.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).gif)

Register for the event

Endowus invites you to our exclusive event with Macquarie Asset Management, as we discuss unlocking opportunities in Infrastructure- a $1.3tn asset class.

This event is reserved for Accredited Investors (AIs) only. To register for the event, please indicate one of the following:

The original version of this article first appeared in The Business Times.

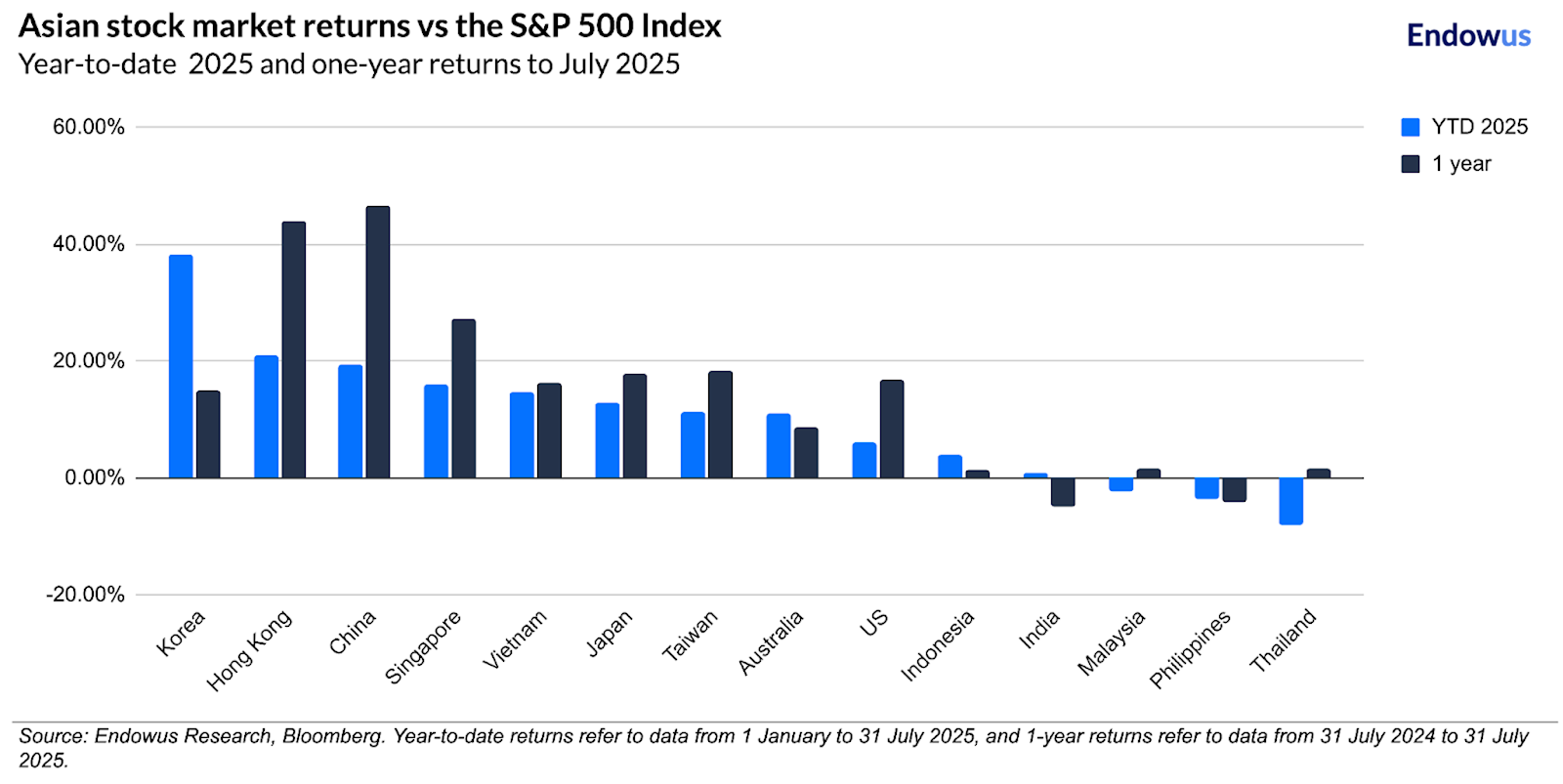

Last year, Singapore was one of the best performing markets globally. The Straits Times index hit record highs. Questions abound, asking how much more upside there is and whether it can continue to outperform its regional peers. This year, the index has underperformed some markets like Korea, China and Hong Kong; however, it remains one of the best performers.

