.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Private infrastructure offers historically low correlation to both equities and bonds as well as spanning a meaningful risk spectrum—from predictable core income strategies to higher-conviction value-add and secondaries—giving investors flexibility in how they deploy capital.

- Three structural growth themes—decarbonisation, digitalisation, and urbanisation—provide durable long-term demand regardless of market cycles. In addition, for Asian investors, USD and EUR-denominated cash flows add a currency diversification benefit alongside portfolio resilience.

- Infrastructure should be treated as a long-term strategic allocation, not a tactical position. Illiquidity is the trade-off for income stability, inflation linkage, and lower correlation.

Infrastructure—the durable, essential assets that underpin modern economies—has become a compelling allocation for long-term investors. Investment in infrastructure offers contracted, regulated cashflow that is potentially insulated from short-term economic cycles.

For investors seeking to add a less volatile allocation to their portfolio, private infrastructure deserves some consideration. Here is why.

What is private infrastructure?

Private infrastructure encompasses investments in long-lived, essential assets—typically spanning energy, transport, and more so lately, digital infrastructure.

Exposure can be obtained through equity and debt. Infrastructure equity captures upside from asset growth and operational improvements. Infrastructure debt targets steady cash flows, benefiting from seniority in the capital structure and strong covenants. Both have historically exhibited low to negligible correlation with traditional asset classes.

