.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Value investing is the practice of buying stocks that trade below their estimated intrinsic value—a discipline pioneered by Benjamin Graham in the 1930s and extended by Warren Buffett and Charlie Munger through their focus on durable business quality.

- Academic research, including the Fama–French (1992, 1993) factor models, shows that value stocks have historically delivered a return premium over growth stocks across multiple markets, though the premium can disappear for extended periods.

- Identifying undervalued stocks requires combining quantitative screening—using metrics such as P/E, P/B, and free cash flow yield—with a qualitative assessment of competitive position, management quality, and balance sheet strength.

Most investors intuitively understand that identifying a dislocation—a mismatch between the price of an asset and its underlying worth—is the foundation of successful investing. Benjamin Graham formalised this common-sense idea into a rigorous investment philosophy in the 1930s, one that has since produced some of the most compelling long-term track records in market history, including those of Warren Buffett and Charlie Munger at Berkshire Hathaway.

Value investing is the discipline of estimating the intrinsic value of a business and purchasing its stock only when the market price offers a meaningful discount—what Graham called the margin of safety. The approach asks investors to think like business owners.

This article explains how value investing works, where it comes from, what the evidence says about its long-run returns, and how professional investors can apply its principles to find undervalued stocks.

What is value investing, and where did it come from?

Once we’ve established that investors screen equities to find attractive opportunities, we should add that the end goal for them is to generate returns as the market price converges toward that value over time.

The intellectual foundation of value investing rests on two books by Benjamin Graham, a Columbia Business School professor who later taught Warren Buffett. Security Analysis (1934, co-authored with David Dodd) laid the theoretical groundwork: it argued that securities had an objective, calculable worth—derived from earnings, assets, and cash flows—and that market prices frequently deviated from this worth due to investor emotion. Graham's later book, The Intelligent Investor (1949), distilled these ideas for a general audience.

"The intelligent investor is a realist who sells to optimists and buys from pessimists."

—Ben Graham, The Intelligent Investor (1949)

Graham's central concept was the margin of safety: the difference between a stock's estimated intrinsic value and its current market price. If a company is worth S$100 per share and trades at S$65, the investor has a 35% margin of safety—a cushion against errors in the valuation estimate, unexpected business deterioration, or simply bad luck. Graham wrote that the margin of safety was, in three words, the secret of sound investment.

Warren Buffett trained under Graham at Columbia and began his career as a strict adherent of the statistical approach—buying deeply discounted stocks regardless of business quality. Charlie Munger later shifted Buffett's thinking toward what might be called quality-at-fair-price investing: the idea that a wonderful business purchased at a reasonable price was worth more than a mediocre business purchased at a bargain price. Buffett has credited Munger directly: "Charlie shoved me in the direction of not just buying bargains, as Ben Graham had taught me." This evolution reflects a broader tension within the value investing tradition between deep value (statistical cheapness) and quality value (durable competitive advantage at a reasonable price).

What does the evidence say about long-term value investing returns?

The empirical case for value investing is well-established.

The most rigorous academic evidence that “value” is a premium comes from Eugene Fama and Kenneth French, whose 1992 and 1993 papers demonstrated that stocks with low price-to-book (P/B) ratios had historically delivered higher returns than stocks with high P/B ratios across US markets and, subsequently, internationally. This value premium—the return advantage of cheap stocks over expensive ones—became one of the foundational pillars of factor investing.

The debate about why the value premium exists is unresolved. Fama and French attributed it to risk compensation: value stocks are typically companies in financial difficulty, and investors demand higher returns to hold them1. Lakonishok, Shleifer, and Vishny (1994) offered an alternative explanation: behavioural biases lead investors to systematically overpay for glamour stocks and underpay for unglamorous ones, creating a persistent mispricing that disciplined investors can exploit.