We forget that this outperformance follows a sustained period of underperformance for Singapore. Many other markets are also at historic highs. The question may not be whether we invest or not, but how much of what we invest should we put in our home market?

Why do we prefer investing in our home market?

It is human nature to favour something familiar to us. This is known as mere exposure bias. It describes our tendency to develop preferences or dislikes for things simply because we are familiar with them. That is why it is also known as familiarity bias.

Now, as we apply this in the context of financial markets, this is expressed in the form of home bias or home country bias, which is the tendency for people to invest the majority or all of their investments into domestic equities, ignoring the benefits of diversifying into foreign equities.

It could also be caused by difficulty in investing in overseas markets, such as regulations, cost or FX. However, familiarity bias is often what causes individuals to invest in the home market and companies that they are more familiar with, despite evidence that diversification can produce a more optimal portfolio.

US exceptionalism is alive and well

This home bias exists in every market, including the US, Singapore and across Asia. However, the effect is different because some markets are bigger and have broader representation than others. There is only one market that is big enough and has globally competitive companies listed, is diversified across geography, sector and size, that allows for a meaningful and consistent outperformance over time, and that is the US stock market.

Whether it is the S&P 500 index or the broader Russell indexes, the US represents more than half of the global stock market capitalisation, and 64% of the MSCI All Country World Index (ACWI). The next largest is Japan at below 5%, which attests to the big gap the US has over every other market in the world and shows how exceptional the US market is.

It is also why in the past two decades, there have been increasing investments flowing to the US as a form of diversification for local non-US investors. The average annual foreign capital flow into the US stock markets has increased from an average U$50 billion in the 1970s to over $500 billion in recent years. This, in turn, has resulted in better returns for these investors as it has achieved the best long term returns.

