.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Dollar-cost averaging (DCA) is a disciplined investment approach that reduces exposure to entry-point timing risk by deploying capital in fixed periodic instalments rather than all at once.

- Research consistently shows that lump-sum investing outperforms DCA over the long run in rising markets. On the other hand, DCA tends to deliver better outcomes when markets are volatile, when capital is accumulated gradually through income, or when an investor’s behavioural tolerance for near-term drawdowns is limited.

- The most important function of DCA is not return optimisation. It is behavioural: a structured approach that keeps investors in the market through periods of uncertainty rather than deferring deployment indefinitely.

Dollar-cost averaging (DCA) is one of the most widely recommended strategies in personal finance—and one of the most frequently misunderstood. Its advocates position it as an antidote to market timing risk. Its critics note, correctly, that it produces lower expected returns than deploying capital immediately in a rising market.

Both observations are true—investing outcomes are a function of both market conditions and investor behaviour. Most people think that they are rational, until the chaos starts. Swift downturns and speculative frenzies have a way of overwhelming logic, which is what makes DCA, a strategy that takes emotions out of the equation, enduringly relevant, and worth understanding.

This article looks at when DCA is likely to produce better investment outcomes than lump-sum investing, when it does not, and why its greatest value of keeping investors invested is itself a form of return optimisation strategy.

What is DCA, and how does it work?

DCA is the practice of investing a fixed sum at regular intervals—monthly, quarterly, or otherwise—regardless of prevailing market conditions. Because the investment amount is fixed, the same capital acquires more units when prices are lower and fewer when prices are higher. Over time, this produces an average cost per unit that is lower than the simple average of the prices at which purchases were made—a mathematical property sometimes described as the benefit of purchasing more when valuations are depressed.

The mechanics are straightforward. An investor who deploys S$1,000 per month into a broad equity index exchange-traded fund (ETF) for 12 months will accumulate units at different valuations throughout the year. In months where the index declines, the same S$1,000 acquires proportionally more units. In months where the index advances, it acquires fewer. The investor does not need to form a view on whether the market is overvalued or likely to correct, stripping away another layer of decision-making.

When does DCA work best?

DCA is most likely to add value relative to a lump-sum deployment in three distinct situations.

The first is when capital is not available as a lump sum. For salaried investors, DCA aligns naturally with how capital accumulates—cash is paid monthly, which makes it practical to deploy at regular intervals. Lump-sum investing may be more relevant when there is a windfall or a bonus. In this context, the relevant discipline is ensuring that available capital is deployed consistently rather than allowed to accumulate in cash pending a more favourable entry point.

The second is during periods of elevated volatility or sustained market drawdowns. When an investor deploys capital across a falling market, the average cost of acquisition declines as prices fall. If the market subsequently recovers, the lower average cost produces a materially better outcome than a single entry at the pre-drawdown level. This is the scenario in which DCA’s mathematical properties are most favourable, but it is also the scenario that most investors find psychologically most difficult to execute.

