.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Whether to pay down a mortgage or invest depends on one core comparison: the guaranteed after-tax return of debt reduction versus the uncertain—but typically higher—long-run return of a diversified portfolio.

- A broadly diversified portfolio typically outperforms mortgage prepayment on a return basis, but higher mortgage rates, shorter horizons, and genuine drawdown intolerance can potentially shift the calculus.

- For most Singaporean homeowners, the right answer should be a mix of the two—maintain standard repayments while investing consistently, with CPF Ordinary Account (OA) and Supplementary Retirement Scheme (SRS) mechanics adding more specific tax advantages.

For homeowners with surplus capital, few financial decisions feel as consequential as this one: accelerate mortgage repayment, or invest that capital in financial markets?

The question has a clean surface logic—eliminate a known liability versus build a growing asset—but the correct answer is rarely as straightforward as either framing suggests.

Every dollar applied to mortgage prepayment—factually though not nominally—earns a return equal to the mortgage interest rate. Every dollar invested earns an uncertain return that has historically exceeded most mortgage rates over sufficiently long period—but comes with drawdowns, volatility, and no guarantee of any particular outcome.

This piece works through the key variables—mortgage rate, investment horizon, tax position, CPF, and SRS—so you can make the decision that fits your circumstances.

What is the actual return of paying off your mortgage?

Mortgage prepayment earns a guaranteed, risk-free return exactly equal to the mortgage interest rate. If your mortgage carries a rate of 3.5% per annum, every dollar of prepayment earns 3.5%—with no volatility and no drawdown risk. That is the baseline against which every investment alternative must be compared.

In Singapore, mortgage interest is not tax-deductible for owner-occupied residential properties. The effective “return” of mortgage prepayment therefore equals the nominal rate directly, with no adjustment required. In jurisdictions where interest is deductible (such as the United States), the calculus shifts in favour of investing all other things equal, but that complication does not apply here.

Prepayment return is guaranteed in absolute terms but not in opportunity cost terms. Deploying capital into a mortgage denies the opportunity to invest elsewhere. The question is not whether prepayment earns a real return—it does—but whether that return is the best available use of the marginal dollar.

How does mortgage prepayment compare to investing?