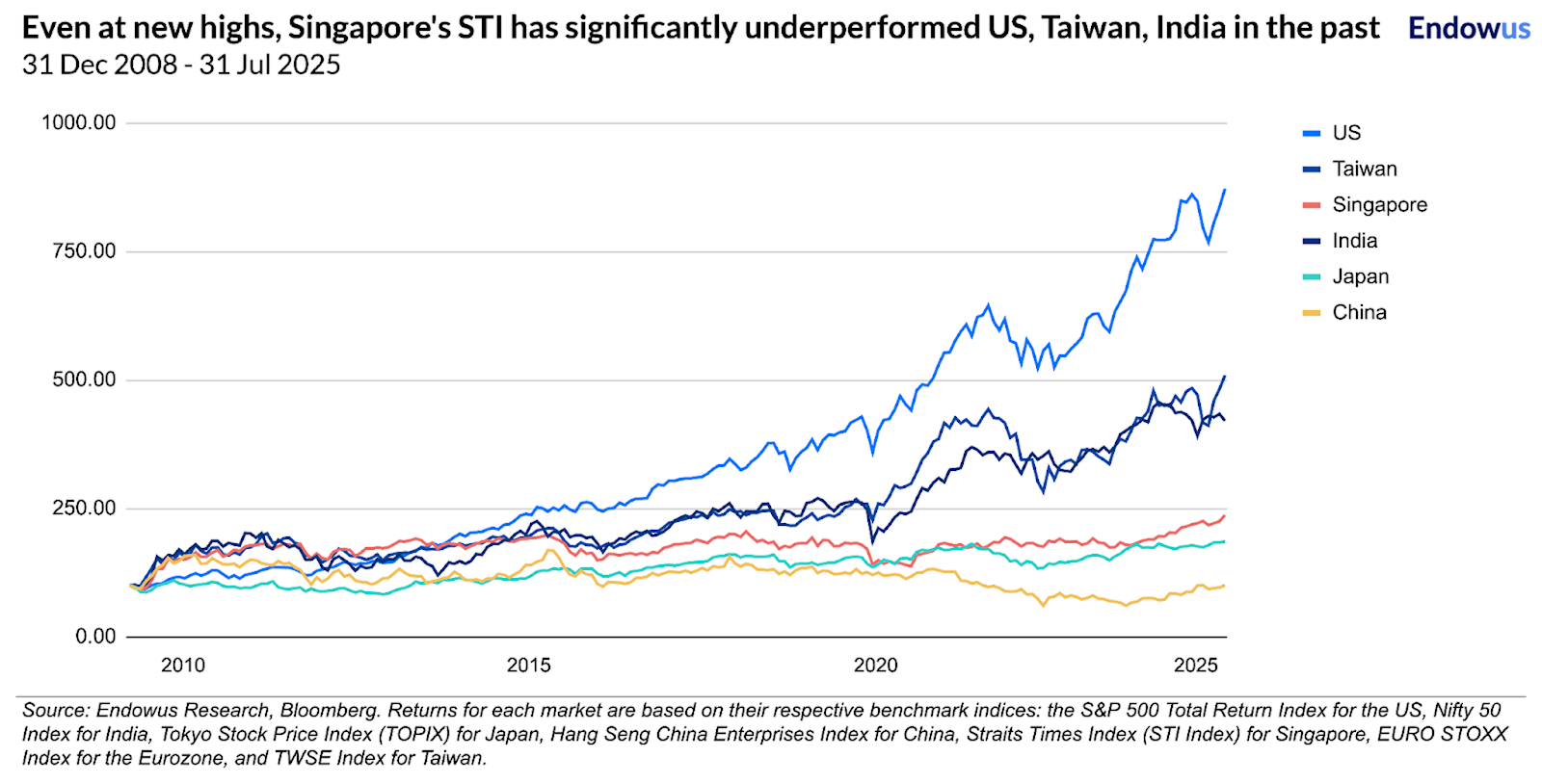

Has home bias been good for Singapore investors?

Singapore’s primary benchmark stock market index is the Straits Times Index, which is a collection of the 30 largest and most liquid companies listed on the SGX. There are over 600 companies listed on the SGX. While the STI represents a meaningful S$622 billion of market capitalisation, the total Singapore market cap is greater.

Recently, the MAS announced its Equity Market Development Plan (EQDP) to revitalise and broaden the Singapore equity market, especially the mid- and small-cap segment outside the STI. It has allocated S$5 billion to co-invest alongside private capital and has allocated some initial capital to Avanda, Fullerton, and JP Morgan Asset Management. Also, Amundi, the largest European asset manager, has launched the lowest cost STI index fund at 0.15% in Singapore. Both initiatives are happening in time for SG60.

With the STI index reaching new historic highs and the Singapore market receiving renewed interest through these new product launches and support from the government, many investors wonder whether this rally has more legs.

We know that diversification is a great strategy as it is a way to mitigate the risk of putting all your eggs in one basket. In fact, for an extended period, the Singapore market has been a perennial underperformer. Over the past 15 years, the STI underperformed the S&P 500 in 11 of 15 years, and the STI is up 2.4x compared to the S&P 500, which is up 8.7x during that time. Of course, the real question is whether this trend will continue or if it is a case that past performance is not a good representation of future performance? In fact, the period between 2002 and 2012 marked a period where STI outperformed 9 out of 11 years.

How do individual countries outperform

While no other country is comparable to the US, some regional players do set themselves apart. India, for its growth and diversified sectoral exposure, and Taiwan, for its tech and entrepreneurial companies generating high returns on equity through cycles, are two examples of countries with good equity culture that have generated better returns. These countries also exhibit strong home bias.

