.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Markets consistently misprice geopolitical shocks by extrapolating short-term disruption into permanent structural damage, creating opportunities for disciplined long-term investors.

- The most common errors are linear thinking, binary positioning, and over-reliance on historical analogies—all of which lead investors to overprice tail risk and panic-sell, at times just when the market starts to recover.

- Staying diversified, maintaining a long-term horizon, and selectively allocating to private markets and alternatives may offer the most durable path through geopolitical volatility.

Markets are poor students of geopolitics—and that can typically create opportunity.

When conflict erupts or a political shock lands, the typical market response is immediate—oil prices can spike (or in the case of COVID-19, tank), safe-haven assets attract inflows, and certain sectors reprice on sentiment before fundamentals catch up. Most of those moves tend to reverse. Marko Papic, Chief Strategist at Clocktower Group and author of Geopolitical Alpha: An Investment Framework for Predicting the Future, has spent his career explaining why this happens—and how disciplined investors can position themselves on the other side of it.

His framework explains the difference between geopolitical beta and geopolitical alpha.

Geopolitical beta and alpha: the core framework

Geopolitical beta refers to broad, structural forces such as demographic shifts, the rewiring of supply chains for national security, and the long-term transition to energy independence. These move regardless of the daily news cycle or the stated preferences of individual politicians.

Geopolitical alpha is what an investor generates by looking past the market's immediate emotional reaction to a geopolitical shock—avoiding linear extrapolation and binary thinking—to identify the mispriced second- and third-order effects. First-order effects are easy to forecast. They are also, in Papic's view, largely irrelevant to long-term portfolio construction. It is the effects that follow that are least priced in. For instance, how to position for a market rebound after the initial COVID-19 shock.

This distinction matters more today than it did a generation ago. Most current professional investors built their careers between the 1980s and the early 2020s—four decades during which geopolitics barely registered as a variable in portfolio construction. That experience has left the median investor ill-equipped for a world where political and geopolitical factors influence asset prices with far greater frequency.

Papic identifies five recurring mistakes that follow from this gap.

Lesson 1: Avoid linear extrapolation of geopolitical events

The most common error is treating an ongoing geopolitical event as a permanent inflection point. Russia's invasion of Ukraine, in this reading, becomes a rupture that changes everything, even though Russia and Ukraine had already fought a war in 2014–15.

The S&P 500 trajectory tells a more measured story. Despite a relentless sequence of geopolitical shocks over the past two decades—trade wars, pandemics, armed conflicts—the S&P 500 largely continued its long-run upward trajectory. When the index did fall sharply, declining 25% from peak to trough between 3rd January and 12th October 2022*, the driver was an economic cycle unwinding, not a geopolitical event determining a new normal. Investors who extrapolated geopolitical disruption into permanent structural damage tended to reduce risk at precisely the wrong moment—buying high on the way up and selling low on the way down.

Lesson 2: Resist binary thinking

Investors tend to apply binary thinking to most economic events. For instance, an inflation print or a non-farm payroll number have certain consequences attached to it. So do Federal Reserve Board meetings. Geopolitical events? Not so much.

When Saudi Arabia declined US requests to increase oil production in February 2022, many investors read it as confirmation of an emerging Saudi-Chinese alliance—a clean, adversarial binary. In reality, Beijing wanted exactly what Washington wanted: more supply and lower prices. The situation was not a 1 or a 0. It rarely is. Geopolitical outcomes almost never resolve into the clean, decisive scenarios that binary positioning assumes - and portfolios built around such assumptions tend to be whipsawed when the nuance reasserts itself.

Lesson 3: Be cautious with historical analogies

Faced with unfamiliar geopolitical terrain in the early 2020s, many investors reached for intellectual shortcuts. The Cold War became the template for US-China relations. The 1970s became the model for inflation. The Spanish flu became the lens for COVID-19.

The danger is that analogies actively misrepresent the present. The Cold War, for instance, was not a period of sustained confrontation—it moved through extended cycles of escalation and accommodation.

More problematically, investors tend to reach for the most dramatic historical precedents rather than the far larger number of more mundane ones. The result is a systematic tendency to overprice tail risk and underprice the more probable, less cinematic outcomes.

Lesson 4: Understand that unsustainable trends reverse, but timing is not a strategy