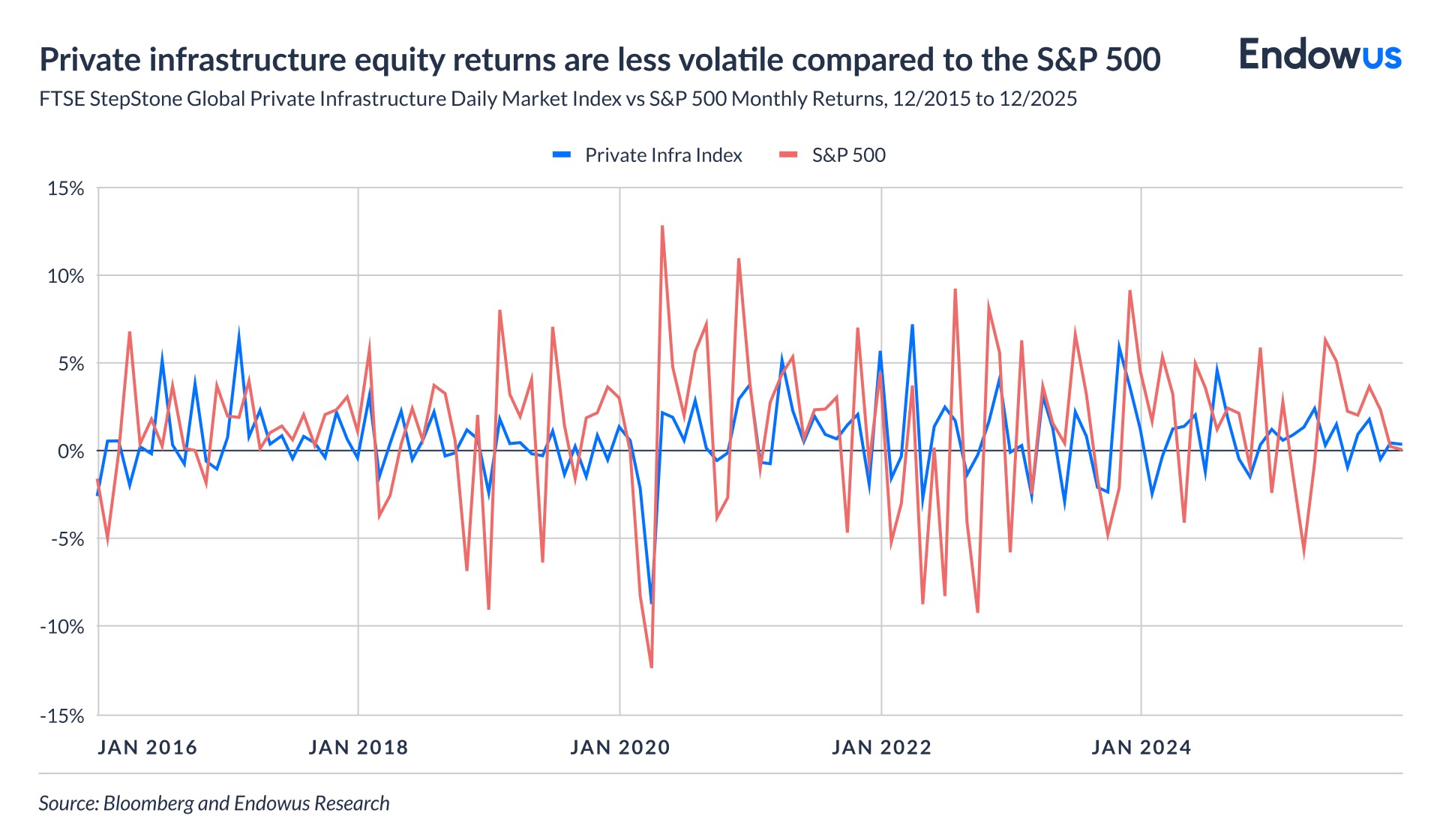

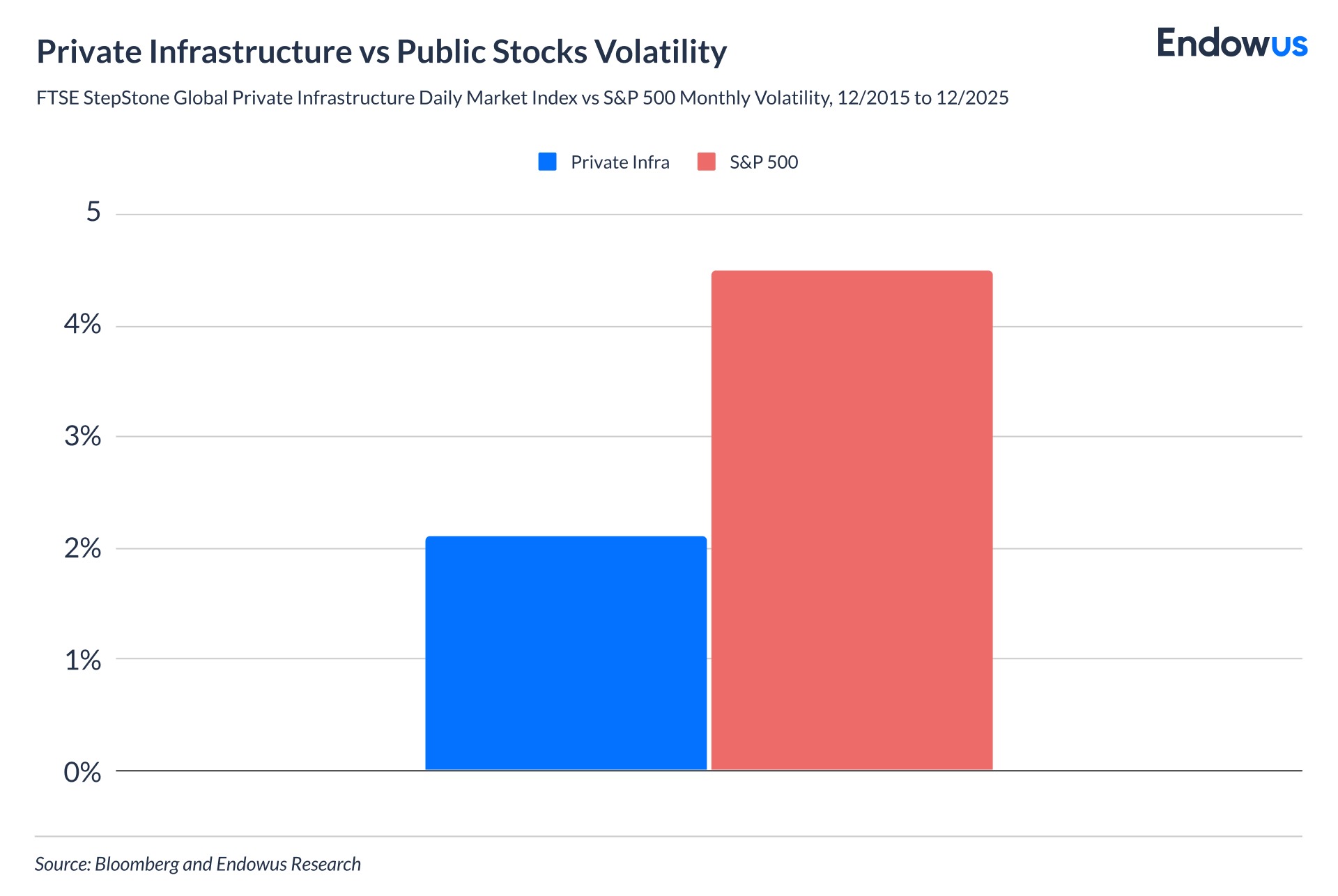

From 2007 to 2023, the Preqin infrastructure equity index recorded annual volatility of approximately 5.3%—roughly one-third that of the S&P 500. Over the same period, private infrastructure substantially outperformed listed infrastructure equity.

Infrastructure debt, in particular, has grown significantly over the past decade as a flexible financing tool supporting the clean energy transition and digital infrastructure build-out. Correlation between infrastructure debt and traditional fixed income has historically been close to zero, or negative, depending on the geography.

The portfolio case: Potential diversification benefits

Adding private infrastructure helps enhance portfolio resilience, potentially increasing risk-adjusted returns by reducing overall volatility.

