar year, while OA-to-SA transfers do not.

Both count toward the same FRS ceiling of SA savings. Because cash top-ups carry a tax benefit that transfers do not, it generally makes sense to do the former first, then direct OA-to-SA transfers at whatever SA shortfall remains.

Another constraint to be aware of: the CPF Annual Limit, currently S$37,740, caps total CPF contributions across all three CPF accounts in a year, including both mandatory and voluntary contributions. Hence, the amount of cash top-ups you can make is capped by both the FRS and CPF Annual Limit.

The last thing to note is that under the RSTU, neither cash top-ups nor OA-to-SA transfers can be invested through CPFIS. Once funds are in the SA via either route, they earn the guaranteed 4.0% floor but are not deployable for investment.

What else should you consider before an OA-to-SA transfer?

Rather than a fixed rule, this decision is better approached as a framework. These are a few considerations:

- Desired SA balance: Transfers can only be made up to the FRS—currently S$220,400 in 2026. Members should be intentional about whether they want their SA to exceed the FRS, as future mandatory contributions will continue to flow into their SA (up to the prevailing ERS).

- Time horizon: The compounding benefits of a transfer become more apparent with time. For members nearing age 55, the impending SA closure will mean that SA amounts above the FRS will be transferred to their OA. Doing an OA-to-SA transfer nearing age 55, in this scenario, may not make a material difference in interests earned.

- OA’s investment flexibility: While SA earns a higher interest rate than OA, retaining your savings in OA allows for them to be invested through the CPFIS. Meanwhile, OA-to-SA transfers made under RSTU are not investible.

- Transfer timing: Should you decide to do an OA-to-SA transfer, it is best to do so early in the year. CPF balances for interests are computed monthly—if you make a top-up in January instead of December, you can earn up to 20% more interest in just 10 years on those monies.

How to transfer OA to SA

OA-to-SA transfers are done through the CPF Board's my cpf online portal. The process is straightforward and takes effect immediately upon submission.

To make a transfer, log in to my cpf at cpf.gov.sg, navigate to "My Request" and select "Building Up My CPF Savings", then choose "Transfer from my Ordinary Account to my Special Account". You will be prompted to enter the amount you wish to transfer and confirm the transaction.

There is no minimum transfer amount. The maximum is limited to the FRS shortfall in your SA—that is, the difference between the current FRS and your existing SA balance. Once submitted, the transfer cannot be reversed.

Should you simply invest your OA?

An OA-to-SA transfer is not a standalone retirement decision. It is one input into a wider framework that includes investment strategy, liquidity management, and long-term income planning.

Within CPF, members with surplus OA savings face three distinct options.

- Leaving funds in the OA earns 2.5% per annum—a guaranteed return, but the lowest of the three.

- Transferring to the SA earns 4.0% per annum, also guaranteed, but permanently locks the capital before age 55.

- Investing OA funds through CPFIS, which introduces market risk in exchange for the possibility of returns that exceed either CPF floor rate, comes without the irreversibility of a transfer.

A higher Retirement Account (RA) balance at age 55—built from SA savings—translates directly into higher monthly payouts under CPF LIFE. For members preferring a risk-free approach, disciplined SA accumulation through cash top-ups or OA-to-SA transfers over a long horizon may be a cost-effective path, given the guaranteed 4.0% return.

For those willing to take some market risk, members can invest their OA savings through CPFIS in a range of approved investment products. Over sufficiently long horizons, a globally diversified portfolio has historically outperformed the OA's 2.5% floor—though this outcome is not guaranteed and carries short-term volatility that the SA does not. For members with surplus OA balances and a long time horizon, investing through CPFIS may complement SA accumulation rather than replace it.

For members approaching retirement, the priority typically shifts toward income certainty. In that context, a well-funded SA—and the CPF LIFE payout it supports—may matter more than additional investment exposure.

Frequently asked questions about OA-to-SA transfers

What is a CPF OA-to-SA transfer?

A CPF OA-to-SA transfer moves funds from the Ordinary Account to the Special Account within the CPF framework. The primary effect is that the transferred balance earns 4.0% per annum instead of 2.5%, compounding at a higher rate toward retirement. Transfers are irreversible.

What are the conditions and limits for CPF OA-to-SA transfers?

Transfers can be made up to the Full Retirement Sum (FRS) in the SA, which is S$220,400 in 2026. Members cannot transfer more than the FRS shortfall in their SA. The transfer must be made voluntarily through the CPF Board's online portal, and the amount transferred is permanent — it cannot be returned to the OA before retirement age.

Is an OA-to-SA transfer the same as a CPF cash top-up?

No. While both may fall under the RSTU scheme, cash top-ups qualify for personal income tax relief, while OA-to-SA transfers do not.

Can I transfer OA savings to my MediSave Account (MA)?

Not if you are below age 55. OA-to-MA transfers are only available to members aged 55 and above, and only after meeting additional conditions: they must have set aside the FRS (or BRS with a property pledge), and their MA balance must not have met the Basic Healthcare Sum. Members below 55 who wish to increase their MediSave balance should explore cash top-up instead.

Does the SA closure policy at age 55 affect OA-to-SA transfers?

Yes. The CPF Board has announced that the SA closes at age 55, at which point SA savings are transferred into the Retirement Account up to the prevailing FRS, with any remainder moving to the OA. For members well below age 55, the SA remains the appropriate long-term retirement savings account in the interim.

Should I transfer CPF OA to SA or invest through CPFIS?

This depends on your risk tolerance, investment horizon, and whether your OA balance is genuinely surplus. The SA offers a guaranteed 4.0% floor with no investment risk or cost. CPFIS investments in equities or bond funds may deliver higher expected returns over time, but carry variability and cost that the SA does not. For many members, a combination—retaining some OA for CPFIS while designating true surplus as a transfer candidate—may be more appropriate than an either/or choice.

Endowus CPF Portfolios outperform average returns of CPF Investment Scheme (CPFIS)-included funds in 2020

5 Things to know before investing your CPF

Webinar: Starting your CPF Millionaire journey early

%20F1(2).webp)

.webp)

.webp)