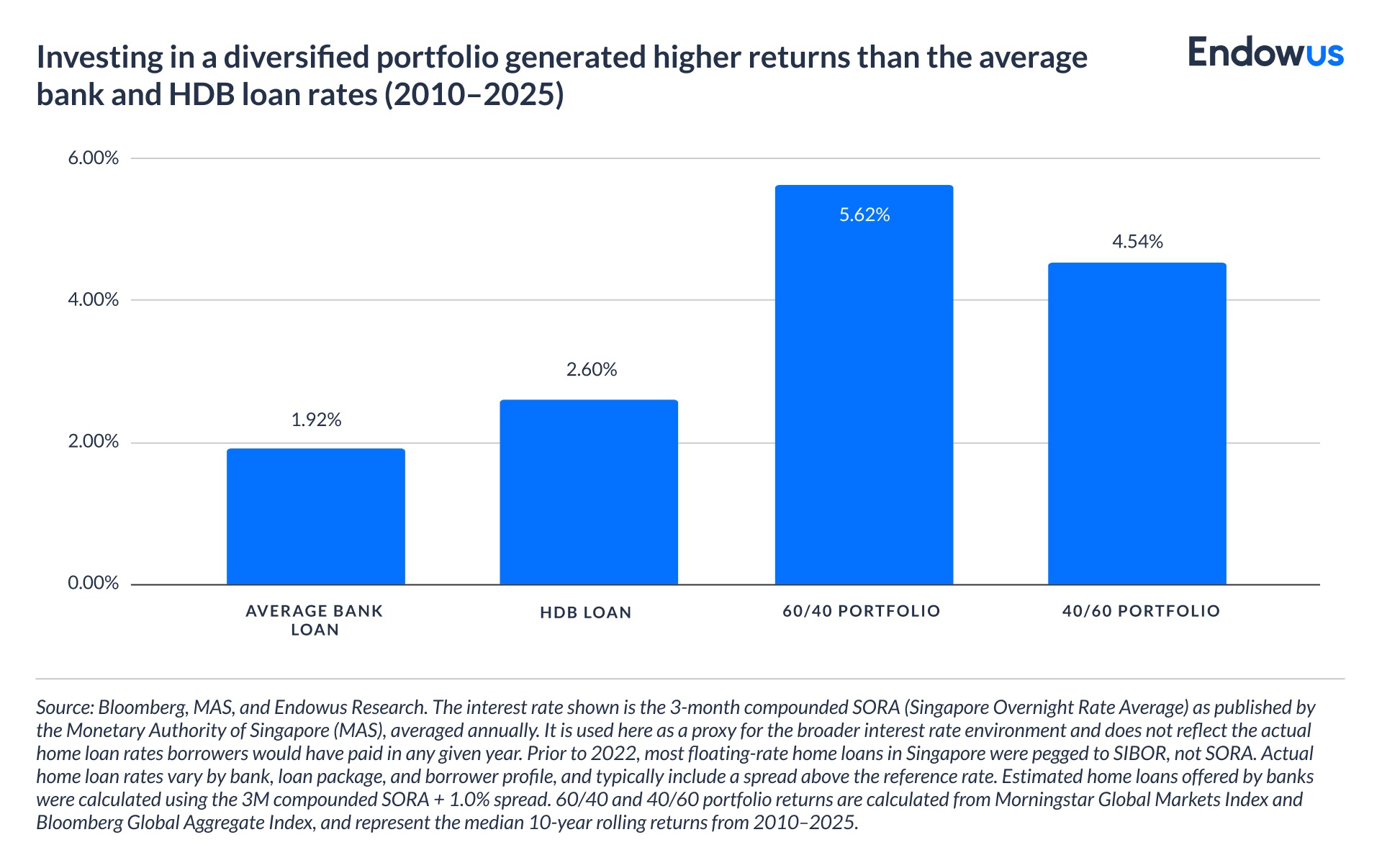

In the years between 2010 and 2025, the median 10-year rolling returns of a 60/40 portfolio is 5.62%, higher than HDB loan rate and estimated bank loan rates.