Analysis of the value factor from 1926 to 2020 also found that positive value factor returns were closely linked to declining stock market volatility—suggesting that risk sentiment, not just valuation, plays a meaningful role in when the premium materialises. Separately, CFA Institute research on factor time horizons found that the value factor becomes more attractive over longer investment horizons, consistent with the view that value investing rewards patience. This specific topic was also touched upon at a recent event in Hong Kong, in the conversation between Dimensional Fund Advisors co-CIO Savina Rizova and Endowus CIO Hugh Chung.

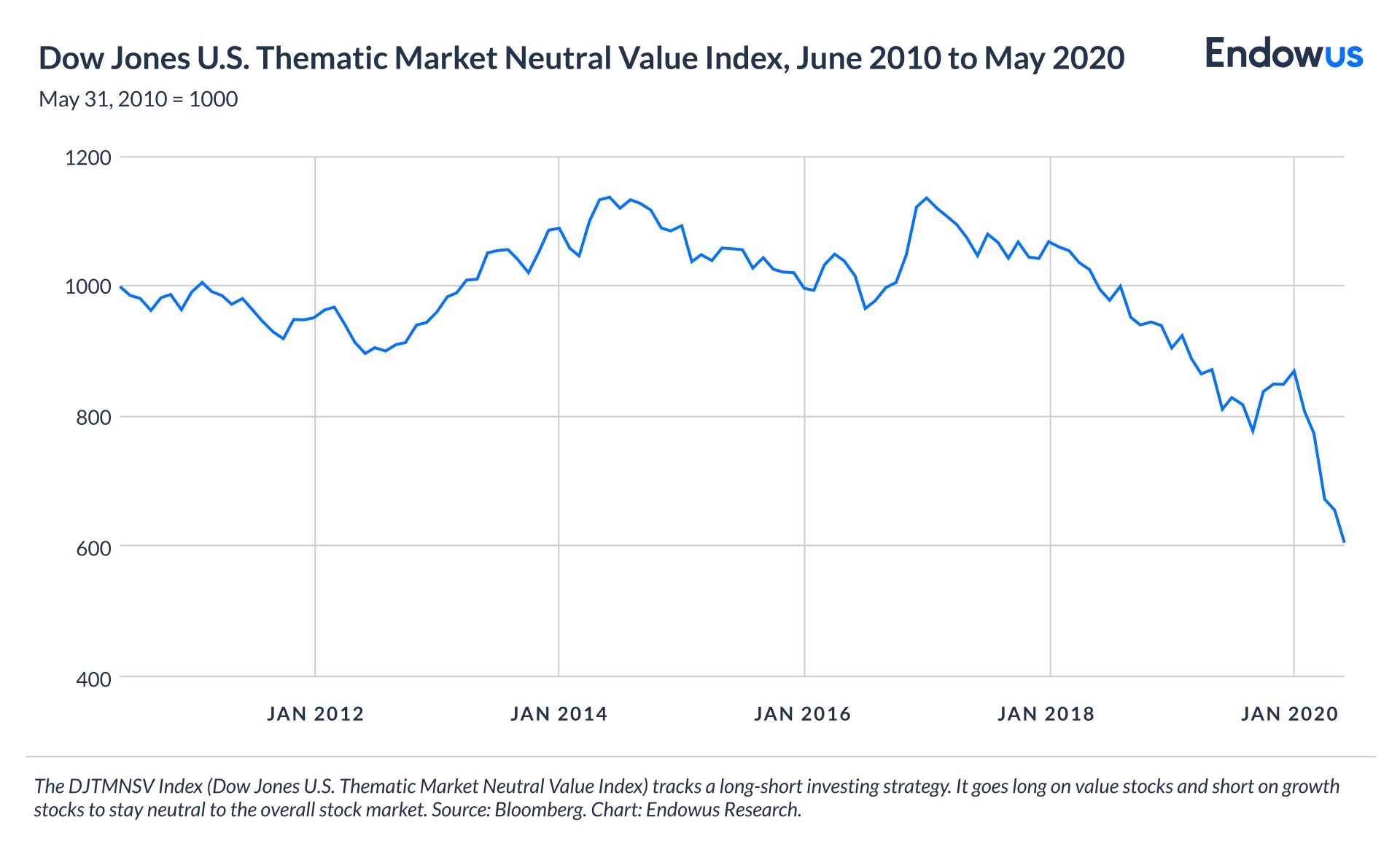

The value premium has, however, been subject to extended periods of underperformance. The decade from 2010 to 2020 (see chart further below in this article) was particularly challenging for traditional value strategies in the US, as technology and growth companies—often trading at high multiples—substantially outperformed the broad market. This does not invalidate the long-run evidence, but it does confirm that investors applying value principles must be prepared for multi-year periods when the market does not reward the approach.

Key valuation metrics used in value investing

How do you find undervalued stocks?

Finding undervalued stocks is typically a two-stage process: quantitative screening to identify candidates, followed by qualitative analysis to determine which candidates are genuinely undervalued rather than cheap for good reason.

The first stage involves filtering the investable universe using valuation metrics—typically P/E, P/B, free cash flow yield, and EV/EBITDA—to identify stocks that trade at significant discounts to their sector or historical averages. Graham's original framework emphasised selecting stocks trading below their net current asset value (current assets minus total liabilities), which in today's market requires a very wide screen and typically returns only deeply distressed companies. A more practical modern application screens for stocks in the bottom quartile of valuation within their sector peer group.

The second stage is qualitative. A stock that screens as cheap may be cheap for structural reasons: declining revenues, rising debt, competitive disruption, or poor capital allocation by management. Charlie Munger's lasting contribution to value investing was the emphasis on business quality—what Buffett later popularised as the “economic moat,” a durable competitive advantage that protects a company's earnings from being eroded by competitors. A cheap stock without a moat is not a value investment; it is defined as a value trap.