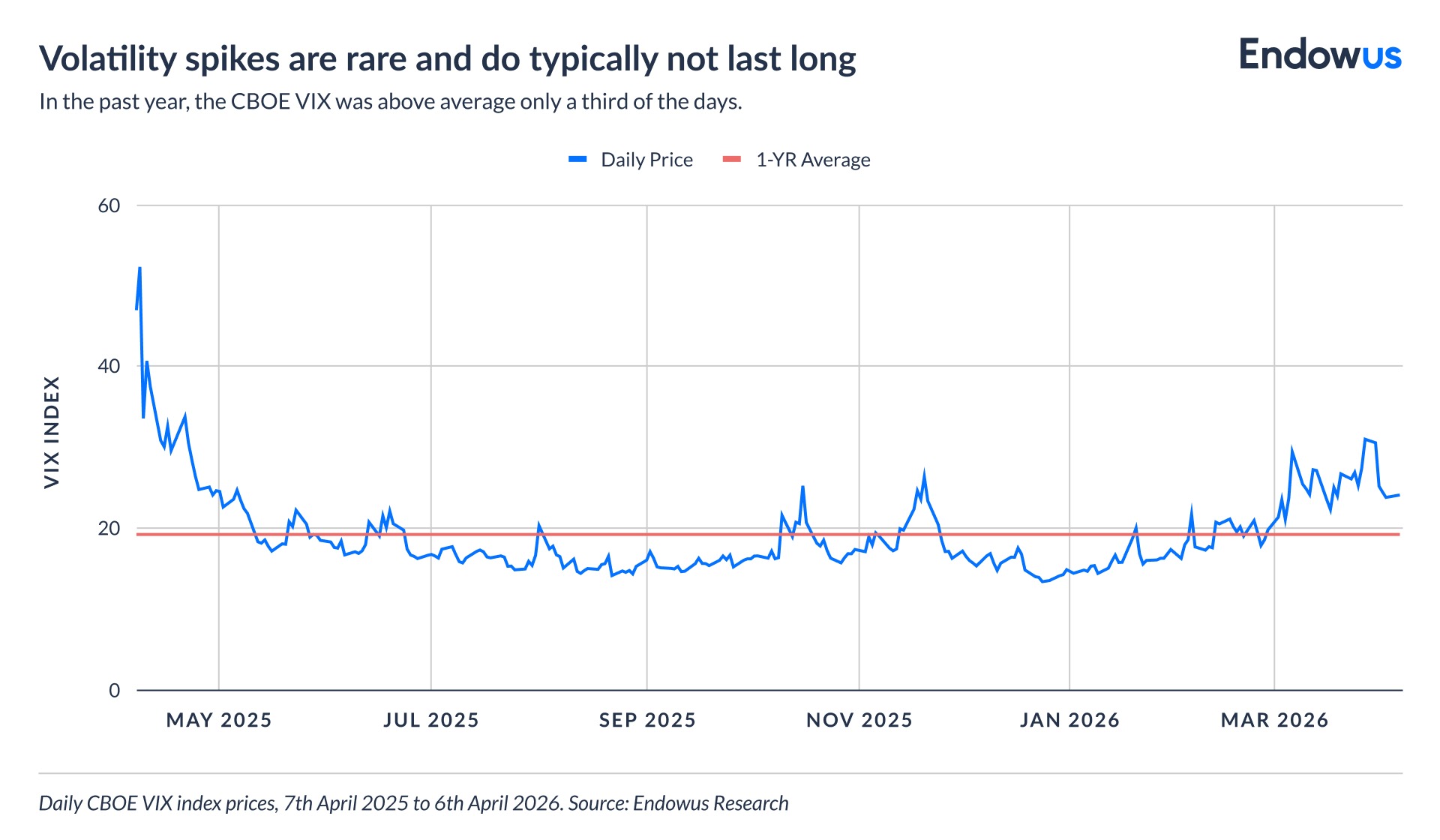

Geopolitical and political trends at an extreme are likely to unwind. The direction of travel may be clear even when the timing is not, and that gap is where most investors come unstuck. Attempting to time the tide change is a fool’s errand. Instead, investors should know that contrary to what it may appear from news headlines, high volatility in financial markets is typically short-lived.