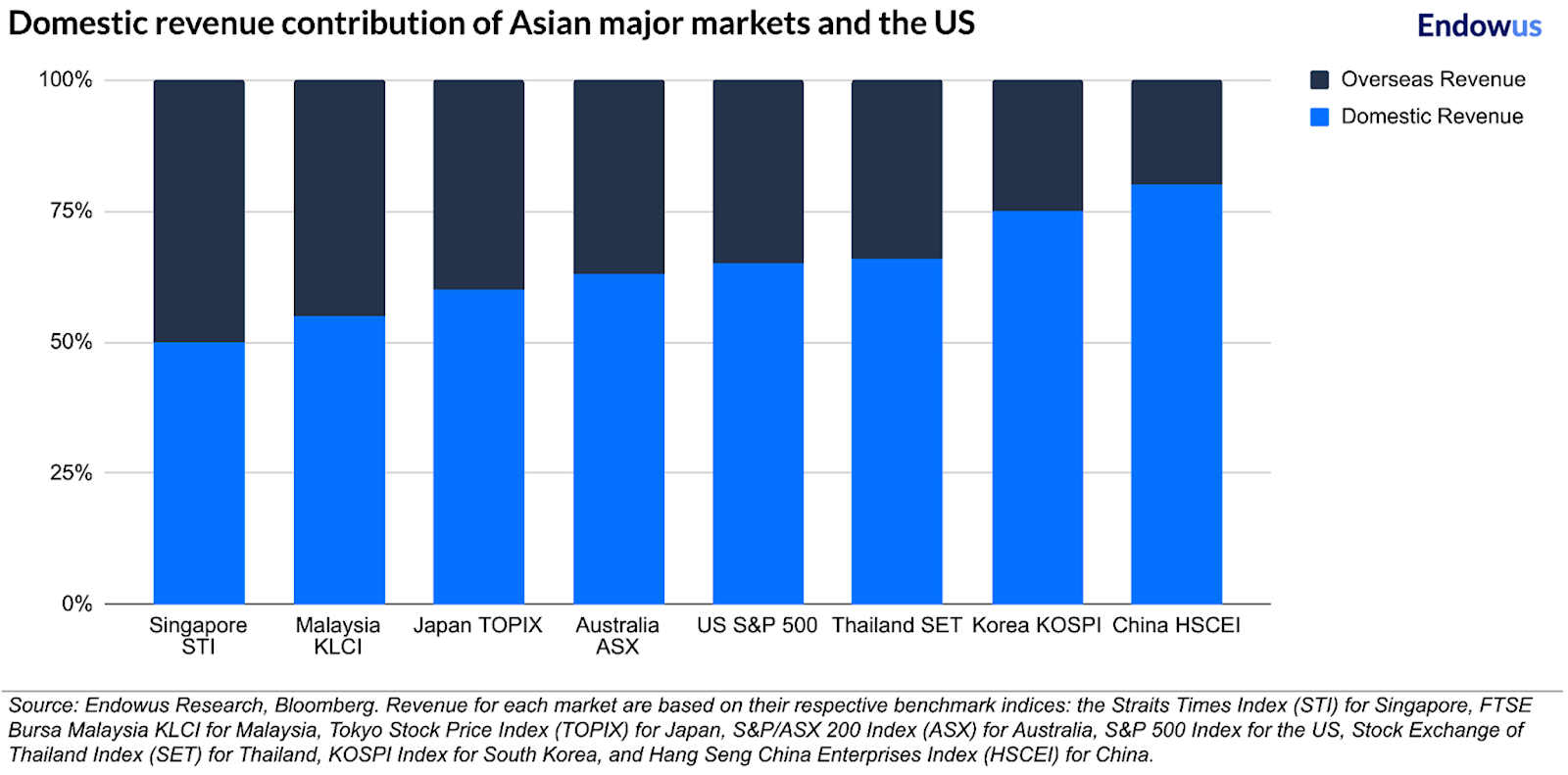

What sets Singapore apart is the fact that it is the market with the lowest dependence on the local economy and the highest overseas revenue contribution, compared to the other major stock market indexes in the rest of Asia and the US. Most of it comes from the close neighbours in South East Asia, but this growing diversification in its revenue source is a positive.

Another good example of a positive home bias is Australia, with its ageing and wealthy population and its superannuation pension system. It has many similarities to Singapore, which has one of the highest GDP per capita, savings pool, ageing population and housing ownership in the world, as well as the CPF Investment Scheme. Singaporeans have the wherewithal to invest consistently in their local market too.

What drives change?

We can feel the world is changing. The continued noise around the tariff wars, the concerns about US economic growth and the Fed’s interest rate policy abound. However, these are cyclical issues. The underlying current of structural changes is pointing to a new global regime and the end of a US-led post-war international order, which could reshape many things, among which is international cross-border investment flow. A rise of inwardly looking countries may start to keep more of their capital at home. This is why a new structural change of this order and magnitude could reshape investor behaviour and investment patterns that could be positive for the Singapore market and the Singapore dollar over the long term.

Investing in our home also goes beyond the stock market. It is important, especially with Singapore’s demographics, that we do more to diversify into regional opportunities and nurture and support the local economy and enterprises. However, investing in the social sector is just as important as investing in the financial sector. That is why as we kickoff the SG60 celebrations, the Community Chest, National Volunteer and Philanthropy Centre and Endowus have teamed up to launch the “Invest in our Home” campaign to raise awareness and fundraise for strong local charities and non-profit organisations that will strengthen the fabric of our society and generate greater social returns as well as financial returns.

Webinar: Travel, market and crypto bubbles

.png)

We are heading into bubble trouble

Endowus 2020 review and 2021 outlook

%20F1(2).webp)

.webp)

.webp)