Practical indicators of a moat include brand pricing power (how the brand name is able to command a higher price), customer switching costs (how difficult it is for customers to move to a competitor), network effects (how a product or service becomes more valuable as more people use it), cost advantages from scale, and regulatory barriers to entry. Investors should also assess whether a company will still be competitively relevant in five to ten years before concluding that a low valuation represents a genuine opportunity rather than a structural discount.

Balance sheet strength matters equally. Graham was insistent that value investors should own companies with sufficient financial resources to survive adverse conditions. A company trading at a low P/E multiple but carrying substantial debt is in a different risk category from one with net cash. The margin of safety concept applies not only to the price paid but also to the business's capacity to endure adversity.

What makes value investing challenging in practice?

The gap between value investing as a principle and value investing as a practice is significant. Several structural challenges require careful attention.

The first is the abovementioned value trap. Distinguishing genuine mispricing from structural decline requires substantial analytical discipline and strong research ability. Errors are common even among experienced investors.

The second is patience. Merton Miller, the economist, once observed that markets can remain irrational longer than investors can remain solvent. Even when an analysis of intrinsic value is correct, there is no guarantee of when—or even whether—the market will close the gap.

The third challenge is information quality. Valuation metrics based on reported financial statements depend on the integrity of those statements. For investors in markets where accounting standards vary, applying extra scrutiny to reported earnings, debt levels, and cash flow conversion is essential.

Finally, concentration risk deserves attention. Classic value investing, in the Graham tradition, involves concentrated positions in a relatively small number of stocks, on the basis that diversification across many mediocre ideas dilutes the return advantage of the best ones. Charlie Munger, for instance, ran highly concentrated portfolios. Concentrated value investing can amplify both gains and losses, and is generally more suitable for investors with sufficient analytical resources to conduct deep due diligence on each holding.

How does value investing apply to investors in Singapore?

