.webp)

.webp)

.webp)

.webp)

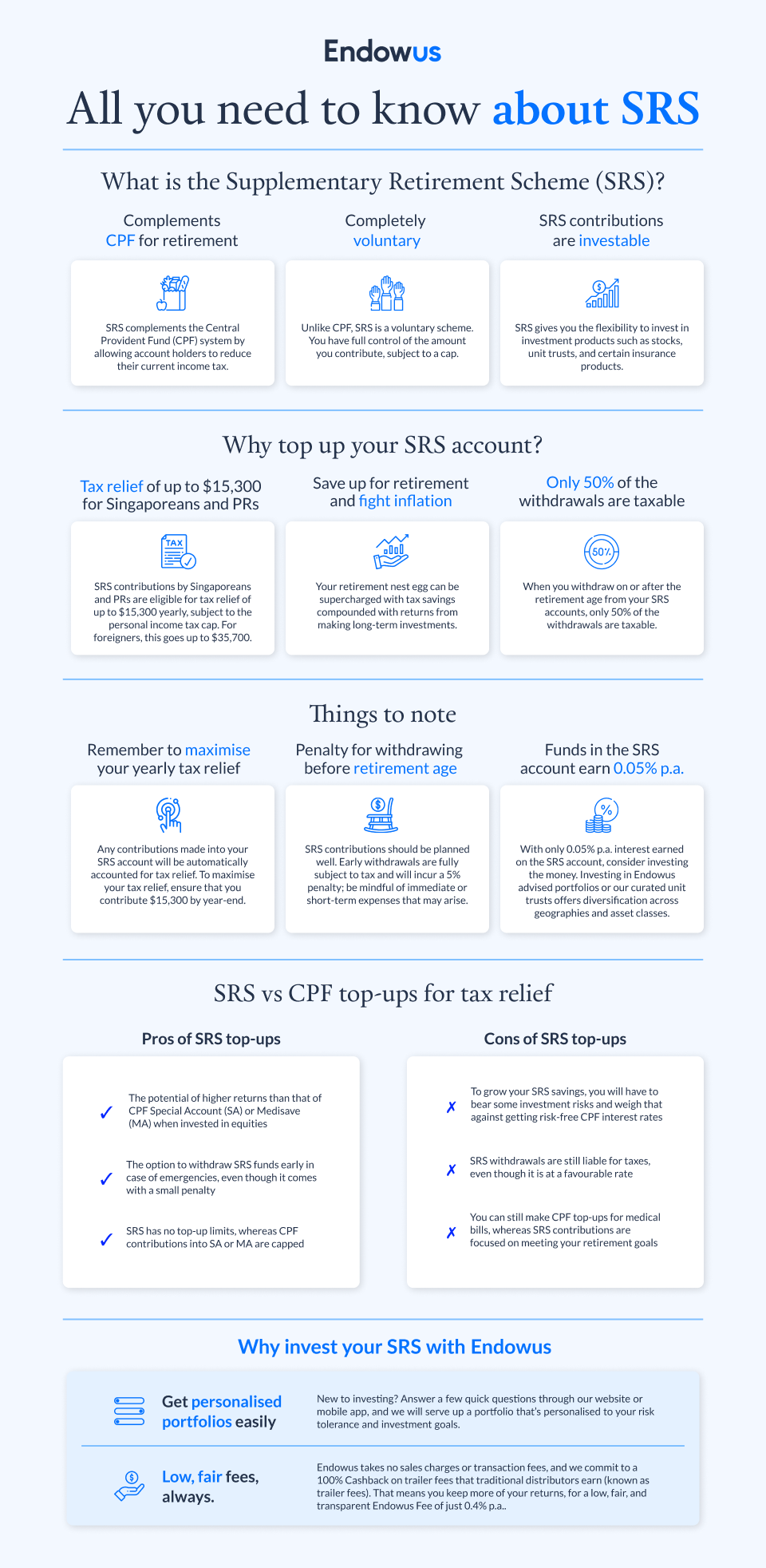

Most of us living in Singapore are familiar with CPF — it's where a large portion of our pay cheque goes every month. But we may not be as familiar with the Supplementary Retirement Scheme (SRS).

Unlike our CPF, a mandatory social security savings scheme, participation in the SRS is voluntary. SRS is designed to complement our CPF savings, which are meant for housing, medical, and basic income needs in retirement.

