.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

The original version of this article first appeared in The Business Times.

For generations of Singaporeans, the Central Provident Fund (CPF) has been the bedrock of financial security. Its tiered interest rates—2.5% for the Ordinary Account (OA) and 4% for the Special Account (SA)—are often regarded as the ultimate "risk-free" benchmark. In a volatile world, the psychological comfort of a government-guaranteed return is hard to overstate.

However, as the financial landscape evolves, a "risk-free" return can ironically become a risk in itself: the risk of falling behind. In the recent past, we have gone through a period of high-inflation, and the real value of OA balances has struggled to keep pace with the rising cost of living at the base rate. When the "science of wealth" is applied to retirement planning, it becomes clear that for many Singaporeans, the greatest threat to their golden years is not market volatility, but the erosion of purchasing power.

The changing CPF investing landscape

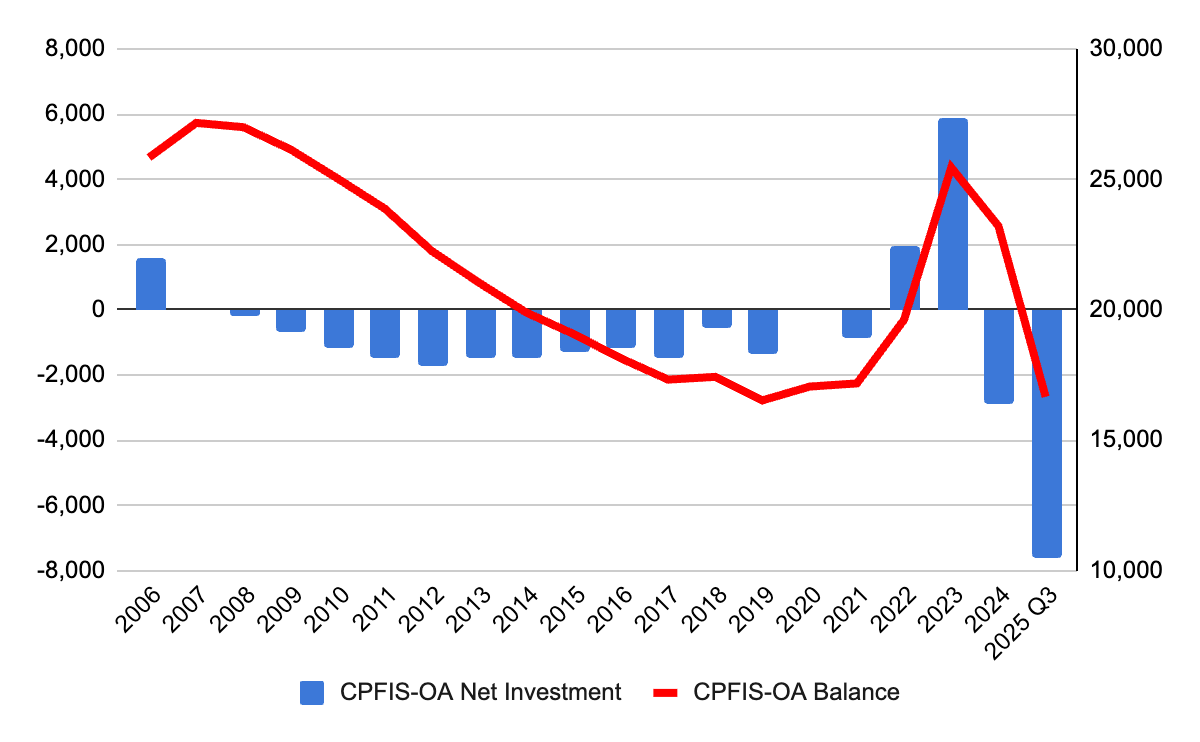

Recent shifts in the CPF landscape have brought these considerations to the forefront. The closure of the Special Account for members aged 55 and above, which started in 2025, has forced many "young seniors" to rethink their strategies. While RA (Retirement Account) savings earn a healthy 4% or higher, any excess from the shuttered SA is now funneled back into the OA at 2.5%.

This "right-siting" of funds has coincided with a recent discussion in Parliament on the Lifetime Retirement Investment Scheme (LRIS). In a recent parliamentary session, Minister for Manpower Dr. Tan See Leng highlighted that the government is in the final stages of studying the LRIS to provide members with more streamlined, low-cost investment options that strike a better balance between risk and return.

