.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

- Inflation and longevity are the two key risks that make retirement planning difficult, our wealth needs to outpace rising costs and sustain you through retirement.

- Experiences are not enjoyed the same as we age—as we build wealth for retirement, we need to learn to spend it meaningfully, both now and later.

- A holistic retirement plan gives you the flexibility to spend now, while achieving financial adequacy for retirement in the years to come.

There is a certain irony at the heart of retirement planning. Most people spend their working lives anxious about not saving enough. Then, when they finally arrive at retirement, they are often too afraid to spend—leaving money unspent, and experiences unlived, in the name of prudence.

Bill Perkins captures this tension well in his book, Die With Zero, presenting a case against the instinct to save indefinitely. Perkins describes how retirees move through three phases: in the early, active years of retirement, the "go-go" phase, energy levels are high and the appetite for travel, adventure, and new experiences is strong. The "slow-go" phase follows, where health begins to shape or even limit what is possible. Finally, the "no-go" phase brings a quieter existence where the pleasures of life shift inward—family, comfort, and routine.

The implication is uncomfortable but worth sitting with: some experiences are best enjoyed now, not later. Saving obsessively and spending on hardly anything is essentially a waste of money, Perkins writes.

But his argument, compelling as it is, leaves an important question unanswered: how do you spend without worry if you do not know whether you have enough?

This anxiety is not irrational—the cost of living rises year by year, and none of us knows for sure how long we will live.

Why do we never feel there’s enough?

Based on statistics by the Ministry of Manpower, real median gross monthly income—adjusted for inflation—grew 2.1% per annum (p.a.) over 2015–2025. While income growth has outpaced the Consumer Price Index (CPI) inflation, we still hear many Singaporeans lament the rising cost of living.

It’s harder to feel the ground under our feet

In his 2026 annual letter to investors, Chairman of BlackRock, Larry Fink, wrote that today’s economic anxiety comes from “a deeper feeling that capitalism is working—just not for enough people.” Mass layoffs and AI disruption paint a sobering picture of today’s job insecurity. Neither is the financial reward of employment always proportionate to the time and effort one gives.

Fink presents an unfiltered view of reality: “the vast majority of wealth has flowed to people who owned assets, not to people who earned most of their money by working.” His words are a poignant reminder that investing is non-negotiable today—in fact, it is the only way to accumulate enough wealth so that we do not outlive it.

Outliving our wealth is a real concern

Longevity risk impacts all of us, and we should all be worried about it. As of 2024, Singapore’s life expectancy at birth is 83.5 years—a continuity of a gradual upward trend.

Between 2001–2025, the average annual CPI inflation was 1.9%. Assuming the same average inflation rate over the next 25 years, a 35-year-old with $40,000 in annual expenses now will need approximately $64,000 to maintain the same standard of living at 60. While average income tends to grow faster than inflation during our working years, the pressure comes when we wonder if our accumulated wealth can carry the full weight of rising costs at retirement.

A sound retirement income plan must address two related questions. First, income: in the absence of a salary, how do you ensure a stable, predictable source of cash flow to sustain your lifestyle? Second, capital: what strategy preserves, and ideally grows, the pool of wealth that finances this income, so that it does not run out before you do?

How to plan for retirement, and for peace of mind

The bare minimum: Beat inflation

Emergency savings—typically three to twelve months of living expenses—should sit in a bank account for accessibility.

However, being cash-heavy has its costs too. A basic savings account at major Singapore banks offers a base interest rate of about 0.05% per annum (p.a.). With headline inflation averaging 1.9% in the last 25 years, cash that sits idle in such savings accounts is essentially losing purchasing power. Lower risk financial instruments like money market funds and shorter duration bonds offer liquidity while growing your cash.

Spend as you build wealth

Retirement planning does not mean deferring all enjoyment until you stop working. The key is to separate your wealth into pots based on when you need the money, and invest each pot accordingly.

Taking travel plans as an example: for a regional trip to Asia within the next one year, investing your savings in a low-risk portfolio keeps them on a steady, gradual growth. For a Europe tour in five years’ time, you can afford to take on slightly more risk for potentially higher returns. And for retirement, which may be decades away, a longer time horizon means you can ride out market volatility and invest more aggressively for growth.

This goal-based approach also brings discipline to how you deploy your money, so your near-term spending plans and long-term retirement savings are not competing with each other.

Secure lifelong, guaranteed retirement income with CPF

For Singaporeans, CPF is one of the most important components of retirement planning. Two features make it particularly relevant.