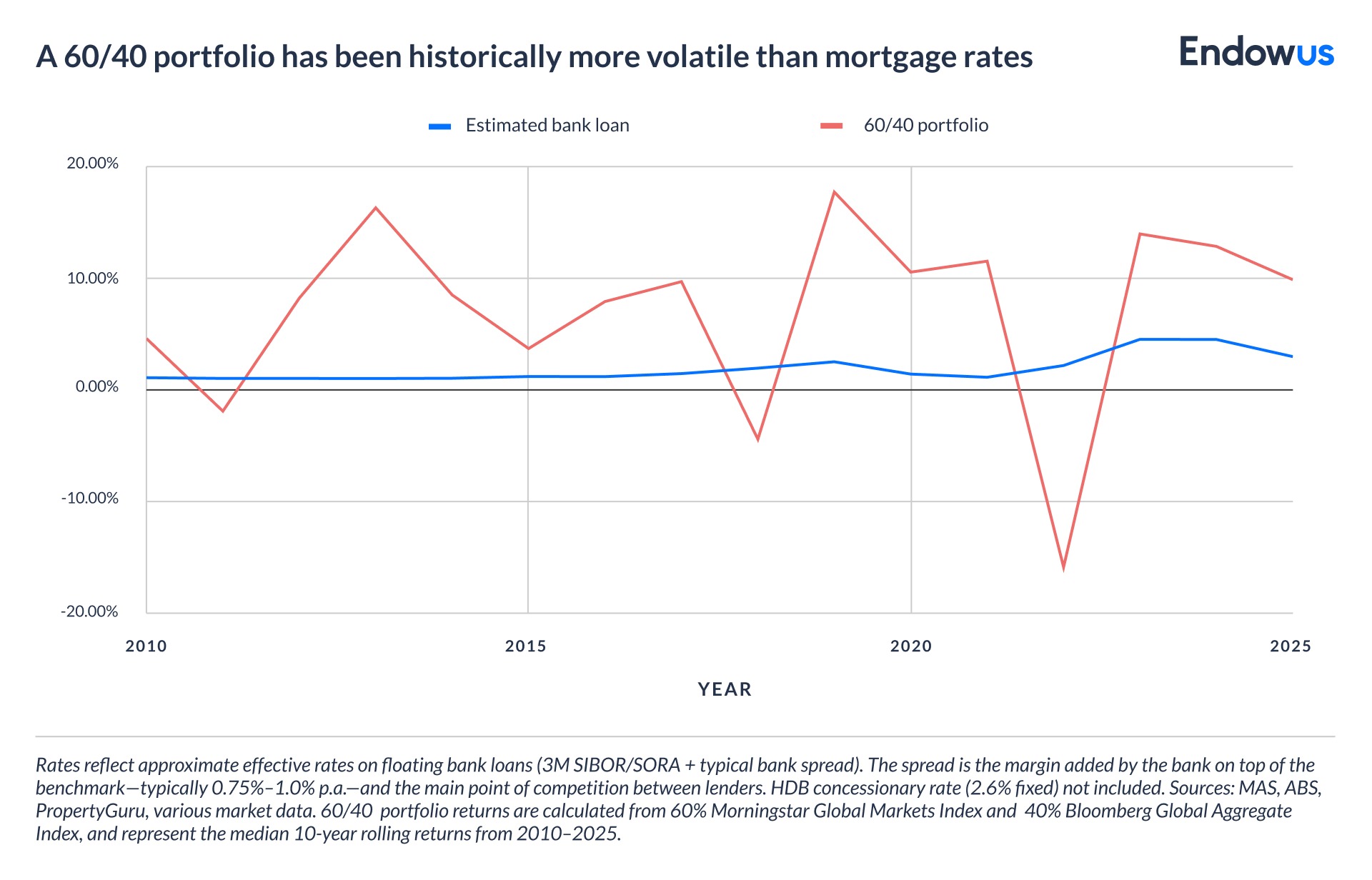

The comparison is less clear in higher-rate environments. When mortgage rates rise, the guaranteed return of prepayment approaches the risk-adjusted expected return of a balanced multi-asset portfolio—particularly when the investor's horizon is limited or their capacity to hold through drawdowns is uncertain.

In Singapore, the average 3-month compounded SORA moved from 0.16% in 2021 to 3.57% in 2023 before partially retracing. And the trade-off at close to 4.0% may change. Investors who deployed surplus capital into equities during the Dotcom crash in 2000 or Global Financial Crisis in 2008 experienced significant drawdowns before the long-run return assertion proved correct—a reminder that historical averages are not experienced uniformly.

What role does the interest rate environment play?

The mortgage rate is the single most important variable in this decision as it is typically less volatile than equity returns. It establishes some form of hurdle rate—the minimum expected return an investment must clear to justify choosing it over mortgage prepayment.

A useful framework: when the mortgage rate sits below approximately 3.0% to 3.5%, the expected long-run return of a globally diversified 60/40 portfolio has historically provided sufficient margin above the hurdle to favour investing—for most investors with a 10-year or longer horizon. When the rate exceeds 4.0% to 4.5%, the guaranteed return of prepayment is difficult to replicate on a risk-adjusted basis in fixed income markets. The decision then turns increasingly on equity allocation, horizon, and risk tolerance.

Variable-rate mortgages add complexity. An investor who chose to invest rather than prepay a 1.2% floating-rate mortgage in 2021 faced a very different decision two years later when that same rate had moved above 4.0% in 2023. For borrowers on floating rates, revisiting this decision periodically as the rate environment evolves is prudent, not a one-time call.

How do you decide? A framework by investor profile

The right allocation between mortgage prepayment and investment is a function of six variables. Two deserve particular emphasis.

Firstly, no allocation decision—prepayment or investment—should come before an adequate liquidity buffer is in place. Mortgage equity is illiquid; invested capital is subject to drawdown risk. Neither is a substitute for cash to cover near-term obligations.

Secondly, where an employer matches contributions to an occupational pension scheme, capturing the full match is the single highest-return decision available to most employees—an immediate 50% to 100% return on contributed capital. This takes priority over both prepayment and discretionary investment.

What about CPF and SRS in Singapore?

For Singaporean homeowners, the decision carries dimensions not present in most other markets. The Central Provident Fund (CPF) and Supplementary Retirement Scheme (SRS) both offer tax advantages that materially affect the investment side of the equation.

CPF Ordinary Account (OA) and your mortgage. CPF OA funds used for mortgage repayment accrue notional interest at the CPF OA rate—currently 2.5% per annum—which must be refunded with accrued interest upon property sale. This means using CPF OA funds to accelerate repayment does not eliminate the liability: it defers a portion of it. Homeowners who prepay using CPF OA balances may find their net property equity position less favourable than expected when they sell, depending on how the accrued CPF interest has compounded relative to property appreciation.

