.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

The original version of this article first appeared in The Business Times.

Everyone is focused on the war, the Fed, inflation, the US dollar. Are we focusing on the right things right now?

Let’s start with what we know. The Iran war has produced the largest oil supply disruption in the history of the global energy markets, taking 12 million barrels per day off the market—more than the two 1970s oil crises combined. Brent crude has surged more than 50% in just one month.

Although countries are releasing strategic petroleum reserves at a record pace, fuel, and potentially energy, shortages are rippling through Asia. The expected rise in prices, combined with the likely economic slowdown, is increasing the risk of stagflation.

The fallout across financial markets has been swift but surprisingly measured. Global equities are only down by single digits year-to-date. Bond yields have risen on renewed inflation fears. Gold has rebounded somewhat on safe-haven demand together with the US dollar, though both remain off their highs after a sharp selloff, which is a similar story for Bitcoin. These are the facts, but what does that mean for investors?

Correlation is not causation, and narrative is not analysis

The temptation during a crisis is to draw a straight line from geopolitical events to investment conclusions, and a lot of the focus and concern still centres on the US dollar. With the US at war, these concerns are more pronounced as President Trump requests a record $2.2 trillion budget, of which $1.5 trillion is earmarked for defence, which may worsen its fiscal situation and reignite concerns about the dollar’s position as a reserve currency.

However, the US is a net exporter of oil and is less directly exposed to energy-driven shocks than many peers. The dollar has, in fact, strengthened recently, reflecting its continued appeal as a safe-haven asset in times of uncertainty.

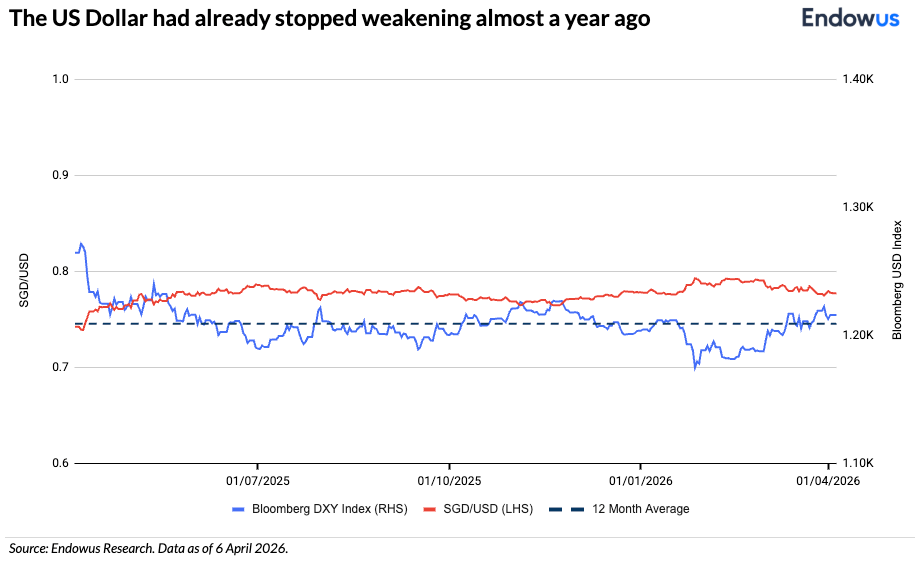

The US Dollar Index (DXY) sits at 100 today. Over the past 12 months, it is down only 2.7%, a remarkably modest move given the geopolitical turmoil and the widespread expectations of a dollar collapse that dominated financial commentary throughout 2025. The DXY traded above 109 in January 2025, fell to the mid-96s, but has since recovered approximately 5% from the lows of September 2025 to the current level. Through all of the noise and clamour, it has been essentially flat for the past year.

For Singapore-based investors, it is important to be reminded that the Singapore dollar has appreciated roughly 4–5% against the US dollar over the past year. That sounds like a meaningful headwind—until you put it in context.