- Forced savings, rewarded with attractive risk-free interest rates: 2.5% p.a. on the Ordinary Account (OA) and 4% p.a. on the Special (SA) and Retirement Accounts (RA) are the floor interest rates for CPF. These interests compound reliably over decades, which is why starting early matters. Voluntary cash top-ups to your SA or RA are rewarded with tax reliefs and matching grants.

- Insurance against longevity risk for everyone: CPF LIFE, the national longevity insurance annuity scheme, provides monthly payouts for as long as you live. Unlike drawing down from a fixed pot of savings, CPF LIFE does not run out.

That said, whether CPF savings and CPF LIFE payouts are adequate at retirement varies from individual to individual. The earlier you start planning for your CPF savings at retirement, the more time you have to act.

Plan your decumulation strategy

The transition from accumulation to decumulation is not as simple as "start spending what you saved".

Decumulation is about strategising which pool you draw from first, how much, and when. One of them is a bucketing strategy that apportions your retirement by time horizon to minimise sequencing risk. For instance, a retiree may create three buckets of wealth:

- Bucket 1: Covers three years’ worth of their expenses, held in cash, money market funds, government bonds or other low-risk investments.

- Bucket 2: For use in the next 3–7 years, and is meant to replenish Bucket 1 when it has been depleted. The majority of it is allocated to defensive assets like bonds for modest growth, and possibly some allocation to equities for growth.

- Bucket 3: Primarily for longer term growth, and similarly, meant to replenish Bucket 2 when it has been sold down. With a longer time horizon, short-term market volatility typically has a muted impact. Hence, higher allocation towards risk assets, like stocks, may be preferred.

Clearly demarcated buckets of wealth can give more clarity on how much you can spend at retirement, and a peace of mind that it continues to grow for future needs. Taking a simple, yet still structured approach can allay anxieties of running out of retirement savings.

“But, what if…”

What if there is a market downturn just as I retire?