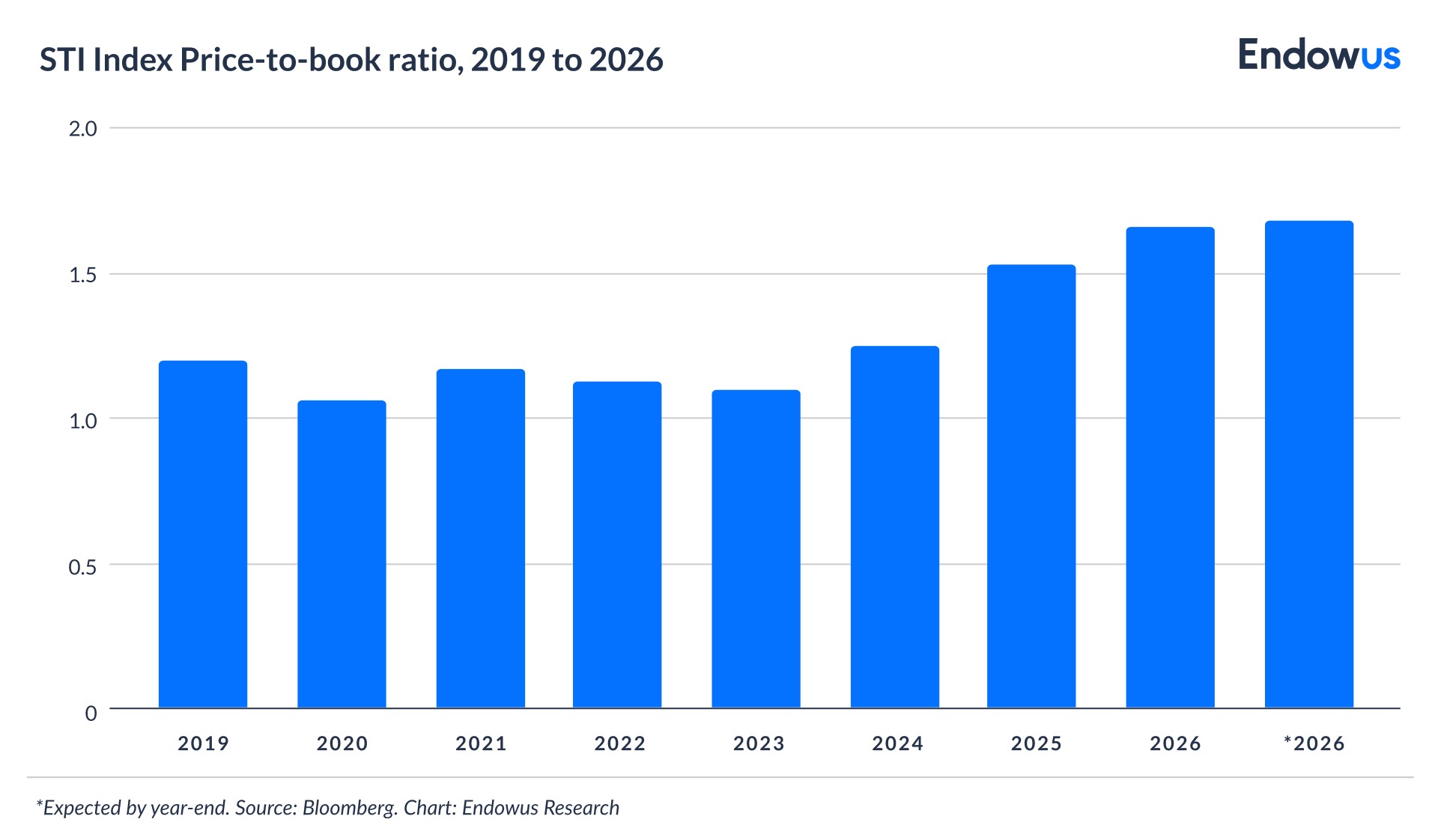

Singapore-listed stocks, particularly in the financial, property, and industrial sectors, have historically traded at lower valuations than their counterparts in the United States. The Straits Times Index (STI) has often carried a P/B ratio well below 1.5—partly reflecting the composition of the index, which skews heavily toward banks, real estate investment trusts (REITs), and property developers. This structural discount meant that Singapore investors had, in principle, a larger universe of potentially value stocks to examine. However, a broader re-rating is happening in Singapore-listed equities since the government launched the EQDP program.