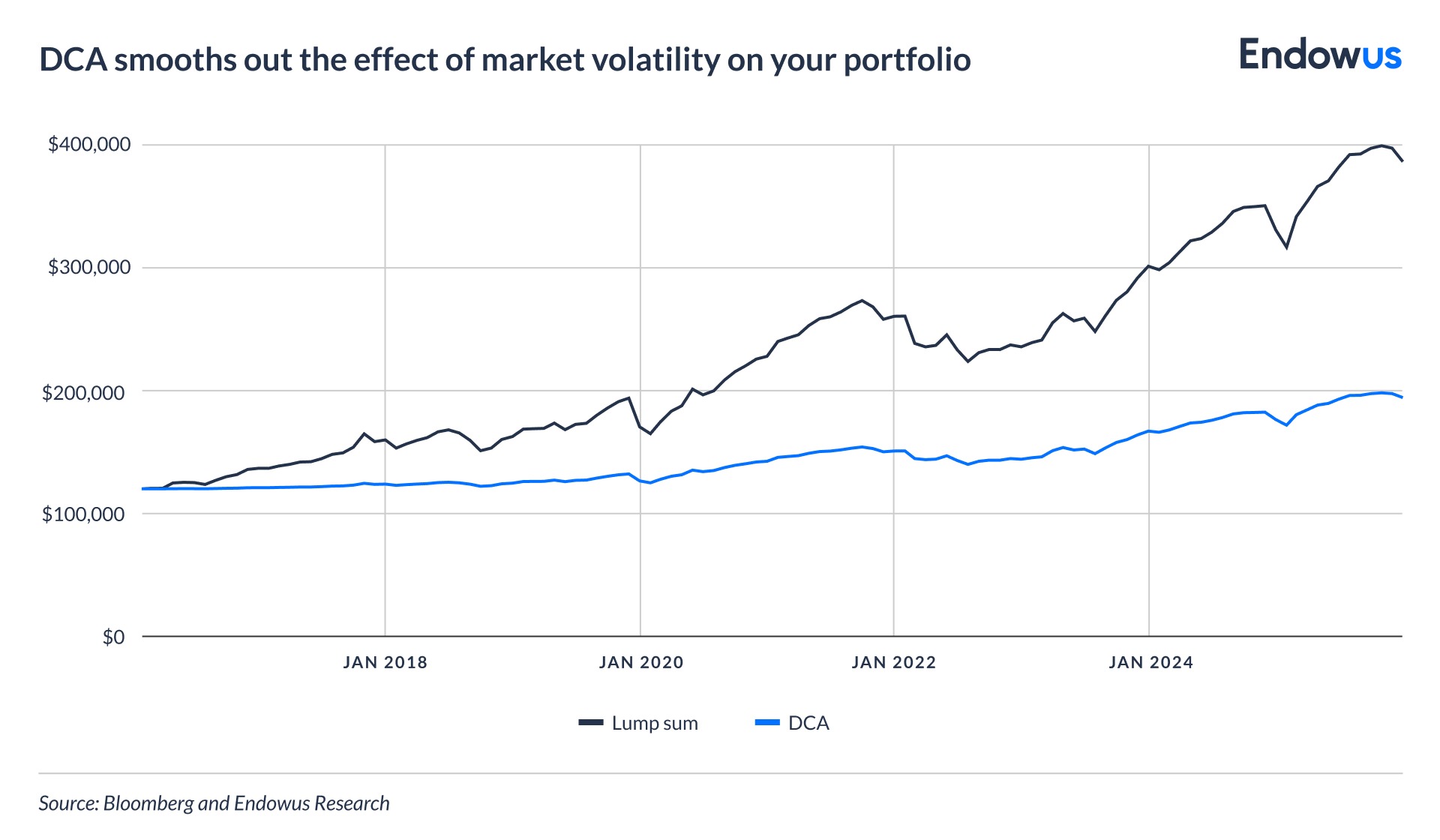

Two investors have S$120,000 capital. The lump sum investor invests the full sum at the start, while the DCA investor invests S$1,000 every month while keeping the rest in a non-interest bearing cash account (assuming inflation is 0). While the lump sum investor’s portfolio has a higher terminal value (S$386,694) than the DCA investor’s portfolio (S$194,341), the latter has a lower volatility (1.37%) than the former (3.02%).

The third—and, in our view, the most practically important—is when an investor’s behavioural tolerance for near-term drawdowns is limited. An investor who deploys a large lump sum and subsequently experiences a significant decline in portfolio value may liquidate the position, crystallising the loss and forfeiting the recovery. The same investor, deploying capital gradually, may find it easier to maintain the strategy through periods of stress. The behavioural benefit of DCA is not captured in any return simulation, but it is real and consequential.

When does lump-sum investing outperform?

The academic evidence on this question is consistent: in the majority of historical market environments, deploying capital as a lump sum has produced higher total returns than spreading that same capital over a series of instalments. A widely cited analysis by Vanguard, covering US, UK, and Australian markets across multiple decades, found that lump-sum investing outperformed DCA in approximately two-thirds of rolling periods examined, with average outperformance of around 2% to 3% over a 12-month deployment horizon.

The intuition is simple: equities have a positive expected return over time, and capital that is not yet deployed earns no return. The longer capital sits in cash awaiting deployment, the more of that expected return is foregone.