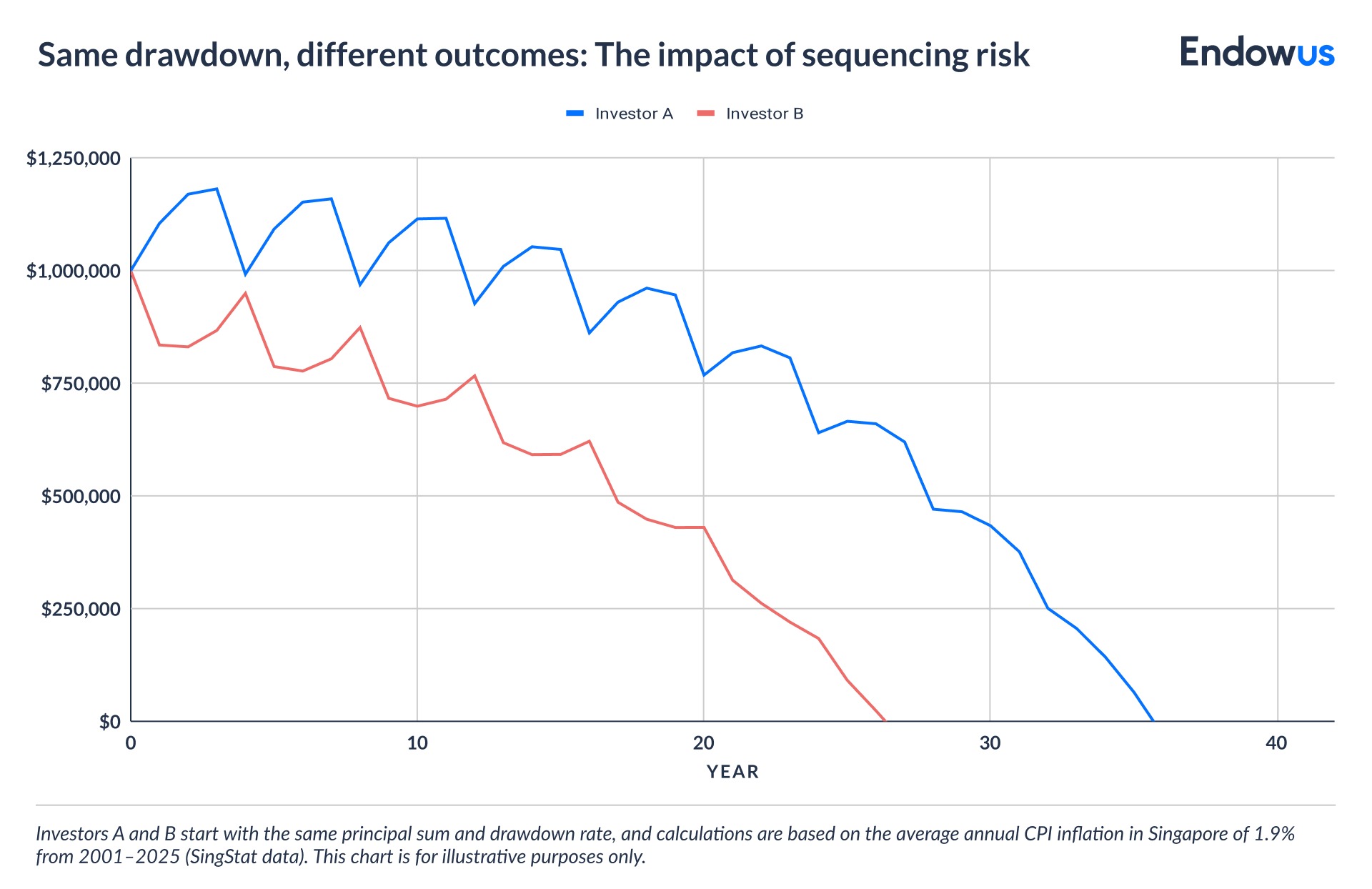

This is one of the most common concerns in retirement planning, also called sequencing risk. A market decline early in retirement—when you are simultaneously drawing down—reduces the principal sum, which has knock-on effects on your portfolio.

Take the following chart for example: two investors with the same initial capital and drawdown rate, but experience a negative return in their first and fourth years respectively, could see a near 10-year difference in how long their wealth can last through retirement.

There are a few mitigation strategies:

- Maintain a one-to-three-year cash buffer you draw from during downturns, letting your portfolio recover without forced selling.

- If you are more risk averse, ensure your CPF LIFE payout covers a meaningful share of essential monthly expenses to reduce exposure to market volatility.

- Ensure your retirement portfolio is globally and sectorally diversified to spread risks.

What if inflation is higher in retirement than I planned for?

CPF LIFE's Escalating Plan, which provides monthly payouts that increase 2% yearly, is also worth considering for those who want some protection against inflation. The trade-off is a lower initial payout compared to the Standard Plan, which pays out the same amount monthly.

Within an investment portfolio, risk assets, including equities, are typically the main driver of growth. An appropriate allocation to equities, based on personal risk tolerance and time horizon, gives your wealth a better chance to beat inflation.

What if my portfolio does not grow as fast as projected?

Look beyond headline returns and scrutinise your investing fees. Just like returns, fees compound over time. Keep investment costs low, avoid overactivity (i.e frequent trading), ensure returns are commensurate with the risk you take, and revisit your financial plan regularly to ensure it keeps pace with your goals.

What if I need to stop working earlier than planned?

Early retirement may or may not be voluntary or expected, which is why early planning is important. The compounding effect of CPF interests and investment returns gets more pronounced with time—take advantage of it so that you are financially prepared for curveballs.

What if I am already in my 50s and have not yet started?

Starting late is better than not starting at all. A 50-year-old still has a 15-year runway before the typical retirement age. Take advantage of schemes like the Matched Retirement Savings Scheme (MRSS), which offers dollar-for-dollar grant on cash top-ups to CPF for Singaporeans aged 55 and above, and yet to have the Basic Retirement Sum in their CPF retirement savings.

You may also wish to speak to our MAS-licensed financial advisors for personalised guidance on building an investment portfolio for your retirement goals.

The bottom line

Retirement anxiety is, in part, a logical response to genuine uncertainty. None of us knows exactly how long we will live, how costs will evolve, or how markets will behave. However, having a proper retirement plan helps us to live better, now and later.

Take a systematic approach: build a stable foundation of guaranteed, lifelong income through CPF LIFE or an annuity plan, supplemented by an investment portfolio, sized and structured to sustain your desired lifestyle across all phases of retirement. The strategy is not to obsess over every dollar of savings. It is to live well—and to do so with enough confidence in your finances that you actually can.

Endowus brings wealth planning together with Cash, CPF and SRS investing, enabling you to create distinct portfolios for different goals and life stages. Each portfolio is tailored to its specific time horizon and risk profile, ensuring you're financially prepared throughout your journey—all at an all-in Endowus Fee starting from only 0.15%, up to 0.60% p.a. Get started with Endowus today.

Retiring with a bucketing strategy

The Nanny State, Crazy Rich Asians and lessons for your retirement plan in Singapore

Should a new Singapore Permanent Resident make voluntary contributions to CPF accounts?

%20F1(2).webp)

.webp)

.webp)