.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

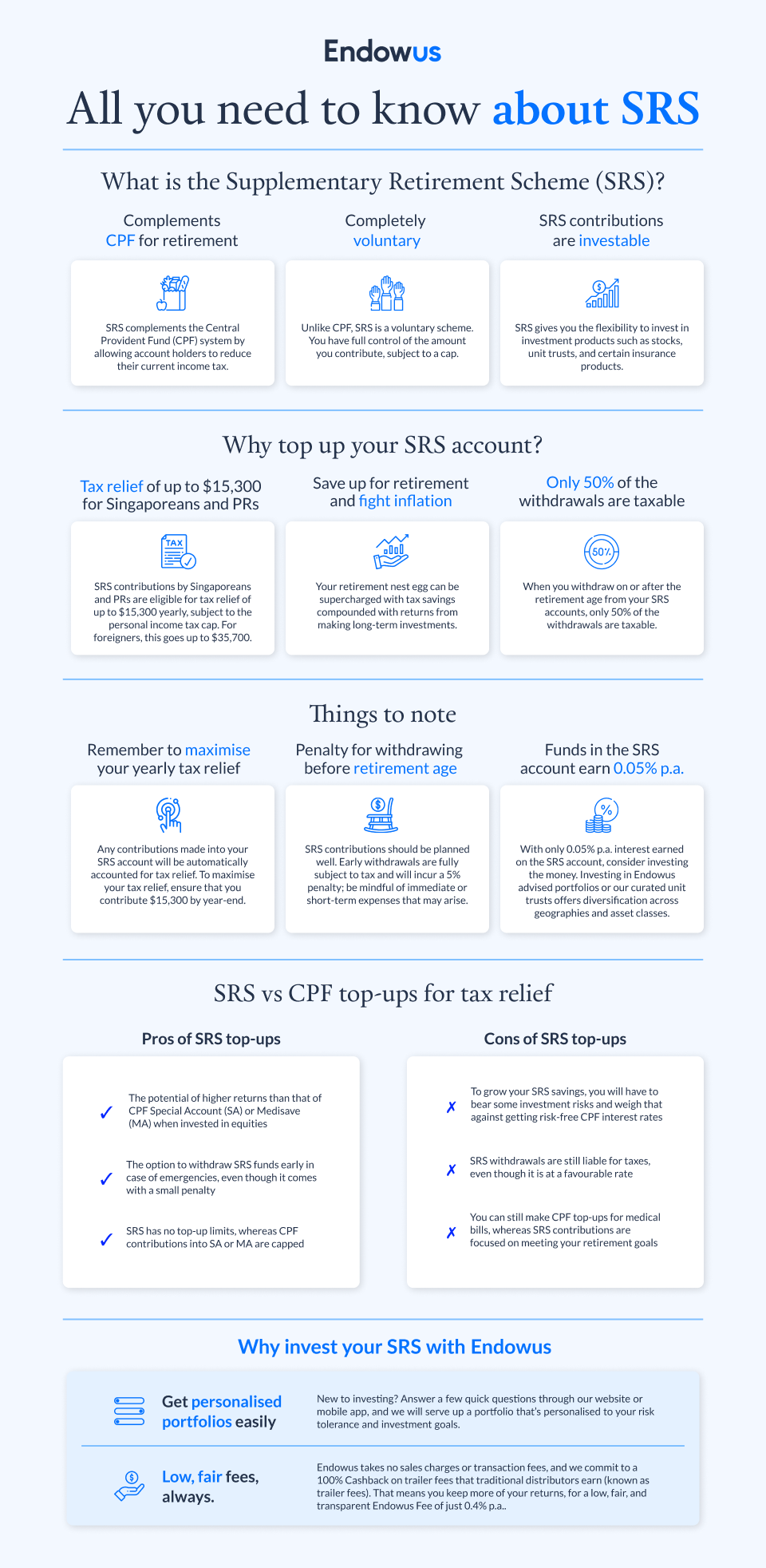

The annual Supplementary Retirement Scheme (SRS) top-up deadline on 31 December is one to mark on our calendars because of the tax perks and the retirement benefits that come with the scheme. Investors can automate their monthly SRS investments so every dollar is optimised to grow to meet long-term needs.

The original version of this article first appeared in The Business Times. This article has been updated to reflect the latest statistics and information, as of 3 Oct 2025.

These days, it takes little effort to remember deadlines when it comes to splashing out on good deals. Black Friday, 10.10, 11.11, and 12.12 — these are some dates and times that we’ve learnt to prepare for, to take advantage of discounts off items on our shopping list.