This does not mean lump-sum investing is always the correct approach. It means that, all else being equal, an investor with a long horizon and a genuine capacity to hold through near-term drawdowns without making reactive allocation changes will, on average, accumulate more wealth by deploying capital immediately. The condition—genuine capacity to hold through drawdowns—is one that many investors overestimate when markets are rising and discover they do not possess when they are falling.

Why consistency often matters more than optimisation

Financial literature on investor behaviour is unambiguous on one point: the average investor’s realised return is substantially lower than the return of the funds they hold, because they tend to add capital at elevated valuations and withdraw it during drawdowns.

DCA does not guarantee superior returns. What it does is reduce the decisions an investor needs to make and, in doing so, reduces the number of opportunities to make a poor one. An investor who commits to a fixed monthly investment in a diversified portfolio—and maintains that commitment through periods of market stress—is likely to accumulate more wealth over time than one who invests opportunistically but consistently errs on the side of caution when conditions deteriorate.

This is the context in which DCA is most valuable: not as a return-maximisation strategy, but as a commitment device that keeps investors invested. The question for any individual is not whether DCA is theoretically optimal. It is whether, in the absence of a structured approach, they would otherwise defer deployment, reduce contributions, or exit the market at the wrong point in the cycle.

Investment implications

At Endowus, we believe the choice between DCA and lump-sum deployment should be determined primarily by two factors: the nature of the capital being invested, and an honest assessment of the investor’s behavioural tolerance for near-term portfolio drawdowns.

For investors accumulating wealth from regular income, which is the majority of long-term retail investors, the question is largely academic. Capital should be deployed as it becomes available, consistently, without attempting to time entry points. The discipline of regular investment, maintained through market cycles, is itself the strategy.

For investors with a large existing sum to deploy—from a bonus, inheritance, or property proceeds—the decision warrants more consideration. If the investor has a long horizon, genuine capacity to hold through drawdowns, and no pressing liquidity needs, lump-sum deployment is likely to produce a higher expected terminal value. If there is meaningful uncertainty about any of those conditions, a structured deployment over three to 12 months reduces the risk of a large early drawdown materially impairing long-run outcomes or, more importantly, triggering a behavioural exit at the trough.

The worst outcome in either approach is not suboptimal timing. It is exiting the market entirely during a drawdown and failing to participate in the subsequent recovery. A strategy that prevents that outcome—even at some cost to theoretical maximum return—is likely to deliver better real-world outcomes for most investors.

Frequently asked questions about DCA

Does DCA outperform lump-sum investing?

In most historical market environments, lump-sum investing has produced higher total returns than DCA over comparable periods—because capital deployed immediately begins compounding immediately. However, DCA tends to outperform in volatile or declining markets, and its primary advantage is behavioural rather than mathematical: it reduces the risk of poor entry-point timing and supports investment discipline through periods of market stress. Past performance is not necessarily a guide to future performance or returns.

When should I use DCA?

DCA is most appropriate when capital is being accumulated gradually from regular income, when market conditions are unusually volatile, or when an investor’s tolerance for near-term drawdowns is limited. It is also a useful framework for deploying a large lump sum in a structured way, reducing the risk of a significant early drawdown at the point of maximum capital deployment.

What is sequence-of-returns risk?

Sequence-of-returns risk refers to the impact of the order of investment returns on long-run portfolio outcomes. For accumulating investors, poor returns in the early years are less damaging than poor returns later, because less capital is at risk when contributions are smaller. DCA naturally reduces sequence-of-returns risk by concentrating deployment in periods of lower valuations.

How often should I invest with DCA?

The optimal frequency depends on transaction costs, the investment vehicle, and the investor’s income cadence. Monthly contributions aligned with salary payment are the most practical framework for most retail investors. The specific interval matters less than consistency: a strategy maintained through periods of market stress will almost always produce better outcomes than one abandoned when conditions deteriorate.

Webinar: Investing in a better future: Through the lens of an equity investor

Why ESG investing should matter to Singaporeans

When you can’t see the forest for the trees: A holistic approach to asset allocation

%20F1(2).webp)

.webp)

.webp)