However, the same caveats apply. A bank trading at 0.8 times book may reflect genuine undervaluation, or it may reflect legitimate concerns about loan book quality, net interest margin compression, or regulatory capital requirements. A REIT trading at a discount to net asset value may be cheap because interest rates are rising and distribution yields have compressed, or because the underlying property portfolio faces structural headwinds. Value investing requires sector-specific understanding, not just index-level screening.

For most individual investors, gaining value exposure through a diversified fund—one that applies systematic value screening across a broad universe of stocks—is a more practical approach than individual stock selection. Diversification reduces the risk of any single value trap materialising into a large portfolio loss, while still providing meaningful exposure to the long-run value premium identified in the academic literature.

Endowus Factor Portfolios offer value factor exposure through its fund selection. For investors who want to tilt their equity portfolio toward value characteristics without concentrating in individual stocks, this approach allows participation in the factor premium while maintaining portfolio diversification.

Investment implications

Value investing is one of the most thoroughly researched investment strategies in finance, with an evidence base spanning nearly a century. The margin of safety concept—buying stocks at a meaningful discount to intrinsic value—remains intellectually sound, and the long-run return premium for value stocks relative to growth stocks is well-documented.

In our view, the most practical lesson from Graham, Buffett, and Munger is not a specific screening formula but a way of thinking: that price and value are different things, that markets misprice assets because of emotion and institutional constraints, and that patient investors (patience being the keyword here) who exploit these gaps—while insisting on financial quality and reasonable margins of safety—may be rewarded over time.

Retail investors should know, however, that they lack the resources to conduct the kind of thorough fundamental research that would allow them to capture the value premium. And even if they could identify a single opportunity—which is highly unlikely in the first place—they would not be able to do so at the scale needed to build a diversified portfolio. Instead, they are better off trusting their professional advisor to build a value-tilted allocation to broadly diversified global equity—either through multiple factor-based funds or a single one with a high number of well-researched individual holdings.

At Endowus, our advisers understand how value factor exposure can complement your overall portfolio strategy.

Frequently asked questions about value investing

What is value investing?

Value investing is the practice of buying stocks that trade below their estimated intrinsic value—the underlying worth of a business based on its earnings, assets, and cash flows. The core idea, developed by Benjamin Graham, is that market prices frequently deviate from intrinsic value, creating opportunities for disciplined investors.

What is the margin of safety in value investing?

The margin of safety is the difference between a stock's estimated intrinsic value and its current market price. Buying at a significant discount provides a buffer against valuation errors, unexpected business deterioration, or adverse market conditions. Graham described it as the central concept of sound investment.

Does value investing work over the long term?

Academic evidence, including the Fama–French factor models, supports the existence of a long-run value premium—the tendency of cheap stocks to outperform expensive ones over time. However, the premium can be absent for extended periods, and value strategies require patience and a multi-year investment horizon.

What is the difference between value investing and growth investing?

Value investing focuses on buying stocks at prices below estimated intrinsic value, typically identified by low P/E, P/B, or other valuation metrics. Growth investing focuses on companies with high expected earnings growth, which are typically priced at premium multiples. The two approaches are not mutually exclusive: Buffett's quality-at-fair-price philosophy incorporates some elements of both. In fact, in his portfolio, Buffett included value companies such as Coca-Cola and Chevron, alongside companies that could fit in a growth portfolio (Apple).

How can I start value investing in Singapore?

You should not do it yourself. Value investing is a professional investment strategy that requires large resources in both manpower and time. For investors who want to incorporate a value tilt into their equity allocation, an Endowus adviser can help assess which approach suits your risk profile, investment horizon, and existing portfolio—and implement it as part of a coordinated strategy across your full wealth picture.

1Fama, E.F. & French, K.R. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427–465.

Webinar: Investing in a better future: Through the lens of an equity investor

Why ESG investing should matter to Singaporeans

When you can’t see the forest for the trees: A holistic approach to asset allocation

%20F1(2).webp)

.webp)

.webp)