SRS and the tax advantage. SRS contributions receive immediate income tax relief at the contributor's marginal rate—effectively a guaranteed return equal to the tax saving in the year of contribution. For investors in higher income tax brackets, the after-tax return of an SRS contribution may exceed the mortgage interest rate before a single unit of investment return is generated. This makes SRS contributions a strong candidate for priority allocation before additional mortgage prepayment, subject to the annual contribution cap.

Why the mathematically optimal answer may not be the right one

The mathematical case for investing over prepayment appears robust across most rate environments and long horizons. The behavioural case is more nuanced.

Mortgage debt is visible, fixed, and emotionally salient in a way that portfolio returns are not. For some investors, carrying mortgage debt generates sufficient anxiety to impair their capacity to maintain an investment portfolio through drawdowns—leading to the worst of both outcomes: an underpaid mortgage and a portfolio sold at a loss.

Research on investor behaviour consistently finds that actual realised returns lag the returns of the vehicles investors hold, driven almost entirely by poorly timed entry and exit decisions. An investor who maintains consistent mortgage repayments and invests the remainder with genuine commitment to a long-term allocation is likely to accumulate more wealth than one who invests aggressively but sells during drawdowns or abandons the strategy when conditions deteriorate.

The relevant question is not which strategy is theoretically optimal. It is which strategy you will actually maintain through a 10% to 20% drawdown in your investment portfolio while continuing to service your mortgage. If the honest answer involves material uncertainty, a more conservative split—or a greater allocation to prepayment—may produce better real-world outcomes despite lower expected returns.

Investment implications

At Endowus, we view this decision through the same framework we apply to portfolio construction generally: match the allocation to the investor's actual circumstances, not to a theoretical optimum that assumes perfect behavioural consistency.

For most investors, the practical answer is a structured split: maintain standard mortgage repayments while investing a defined monthly amount consistently, and review the allocation when the rate environment changes materially. The worst outcome is not choosing the suboptimal strategy between the two—it is deferring both, holding capital in cash while waiting for the 'right moment' to decide, which is, in effect, a decision to earn a below-hurdle return on the full amount.

Frequently asked questions

As someone who is based in Singapore, should I prioritise paying off my mortgage or investing?

The answer depends on your mortgage rate, investment horizon, and risk tolerance. When mortgage rates are low (below ~3.0% to 3.5%), a 60/40 diversified portfolio has typically outperformed prepayment over long horizons (5.62% median 10-year rolling returns). When rates are high or your horizon is shorter, the guaranteed return of prepayment becomes more competitive. For most investors, a structured split between the two is more appropriate than an exclusive focus on either.

What is the break-even mortgage rate for investing instead?

There is no single break-even rate—it depends on the expected return and risk profile of the investment. As a general framework, rates below ~3.0% to 3.5% have historically favoured investing for investors with a 10-year or longer horizon. Above 4.0% to 4.5%, the guaranteed return of prepayment becomes increasingly competitive with the risk-adjusted expected return of most asset classes.

Should I use CPF OA to pay off my mortgage?

Using CPF Ordinary Account (OA) funds for mortgage repayment does not eliminate the liability. Upon property sale, the amount withdrawn plus accrued CPF OA interest (currently 2.5% per annum) must be refunded to the CPF account. Whether to use CPF OA funds for repayment or retain them for investment within the CPF system depends on the mortgage rate relative to the CPF OA rate and the available CPF investment options.

Should I contribute to SRS before paying off my mortgage?

For investors in higher income tax brackets, SRS contributions offer an immediate guaranteed return in the form of income tax relief at the marginal rate—which may exceed the mortgage interest rate before any investment return is generated. Subject to the annual contribution cap, SRS contributions are generally a strong priority allocation. Those SRS funds then need to be invested within the scheme to generate further returns.

What if I have other debts alongside my mortgage?

Credit card balances, personal loans, and other unsecured debt typically carry interest rates materially above residential mortgage rates—often 10% to 25% per annum. No investment strategy generates returns that reliably exceed these rates on a risk-adjusted basis. Eliminating high-cost unsecured debt takes priority over both mortgage prepayment and discretionary investment.

Why you should use your CPF to pay for your housing loan

Guide to using your CPF to buy housing

Webinar: Property outlook 2022 — Saving for your property and life goals

%20F1(2).webp)

.webp)

.webp)