This reflects the structural nature of infrastructure cash flows, which are linked to long-term contracts, regulated tariffs, or monopoly-like demand. Compared to private equity, infrastructure is also less dependent on multiple expansion, yield contribution to total return is higher, and reliance on exit markets is more limited. This makes it a fundamentally different risk exposure - complementing other alternatives allocations.

Understanding the risk spectrum within infrastructure

Infrastructure is not a single risk bucket. Risk and return profiles vary considerably depending on the sub-segment, and understanding this taxonomy is essential to portfolio construction.

Core and core-plus strategies focus on mature, essential assets with long-term contracted or regulated revenues, committed offtake, and built-in inflation hedging. These typically act as the anchor for any infrastructure allocation—dampening long-term volatility and delivering reliable income.

Value-add and opportunistic strategies target assets with higher complexity—development risk, construction exposure, or transition opportunities. Returns depend heavily on execution, but the upside potential is correspondingly greater. These strategies carry higher cyclicality and downside risk than core.

Secondaries provide a distinct role in the portfolio: they mitigate vintage risk and reduce the J-curve effect. Since secondary investments are already operational cash-flow-yielding assets, yield contribution is front-loaded and return profiles are more predictable. This characteristic tends to resonate well with investors prioritising capital preservation and earlier income distribution.

The most meaningful sources of mispriced risk in infrastructure sit within individual assets—in their regulatory regime, contracting structure, capital structure, and revenue model—rather than in external macro conditions. This is a critical distinction from public markets and much of traditional private equity.

Structural growth drivers

Infrastructure returns are underpinned by three long-term structural forces that are unlikely to reverse regardless of near-term macroeconomic conditions.

- Decarbonisation: the global energy transition is driving sustained capital deployment into renewable energy, grid modernisation, and clean transport infrastructure.

- Digitalisation: demand for data centres, fibre networks, and telecommunications infrastructure continues to accelerate. Note that data centre investment returns are facing increasing pressure as constraints around power availability and water usage become more binding—manager selection and asset-level analysis matter here.

- Urbanisation: growing and shifting urban populations require sustained investment in transport, utilities, and social infrastructure across both developed and emerging markets.

These drivers support long-term demand for infrastructure assets irrespective of short-term market cycles—reinforcing the strategic, rather than tactical, rationale for the asset class.

Why this matters for Asian investors

For investors based in Singapore and across Asia Pacific, private infrastructure offers an additional dimension of portfolio benefit: currency and geographic diversification.

Many infrastructure assets generate cash flows denominated in US dollars or euros, providing a natural hedge against home-currency concentration risk. This is particularly relevant for investors with significant Singapore dollar-denominated holdings or exposure to regional regulatory and political risk.

High-net-worth and ultra-high-net-worth (UHNW) investors globally are increasing their allocations to private markets. Broader industry surveys suggest that the primary motivations—income needs, inflation sensitivity, and portfolio resilience—are especially pronounced among Asian investors navigating a domestically more uncertain economic environment.

That said, while the appeal of potentially stable cashflows may feel especially compelling amid today's (April 2026) market volatility, private infrastructure is best understood as a strategic portfolio allocation—not a tactical response to shifting macro conditions. Its long investment horizon and inherent illiquidity are features of a long-term, well-diversified portfolio, not reasons to time an entry.

Investment implications

Private infrastructure belongs in the alternatives or real assets—less liquid—sleeve of a long-term portfolio, typically alongside private equity and private credit. Within that sleeve, it serves a distinct function: strategic diversification rather than return maximisation.

A well-constructed infrastructure allocation may provide:

- Inflation protection through contracted or regulated cash flows with built-in escalation mechanisms

- Income stability with bond-like characteristics, complementing equity risk elsewhere in the portfolio

- Diversified real-economy growth exposure across strategies (core to value-add), geographies, and asset types

- Portfolio resilience—lower volatility and reduced drawdown risk relative to public markets

The appropriate allocation will depend on individual risk tolerance, liquidity requirements, and time horizon. Given the long-dated and typically illiquid nature of infrastructure investments, its benefits compound over time, and its role in the portfolio should be sized accordingly.

Diversification across managers and vintages is also critical. In competitive sub-segments such as renewable energy and digital infrastructure, investor outcomes are heavily influenced by portfolio construction and - most importantly - manager selection.

Endowus offers access to a diversified infrastructure portfolio in Singapore for accredited investors through the Private Infrastructure Portfolio, which provides exposure to a broad range of infrastructure strategies—including core, core-plus, value-added, opportunistic, secondaries, and infrastructure debt—across developed markets in North America, Europe, and Asia-Pacific.

All direct investment GPs (Macquarie, EQT, KKR, Stonepeak and CIP) are ranked in the top 10 largest infrastructure fund managers by Infrastructure Investor, the world’s leading authority on private infrastructure markets.

Why are more family offices setting up in Singapore?

Webinar: Introduction to the art market

.jpg)

How alternative investments can fit into your portfolio

%20F1(2).webp)

.webp)

.webp)