One of the main reasons why Singaporeans choose to open an SRS account is for tax relief. Singaporeans and PRs can contribute up to $15,300 to their SRS accounts each year, and foreigners can contribute up to $35,700. These contributions are tax-exempt.

Also, it's important to note that SRS tax benefits are on top of your CPF top-up tax relief. You can read more here about whether you should invest for retirement using your SRS savings.

Here are six myths you may have heard and believed about SRS accounts.

Myth #1: SRS is only for Singaporeans

All Singaporeans, Permanent Residents and foreigners living in Singapore can open an SRS account. The only requirements are that you must be at least 18 years old and are not an undischarged bankrupt.

You can start contributing to your SRS the moment you open an SRS account, as long as you earn any income (including directors' fees) in the current year. You can contribute to the SRS up to any age until you make the first withdrawal from your SRS account.

Myth #2: SRS is part of the CPF system

SRS is not part of your CPF — it is a voluntary scheme that complements your CPF savings for retirement. You can contribute any amount to your SRS accounts and as many times as you wish within the year, subject up to a maximum contribution cap of $15,300 for Singaporeans and PRs, and $35,700 for foreigners per year.

The three local banks (DBS, OCBC, UOB) are the appointed SRS operators, and SRS is administered by the Inland Revenue Authority of Singapore (IRAS).

Read more: Should you invest for retirement using your SRS account?

Myth #3: You can have multiple SRS accounts

Unlike brokerage accounts, you can only have one SRS account at any time. It's actually an offence to open SRS accounts with more than one operator, and there are penalties involved.To start contributing to SRS, you must first open an SRS account with one of the three localbanks (DBS, OCBC, UOB).

You can invest your SRS savings through wealth advisory platforms such as Endowus and different brokerages, but with a a single SRS account number.

If you previously had an SRS account but then closed it, you will also not be permitted to open a new account.

Myth #4: SRS funds are locked away until the SRS retirement age

Unlike CPF, your SRS funds and monies aren't locked up. You can withdraw funds from your SRS account at any time before retirement, although this will be subject to a withdrawal penalty of 5%, and 100% of the withdrawal amount will be taxable.

This gives investors a liquidity option if they need to use the funds in their SRS account. Although you should consider whether you require the funds in the short term before contributing to your SRS account because premature withdrawals can leave you paying more in withdrawal penalties and taxes than you initially intended.

There are a few specific scenarios where you can withdraw your money from the SRS account with no penalty imposed, such as withdrawal on medical grounds or terminal illness, and 50% of the amount withdrawn will be subject to tax, with specific exemptions. Foreigners (non-PRs) can also withdraw in one lump sum with no penalty if they have maintained the SRS account for at least 10 years from the date of the first contribution, and 50% of the withdrawal amount will be taxable.

Myth #5: Only you can contribute to your SRS

Your employer can also contribute to your SRS on your behalf, provided that you have given them written instruction or authorisation. For foreigners working in Singapore, this can be an excellent alternative to corporate pension plans or CPF schemes reserved only for Singaporeans and PRs.

An employer's contribution to your SRS account will be considered part of your remuneration, which is taxable. Based on the information provided by the SRS operator, you will then be given tax relief for such contributions in the subsequent year of assessment.

Myth #6: Your SRS withdrawals must be in cash

The funds in your SRS account can be withdrawn in two ways: in cash and in the form of investments that go directly to your Central Depository (CDP) account, or your brokerage account for unit trusts. This means that you won't need to liquidate your SRS investments when you withdraw and incur transaction costs. You can only withdraw your SRS in the form of investments under a few scenarios that qualify for the 50% tax concession:

- Withdrawal on or after statutory retirement age;

- Withdrawal on medical grounds;

- Withdrawal in full by a foreigner, if he or she is neither a Singapore citizen nor PR on the date of withdrawal and 10 years preceding and has maintained his or her SRS account for at least 10 years from the date of the first contribution.

Premature withdrawals must be made in cash, and the investments must be liquidated before the sale proceeds are withdrawn in cash from the SRS account.

To get started with Endowus SRS investing, click here.

Next on the Endowus Fin.Lit Academy

Read the next article in the curriculum: What are the best SRS investment options available?

%20F1(2).webp)

%20(1).gif)

.webp)

.webp)