Lesson 5: Scarcity drives innovation—and markets consistently underestimate this

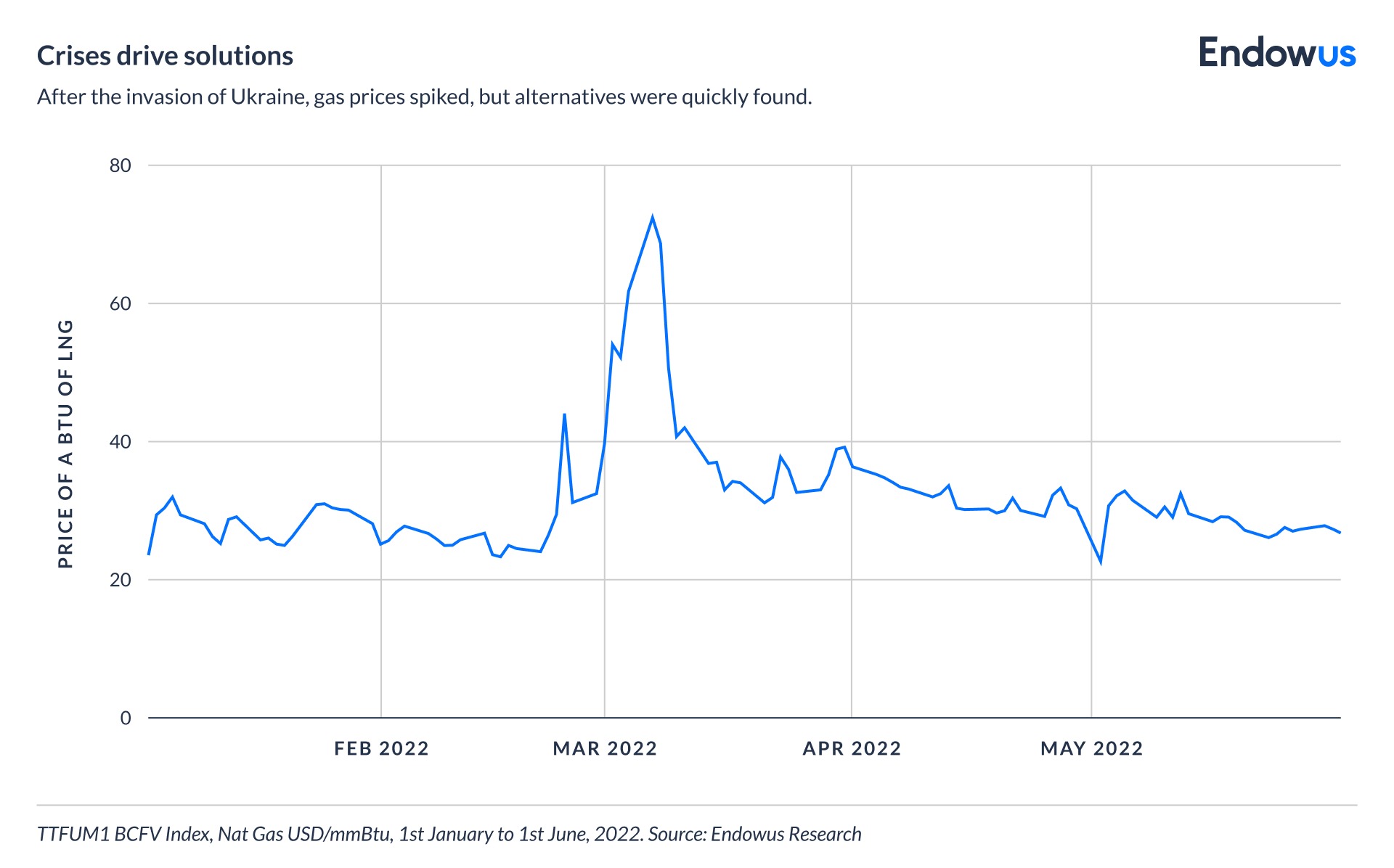

History rarely unfolds along the path that crisis-era forecasts project. When Europe faced an acute energy shortage following Russia's invasion of Ukraine, the consensus view was that the resolution of the energy shortage would take years, if not decades. Instead, Europe built liquefied natural gas (LNG) import capacity far faster than most analysts thought possible.

Conversely, the EU oil embargo on Russia, widely seen as a decisive blow to Russian export revenue, barely dented Russia's exports. If anything, the war pushed global crude prices lower as Russia accepted steep discounts to maintain volumes.

The worst-case forecasts were not wrong because the crisis was overstated. They were wrong because the adaptive response—policy pivots, financial engineering, and technological innovation—was systematically underestimated.

The same dynamic is already visible today. Disruption to vital maritime choke points is accelerating the development of alternative supply chains. Crises motivate countries and companies to innovate at a pace that markets, anchored to the status quo, consistently fail to price in. Investors who model only the disruption—and not the response—will be wrong in the same direction, repeatedly.

The deeper challenge: Why quantitative models struggle with geopolitics

Underlying all five lessons is a structural problem. The financial industry has become highly quantitative. Geopolitics is not. Unlike nonperforming loan levels or spread movements, the geopolitical realm resists easy modelling. Quantitative tools may not be able to explain political variables.

It is also worth noting that a higher frequency of geopolitical conflict is not necessarily damaging for growth or inflation. In Papic's view, both may surprise to the upside—growth benefiting from unexpected productivity gains, inflation remaining relatively contained even if not precisely anchored to central banks' ~2% targets (which are in any case a product of a specific economic cycle—the globalized growth of the 1990s and early 2000s).

The result is a more constructive macro backdrop than a linear reading of current tensions might suggest.

Investment implications for long-term portfolios

Past the initial shock of conflict and geopolitical disruption, it is the second-order effects (long-term consequences on economic trends and international relations) that carry stronger and more durable implications for portfolios.

This points to two practical conclusions.

First, staying diversified and maintaining discipline through geopolitical volatility remains the most reliable approach. Attempting to time markets based on news cycles—rotating in and out of positions on each new headline—is likely to generate worse outcomes than a well-constructed, risk-aware portfolio held through the turbulence.

Second, for investors with appropriate time horizons, alternative assets may offer a way to capture macro-level structural shifts without being shaken out by daily geopolitical noise. Private markets—private equity, private credit, and infrastructure—can potentially provide insulation from public market volatility while allowing investors to benefit from structural trends that play out over the long run. They can also be a guardrail against the temptation to panic-sell, which is a major drag on returns.

*Data source: Bloomberg. The index closed at 4,796.56 on 3rd January, 2022, and was down to 3,577.03 on 12th October, 2022.

Forget your password? It's a good thing for your investments

The lesson of Hyflux: What water and diversification have in common

Free lunch: Diversification in investing is a gift

.jpeg)

%20F1(2).webp)

.webp)

.webp)