Since Endowus, the first digital advisor for CPF Investment Scheme (CPFIS) was included in 2019, many changes have occurred to lay the groundwork for more to be done to help CPF members navigate the complicated investment landscape with more clarity and transparency. The message is clear: the status quo is being challenged. Many segments of the market including the government and market players all seem to recognise that for CPF to remain "fit for purpose", members need better ways to grow their nest eggs beyond the default rates.

CPF members pull money out of CPFIS as interest rates fall

The Complacency Trap: Why investing is mandatory, not optional

We are now entering a period where the aging population and rising income of Singaporeans means CPF contributions coupled with interest payments and top ups will accelerate the total pool of money in CPF. The math on the OA returns is simple but sobering. From 1961 to 2024, Singapore’s average inflation was approximately 2.6%. In the past few years, we have seen spikes as high as 3.9%. If the cost of a bowl of noodles or a doctor’s visit is rising at more than 2.5%, your "wealth" is effectively shrinking.

To make more use of the CPF balance and reach retirement safety, one must look toward the CPFIS. Historically, many were cautioned against investing, citing data that showed a majority of investors failed to beat the base rate hurdle. However, this narrative and more importantly, the data is changing.

Data from the past few years reveals a significant shift: the vast majority of CPF members who invested in Unit Trusts have actually done remarkably well. This is partly due to a more robust global market, but also a shift toward more sophisticated, low-cost investment vehicles and digital platforms.

Performance matters: The reality of higher returns

Compared to a few years ago, there are now lower cost and broadly diversified options available for CPF members. For example, investing into a diversified global equity portfolio could have generated an actual annual average return of 11.2% over the past five years.

Compare $100,000 left in the OA at 2.5% versus the same amount invested at 11.2%. Over five years, the OA balance would grow to roughly $113,141. In the investment portfolio, that same $100,000 would have grown to over $170,000. That is a difference of $57,118—money that could mean the difference between a basic retirement and a comfortable one.

Of course, investing involves risk. Markets can and do go down. But the "science" part of wealth management teaches us that risk is not a binary on/off switch; it is a dial that can be managed through time and diversification. Furthermore, the longer you invest, the risk of losing money decreases significantly. In fact, over a 10-year horizon, the probability of a globally diversified equity portfolio underperforming a cash rate is statistically extremely low.