The SGD has been on a gradual, structural appreciation path against the USD for decades, managed by the Monetary Authority of Singapore through its nominal effective exchange rate policy band. This is not a crisis. It is the normal cost of holding a global reserve currency from a small, open economy with strong fundamentals. And the SGD’s strength is far more pronounced against other regional currencies—the ringgit, rupiah, baht, won, yen, and rupee.

It’s not a US dollar problem, it’s a Singapore dollar issue. The stronger SGD allows Singaporeans to gain greater purchasing power and will allow Singaporeans to spend less to gain the same experience or buy goods overseas.

The dollar is not dead, and its resilience has consequences

However, here is an inconvenient truth for those who predicted the demise of the US dollar: its recent strength, driven by safe-haven demand and expectations that the Federal Reserve will keep rates higher for longer, has actually acted as a brake on the very assets that are supposed to replace it.

Gold and Bitcoin are both denominated in US dollars. When the dollar strengthens, it creates a headwind for these assets in local currency terms, even as their USD prices rise. This is one reason gold’s rally, while impressive, has been more measured than many expected in a genuine energy crisis. Bitcoin, despite the narrative of being a digital safe haven, has delivered returns roughly in line with gold and well off the highs of last year—hardly the exponential outperformance to the moon that its advocates promised.

None of this is to say the dollar does not face long-term structural challenges. The US fiscal trajectory is unsustainable and the weaponisation of the dollar through sanctions has given other nations reason to seek an acceleration to find alternatives. But the gap between “long-term structural concern” and “imminent collapse” is enormous, and investors who confuse the two are making decisions based on fear, not evidence.

What the science tells us about currency and investing

Behavioural finance literature is clear on why investors consistently overreact to currency movements. Recency bias causes us to extrapolate the recent past into the indefinite future: if the dollar has weakened over the past quarter, our minds project that weakness forward in a straight line. Availability bias means the most vivid, alarming headlines about de-dollarisation, BRICS alternatives, or the end of American hegemony, dominate our thinking, even when the data tells a more nuanced story.

Three decades of institutional investing experience have taught me this: making directional bets on currencies is extraordinarily difficult. Even the largest, most sophisticated institutional investors rarely attempt it, and even more rarely get it right. The foreign exchange market is the deepest, most liquid, and most efficient market in the world. The idea that an individual investor can consistently outperform it, or even the stock market, is a fantasy.

The only legitimate reason to take a currency view is when you have future liabilities denominated in a specific currency, such as a mortgage, retirement expenses, medical costs, or children’s education. That is not speculation. That is asset-liability matching, and it is the foundation of sound financial planning.

What Singapore investors should actually do

Rather than worrying about the direction of the US dollar, focus on what you can control.

First, take advantage of SGD-hedged share classes, particularly in fixed income. Currency hedging in bond funds is prevalent, cost-efficient, and removes a source of volatility that has nothing to do with the underlying investment thesis. When you invest in a global bond fund for its yield and diversification benefits, there is no reason to also take on an uncompensated currency bet.

Second, think about your future liabilities. Your biggest financial risks are not that the dollar will depreciate in a given year. It’s that inflation will erode your purchasing power over decades. That healthcare costs will outstrip your savings. Housing prices will continue to climb. These are SGD-denominated problems, but the answer is not to avoid global diversification. It is to invest globally, thoughtfully, and to hedge where the cost is low and the benefit is clear.

Third, diversify. The best antidote to the anxiety of any single geopolitical event, currency move, or asset class drawdown is a portfolio that does not depend on getting any one call right. Diversification remains the only free lunch in investing, and it is as relevant during the Iran war as it was ever before.

The physicist Richard Feynman once observed that the first principle of science is that you must not fool yourself—and you are the easiest person to fool. In investing, the equivalent principle is this: the market is not trying to tell you a story. You are telling yourself a story about the market, and that story will determine whether you act wisely or foolishly.

The story of the US dollar in 2026 is not one of collapse or crisis. It is one of resilience, complexity, and the enduring truth that short-term noise almost never matches the long-term signal. The investors who will do best are not the ones who correctly predict the next move in USD/SGD. They are the ones who build a diversified portfolio aligned to their goals, stay invested through uncertainty, and refuse to let the fog of war become the fog of their financial future.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)