Just as well that as we move closer to Christmas and the end of 2022, now is a jolly good time to stuff the proverbial stockings with discounted purchases. But remember, too, that this season is also associated with an annual tax saving and investing hack. It offers a discount off your tax bill each year and allows you to grow your retirement savings for the long term.

This offer is called the Supplementary Retirement Scheme (SRS). Not only is the scheme an optimal way to save more for your retirement, it is also a nifty hack to lower your tax bill today — whether you are Singaporean, a permanent resident (PR) or a foreigner working here.

Unwrapping SRS

There are two parts to this tax incentive. SRS allows us to postpone how much we should pay on our tax bill now. It also allows you to pay less tax later in your retirement years.

If we manage how much we withdraw from the SRS account each month for our spending needs at retirement, we can even withdraw without paying taxes on these sums annually.

Every year, every Singaporean is allowed to set aside up to $15,300 in an SRS account, with the top-up deadline falling on 31 December of each year. When done so, $15,300 will be deducted from personal income, which translates to tax savings on the current tax bill.

To be clear, to continue enjoying this tax deferment, the money must remain locked in the SRS account until the account holder’s relevant retirement age. If the money is taken out ahead of that time, you will have to pay full taxes on the sum withdrawn, and pay an additional 5% penalty on that amount.

The government will void penalties for exceptional cases, such as on medical grounds.

When we hit the retirement age — set in the year we had put in our first dollar into our SRS account — we can start withdrawing from the account without incurring a penalty. At retirement, tax is payable on just half of the withdrawals.

Because the first $20,000 of chargeable income is not taxed in Singapore, we can effectively withdraw $40,000 ($20,000 multiplied by two) each year tax-free for your retirement spending, or roughly $3,330 to $3,340 a month. This assumes the taxpayer has no other source of taxable income. Even if we would like to withdraw more than $40,000 annually in subsequent years, the tax concession means we will only be charged taxes on half of the withdrawal amount, making such retirement savings highly tax efficient.

Use our SRS calculator to better understand your tax savings under the scheme.

Expats can apply too

Foreigners have a higher SRS contribution limit of $35,700 in the absence of tax relief from CPF contributions.

There are some specifications to note. Foreigners are allowed to withdraw penalty-free before their retirement age, but only if i) the SRS savings are withdrawn 10 years from the date of the first SRS contribution; ii) the SRS savings are withdrawn in full; and iii) they are neither a Singapore citizen nor a Singapore PR on the date of withdrawal and for a continuous period of 10 years preceding the date of withdrawal.

Check the tax rate based on the residency status at the point of withdrawal and the details behind withholding tax, a tax credit that will be used to offset the actual tax liability.

With inflation, holding cash can make retirement harder

The second annual edition of the Endowus Retirement Report showed that high inflation is exposing widening gaps in retirement adequacy in Singapore. In particular, there was a sharp drop in confidence among those in the mid-high income brackets.

Against that backdrop, data from the Ministry of Finance showed that of the $20.6 billion held in SRS accounts as of December 2024, 19% was held in cash. This is even though cash savings in SRS accounts earn just 0.05% interest per annum.

Given high inflation right now, the funds may be taxed less in the future, but cash loses its purchasing power if it sits idle in the account.

An increase in long-term inflation from 1% to 3% will mean a 45.8% fall in retirement savings in real terms. Under such conditions, banking on Black Friday deals and furiously saving alone are unlikely to yield a comfortable retirement.

Savings in the SRS account can be invested in unit trusts, government bonds, shares, and insurance, among other things. Investors can automate their monthly SRS investments so every dollar saved in their SRS account is optimised to grow to meet long-term needs. This way, investors can ride through the ups and downs of market volatility in a disciplined way to enjoy the compounded gains in the decades to come.

But don’t forget to check off that grown-up Christmas list: Honour the year-end deadline for SRS top-ups, and take steps to make investing more than a seasonal affair. You will thank yourself later for that astute planning.

More resources on SRS

Curious to learn more? Pick up tips to optimise your SRS savings and supercharge your retirement plan.

- Your guide to the Supplementary Retirement Scheme (SRS)

- What are the best SRS investment options available?

- Six myths about the Supplementary Retirement Scheme (SRS)

- How to reduce your income tax through CPF and SRS top-ups

- Webinar: Planning for retirement and tax relief despite record inflation

To start investing your SRS money in best-in-class funds with Endowus, follow this link. If you're new to Endowus, you can join us by creating an account here.

Should a new Singapore Permanent Resident make voluntary contributions to CPF accounts?

Understanding the different returns for CPF SA through a MCQ question

Webinar: Tax hacks: Pay less tax with CPF & SRS top-ups

%20F1(2).webp)

.webp)

.webp)