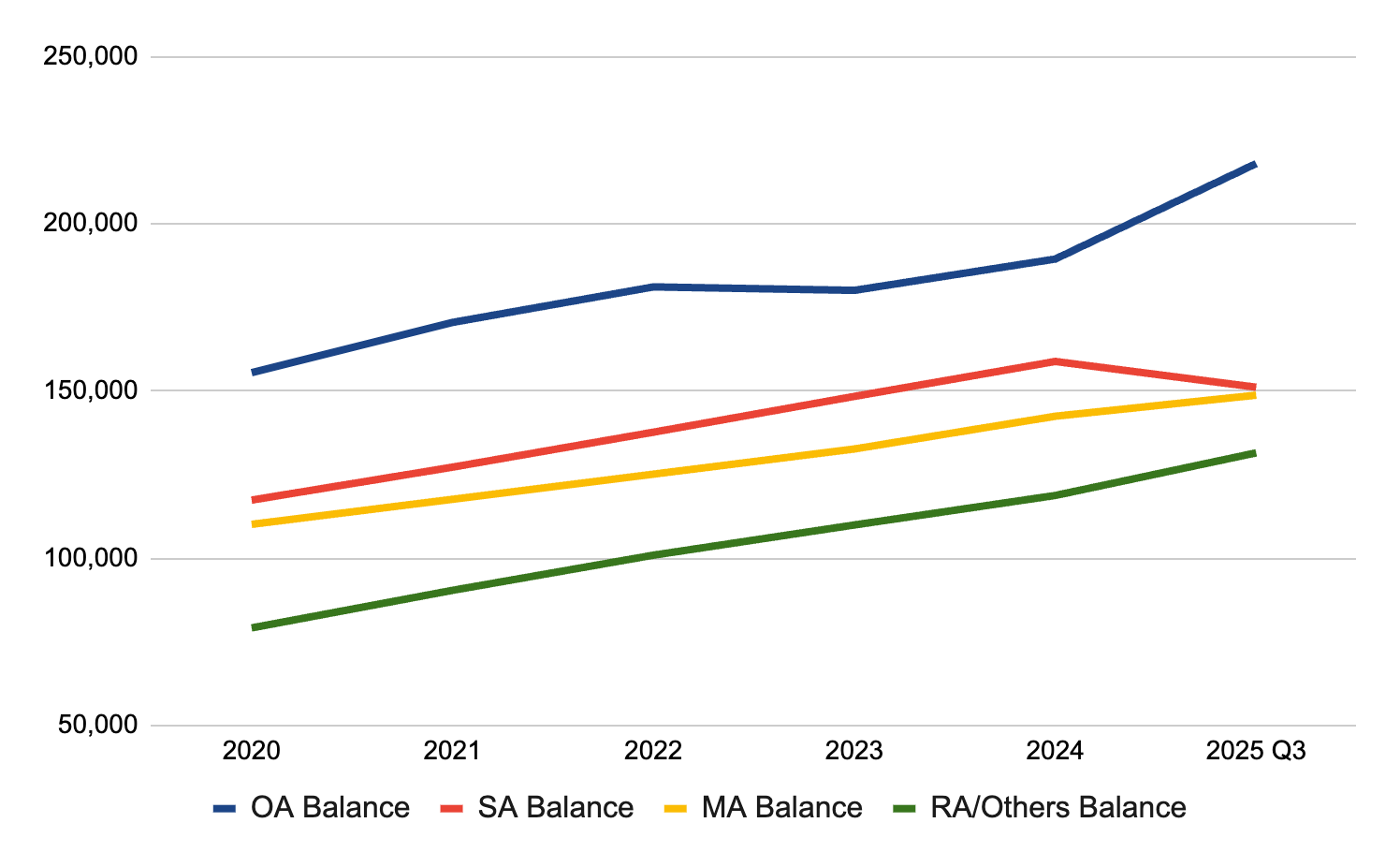

CPF OA balance will become even more important as time goes by

The Performance Gap: Unit trusts vs. ILPs

One of the most critical revelations in recent CPFIS data is the stark performance gap between different product types. For years, many Singaporeans were sold Investment-Linked Products (ILPs) for their CPF savings. While these products offer a veneer of "protection" alongside investment, the data suggests they have been a significant drag on wealth.

ILPs have typically underperformed Unit Trusts by an average of 1-1.5 percentage points per annum. This "ILP tax" is often the result of high embedded commissions, distribution costs, and complex fee structures that eat into the compounding effect. In the world of finance, a 1.5% annual drag over 30 years can result in a final nest egg that is 35% smaller.

This is why the role of the advisor has become so critical. In the past, "advice" was often synonymous with "sales." Today, the modern advisor's role is to provide guidance that is evidence-based and conflict-free.

The role of the advisor in the CPF journey

Why do people still struggle to beat the 2.5% OA rate? Usually, it isn’t because their behaviour failed them; it’s because of human emotions and high costs. Investors often buy when markets are at an all-time high and panic-sell during a dip. They also underestimate the impact of recurring fees that drag on returns. This is where guidance and support become the critical factors for success over the long term.

Minister Tan’s discussion of the LRIS underscores a national recognition that "guidance" is a public good. While the LRIS may provide a simplified pathway, proactive investors can already take control of their journey by seeking out platforms that prioritize transparency and long-term success.

Path to becoming a CPF millionaire

To become a CPF millionaire, time and discipline are your greatest allies. The journey starts with a simple shift in mindset: viewing your CPF OA not as a "savings account," but as a "retirement investment account." Consider the power of compounding. If a 30-year-old invests $50,000 and contributes an additional $500 monthly, at a 2.5% return, they would have roughly $400,000 by age 65. If they achieve a 7% return through a diversified portfolio, that sum balloons to over $1.1 million.

The difference isn't just a number; it is life options. It is the ability to choose when to retire, how to care for one's health, and how to support the next generation.

The Science of Wealth has always advocated for rational, data-driven decision-making. Today, the data is telling us that the perceived "safest" choice—doing nothing with your CPF—might actually be the riskiest long-term strategy for your retirement.

With the upcoming refinements to the CPF scheme and the potential implementation of the LRIS, Singapore is entering a new era where options to reach retirement adequacy will increase and the probability of a better outcome can be enhanced. However, you don't have to wait for policy changes to take the lead. By moving away from high-cost ILPs, embracing low-cost Unit Trusts, and leveraging professional guidance to navigate market cycles, every Singaporean has the chance to turn their CPF into a powerful engine for wealth creation. The guarantee rate is a floor, not a ceiling. It’s time we started looking up.

Endowus CPF Portfolios outperform average returns of CPF Investment Scheme (CPFIS)-included funds in 2020

5 Things to know before investing your CPF

Webinar: Starting your CPF Millionaire journey early

%20F1(2).webp)

.webp)

.webp)